Yi Hai Lun Bi writes each analysis article with a responsible, focused, and sincere attitude, with distinctive features—no pretentiousness, no exaggeration!

Daily market interpretation, I am digital currency analyst Yi Hai Lun Bi!

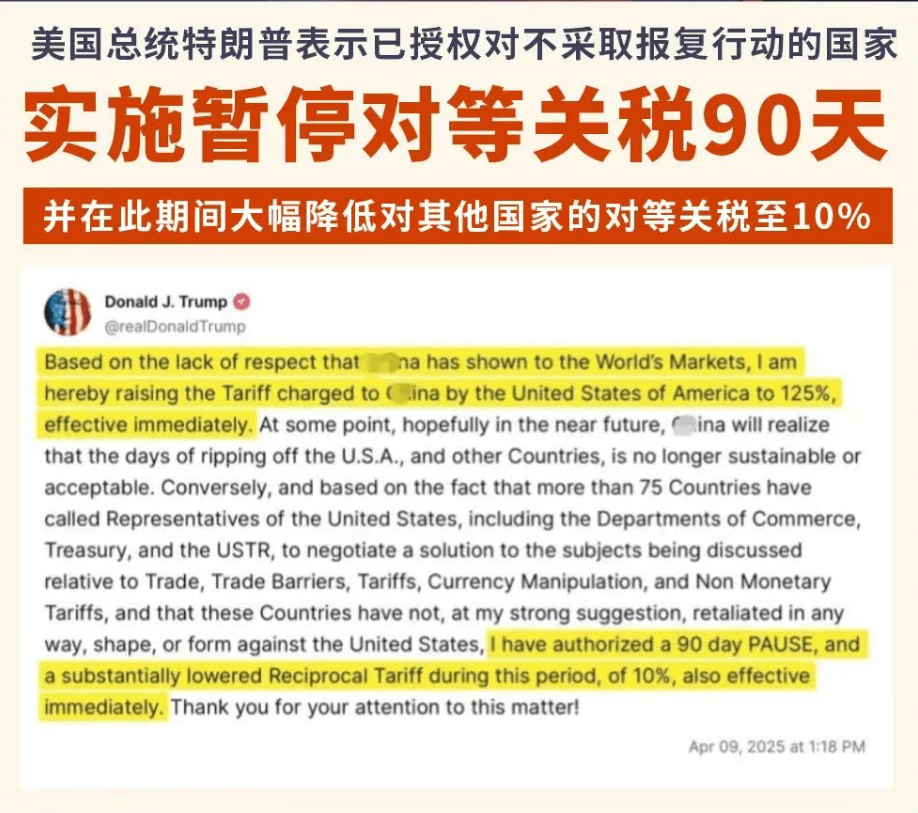

Earlier, it was mentioned that the CPI data released by the U.S. shows that the inflation rate is declining. Yesterday, the PPI data for March was released, showing a month-on-month decrease of 0.4%, the largest drop since October 2023, primarily due to the decrease in energy costs. The drop in oil prices is not a healthy sign and has reignited concerns about an economic recession in the U.S. Trump announced a 90-day suspension of tariffs, adjusting the tax rates for multiple regions to 10%, which only excludes us. Market expectations for an escalation of the trade war have risen again. Furthermore, the U.S. Customs reported yesterday that due to system failures, related tariffs are currently not being collected. The market quickly reacted, and this system failure seems more like a strategic test, indicating that the U.S. may be shifting towards a more moderate stance on tariff policies.

