It seems like I have dug a pit for myself recently

Since the last time I wrote an analysis post on the impact of interest rate cuts expectations

It mentioned that we need to consider stablecoin market cap, ETF funding situation, USD index and other indicators together

Then I kept a pace of researching one indicator each day, analyzing them one by one

But now I find this project too huge

The relationship between individual indicators and crypto is theoretically clear

But in reality, it's another story

From the ETF perspective, the possibility of continued correction is relatively high

1. Medium-term indicators

The market value of stablecoins analyzed earlier, along with the total net inflow and outflow of ETF funds, belongs to medium-term indicators, suitable for observing liquidity trends.

The conclusion has been provided at the beginning of the previous post:

1. The market value of stablecoins is steadily and slightly increasing - indicating that the crypto money is on the sidelines, ready to buy the dip at any moment.

2. The total holdings of ETFs have started to decline since October, stabilizing slightly from 11.25 with minimal growth.

Combining this, I preliminarily feel optimistic about the medium-term, which is the next 1-6 months.

Right now, this is a phase of pullback, far from entering a bear market.

But I need to combine the risk preference data tomorrow to arrive at a more accurate long-term judgment.

2. Short-term indicators

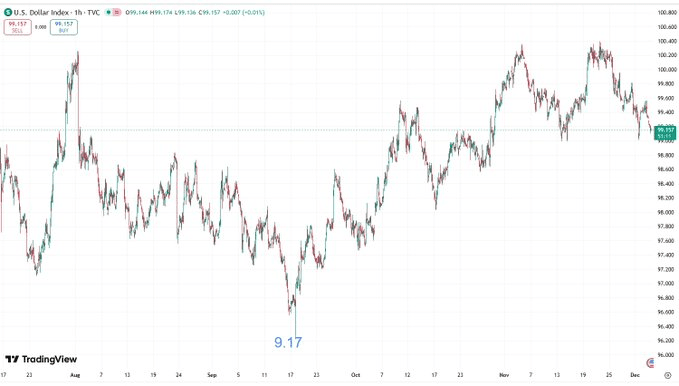

I have prepared three short-term indicators - the US Dollar Index (DXY), daily total net inflow and outflow of ETFs, OI + Funding.

The US Dollar Index is easy to understand; it's a weighted index of the US dollar against other fiat currencies like the Japanese yen and the South Korean won.

The reason is that crypto is priced in USD; when DXY strengthens, it becomes unprofitable for countries other than USD-based ones to invest in crypto, which is bearish for crypto.

Let's first look at the most recent data; the two time points marked in the chart correspond exactly to the initial bottom points of BTC's phase, but they are quite close in time, making it difficult to provide predictive value.

However, the cycle that short-term indicators can achieve is just within one month; it's definitely not real-time. Extending the cycle slightly, DXY's inverse relationship is still quite useful.

We all know that the recent round of pullback started on 10.8, while DXY gave a signal on 9.17, when BTC was priced at 11.5W.

Moreover, looking back at the last true bear market in 2022, it was indeed a year of DXY strengthening, and the reversal signal for BTC came three months earlier.

What's interesting is that the crypto market is influenced by multiple factors, and the relationship between indicators and crypto is theoretically always valid.

However, this does not prevent occasional failures, which require the integration of other relevant indicators for comprehensive judgment.

The interesting and challenging aspect of prediction models lies here; it's not a game of hitting the target in one shot, but rather a matter of probability.

If all indicators never deviate, then everyone would be making money (and simultaneously, no one would be making money, as there would be no opponents).

Similarly, comparing the recent dip to a very similar one at the beginning of this year, from January to April, DXY did not exhibit an inverse relationship with BTC, but instead showed a period of moving in the same direction.

This is quite interesting, but friends who have read my previous two posts will notice.

The research on the market value of stablecoins and ETF-related data is still operating normally.

3. Prediction models

As I mentioned earlier, all indicators cannot be used individually or mechanically; a complete yet uncomplicated prediction model needs to be constructed.

Today I wrote down three medium-term and three short-term indicators, and prepared two long-term indicators.

Tomorrow, I will first study the missing risk preference data for medium-term indicators and gradually supplement the short-term and long-term data.