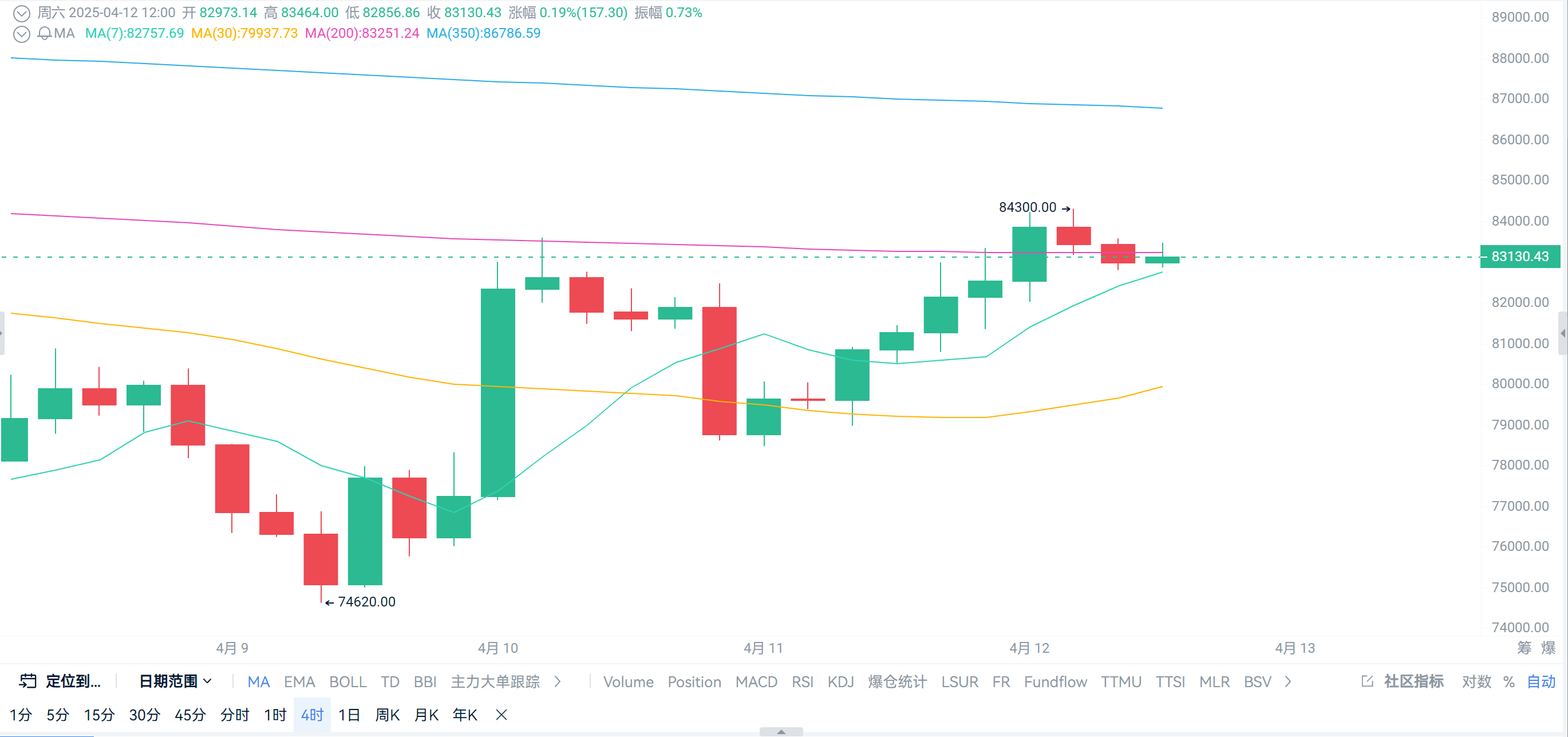

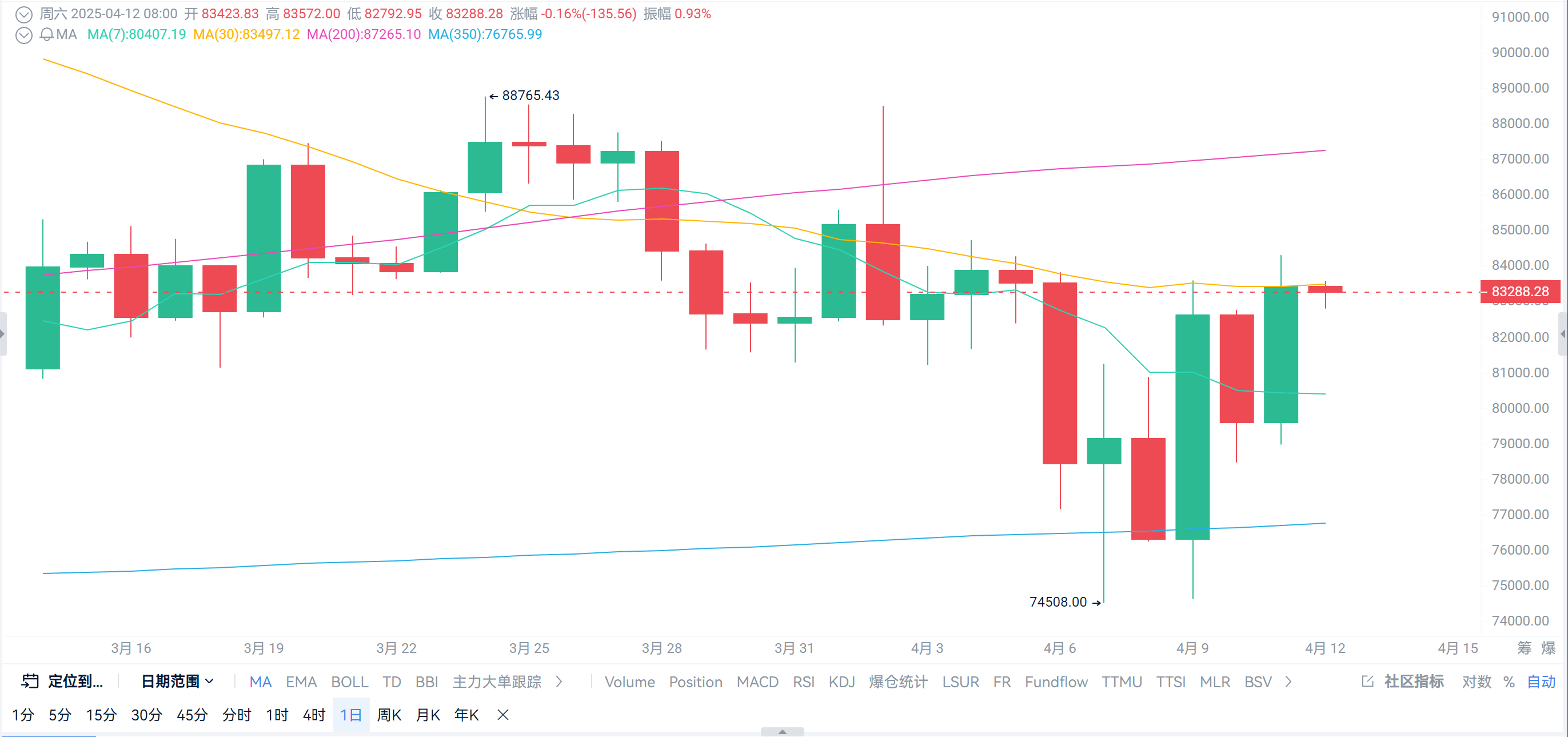

At the same time, Federal Reserve officials have clearly stated at critical moments that if necessary, the Federal Reserve is absolutely ready to step in to stabilize the market. Both the U.S. stock market and the crypto space have welcomed more rebounds, and emotional momentum seems to be building. From the chip distribution chart, the previously mentioned $81,300 to $83,500 is currently a key area. If the support in this area can further play a role, BTC will see higher positions. Technically, BTC has once again tried to stay above the 200 MA on the 4-hour chart. Since the decline in early February, there have been several attempts to hold this position, but ultimately they have not been able to sustain it. Everyone can continue to monitor this key position. However, from the changes in open interest, in just one day, open interest has increased by 10%. Seeing such a rebound over the past month raises questions about sustainability. However, if BTC can stabilize above the 4-hour MA200, its upward space will also open up.

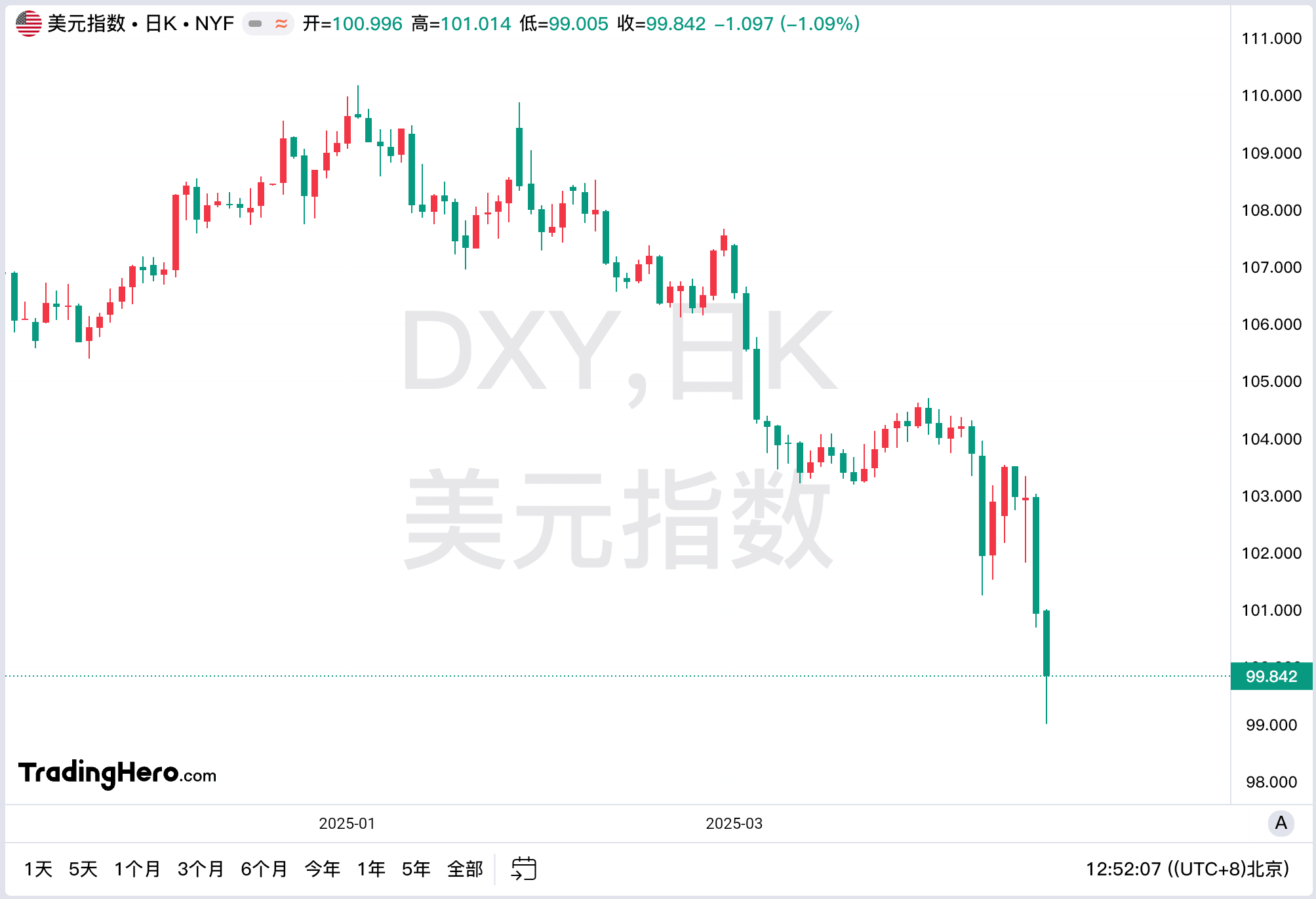

Currently, U.S. Treasuries and the dollar do not seem to be favored by capital. The 10-year U.S. Treasury yield continues to rise, reaching the largest single-week increase since 2001, which means a rapid decline in bond prices, indicating that market liquidity is being quickly withdrawn. The dollar index has also fallen below 100 points, all due to the market's systemic decline in information regarding the U.S. fiscal situation, strategic logic, and global leadership. Safe-haven funds have not flowed into the dollar and U.S. Treasuries as before; instead, the Swiss franc, euro, and gold are performing relatively well. European investors seem to be selling off dollar assets, a rare reversal that suggests the dollar's safe-haven status may be under re-evaluation. Gold prices continue to hit new highs, reaching as high as 3,245. Looking back at past trends, the simultaneous decline of the dollar and the rise in U.S. Treasury yields is very rare. It has occurred four times in the past few decades, each time closely related to systemic financial risks. Before and after Black Monday in 1987, the market was concerned about the U.S. trade deficit and long-term depreciation of the dollar, leading to massive capital outflows, a stock market crash, and severe fluctuations in U.S. Treasuries. During the unexpected interest rate hike cycle in 1994, the market suddenly realized that the pace of rate hikes was underestimated, leading to a massive sell-off of U.S. Treasuries, which also failed to support the dollar. In early 2009, when the U.S. implemented large-scale quantitative easing, market concerns about dollar depreciation and excessive issuance of Treasuries led to short-term declines.

The common characteristics of these periods: the expansion of the U.S. fiscal deficit, unclear or untrusted strategic direction, and outflows of external funds from the U.S. Meanwhile, another risk in the market comes from changes in attitudes in major U.S. Treasury holding regions. We and Japan, as important overseas holders of U.S. Treasuries, seem to be gradually reducing our holdings. Official institutions still maintain a certain level of holdings, but large-scale selling operations seem to be led by hedge funds, which are massively shorting U.S. Treasuries for risk aversion or arbitrage considerations, pushing yields higher. Trump is trying to enhance his negotiating power in the global market by continuously creating market uncertainty while increasing demand for U.S. Treasuries. However, what we see is the exact opposite; the persistent and unpredictable strategy is weakening market confidence in the U.S., forcing funds to flow to other safe-haven tools, with gold prices hitting new highs as the best reflection. In the context of rising U.S. Treasury yields, it conveniently gives the Federal Reserve room for intervention, which also explains the earlier mention of Federal Reserve officials stating that they would step in to stabilize the market if necessary.

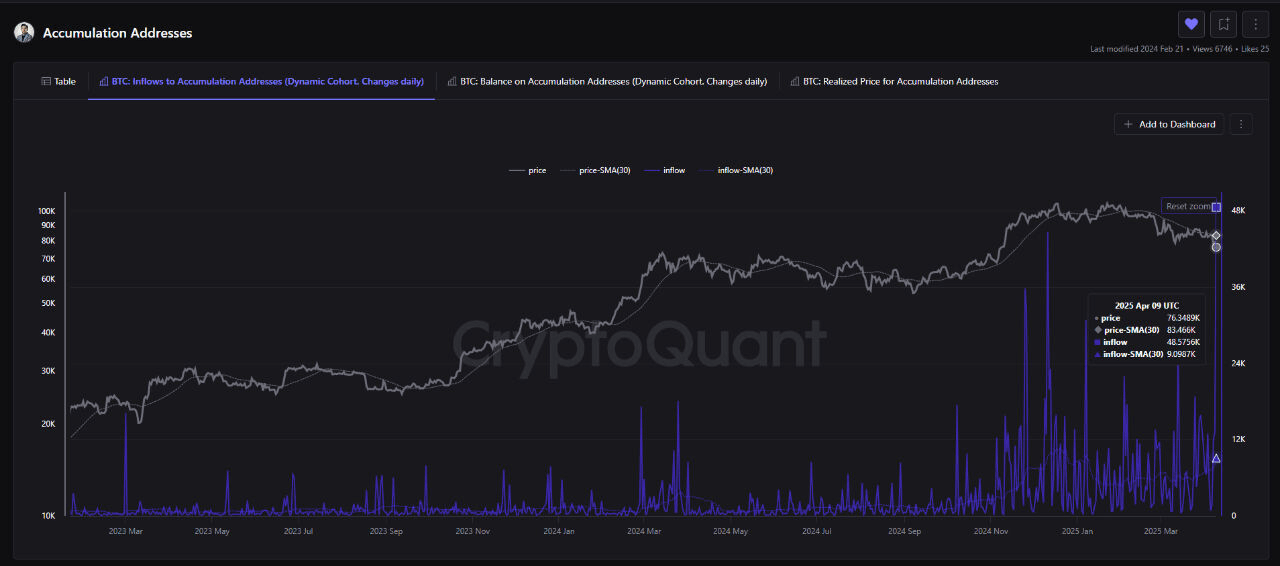

From a global M2 money supply perspective, BTC seems to be about to end its downward trend. Since January until now, the global M2 money supply has rebounded and set new highs. The dollar index has hit a three-year low, bringing more bullish expectations for the future. At least from my perspective, BTC returning to $100,000 is just a matter of time and won't be too far off. Additionally, the supply of stablecoins continues to grow, which is a direct reflection of purchasing power. The explicit demand for BTC has also increased, and BTC whales are still in the market, accumulating more relatively cheap chips. However, in the short term, there are no signs of a reversal. Although BTC has remained above the 365-day moving average, the key points for a trend reversal are for BTC to return above the 200-day moving average and the cost line of short-term holders. However, while the price continues to weaken, the inflow of funds into large BTC holding addresses has seen a significant increase, indicating that BTC whales continue to increase their holdings, which shows their optimism about the market's performance. On-chain data shows that $3.6 billion worth of BTC has flowed into accumulation wallet addresses, the largest single inflow since February 2022. Accumulation addresses are important because they are defined with strong constraints; these addresses must meet the conditions of not transferring out for a long time and not involving exchanges or active circulation. This means they represent those who treat BTC as a long-term asset allocation tool rather than a short-term speculative trading group. When these addresses can still show large accumulation behavior during price fluctuations or significant corrections in BTC, it indicates their strong confidence in BTC's future performance.

Let's take another look at long-term holders. From the decline at the beginning of February until now, the supply from long-term holders has increased by 440,000 BTC, which is the true dominant force in the market. The realized price of BTC is $43,800, while the current spot market price is around $83,000. The level of bubble in the BTC market is not high. If we consider an MVRV ratio of 3.0 or 3.2, multiplying the current realized price by this ratio, BTC would only appear overvalued when it reaches $130,000 or $140,000. Of course, meeting all of this relies on global liquidity, which largely determines the upper limit of the market. On the other hand, BTC is still in a bull market, while the altcoin market remains very difficult. At least the users I have encountered are all facing losses when choosing altcoins. Therefore, I have consistently emphasized that regardless of bull or bear markets, BTC is always the most worthwhile asset in the crypto space.

The current market seems to be guiding us towards a bullish trend, but such times often signify the arrival of risks. However, from a long-term perspective, these concerns can be set aside. The continuous accumulation by long-term investors has provided the market with enough confidence and support. Volatility is inevitable; this does not apply to short-term trading, and the pullback is not expected to be as deep as many imagine. The Federal Reserve seems to be always ready, and some friends may wonder if Trump made a mistake. However, in some aspects, we can indeed see what he wanted to see. Businesspeople pursue profit by any means. It is still too early to draw conclusions; we need to see the final results to know who the true winner is. In summary, the market liquidity has not generated more negative emotions, but the market has also not made any preemptive pricing movements. Current expectations are not sufficient to mobilize market sentiment, and short-term fluctuations are the norm. The range for offense and retreat needs to be gradually narrowed. Currently, the daily chart shows a bearish candle, which lacks sufficient strength, and we need to wait for the market to clarify further. In the evening, we should look for offensive positions from a shorter timeframe. Friends who have ideas can communicate with me in advance! Lastly, I remind everyone that the long-term perspective does not consider it a peak.

Yi Hai Lun Bi: The success of investment depends not only on choosing good assets but also on when to buy and sell. Preserving capital and making good asset allocations are essential for steady progress in the ocean of investment. Life is like a long river flowing into the sea; the determining factor in victory or defeat is never just the gains and losses of a single pass or the profits and losses of a moment, but rather the convergence of many rivers!

This article is merely a personal opinion and does not constitute any trading advice. The crypto space has risks, and investment should be cautious!