Some friends have asked whether the rate cut in December means all good news has been exhausted. I actually believe that, macro-wise, the bad news may have indeed been exhausted.

Of course, it may not necessarily rise; the end of bad news does not mean that there will definitely be good news.

┈┈➤ The Federal Reserve may implement intermittent rate cuts.

╰┈✦ Stop tapering.

First, the Federal Reserve will stop tapering on December 1. Subsequently, whether through intermittent rate cuts or continuous rate cuts, the dollar easing cycle will officially begin.

╰┈✦ Tight funding flow in commercial banks is one of the motives for rate cuts.

This topic has been discussed before, but there is one question that no one has asked: why, in a high-interest environment, when commercial banks can absorb more deposits, is there still funding tightness?

In a high-interest environment, the cost for commercial banks to obtain funds is high, and based on this, the profit margin for lending those funds is relatively small. Therefore, there will be times when funding flows are locally tight.

Especially in the current high-interest environment, it is not due to an overheated economy, so it is relatively more difficult for commercial banks to lend out.

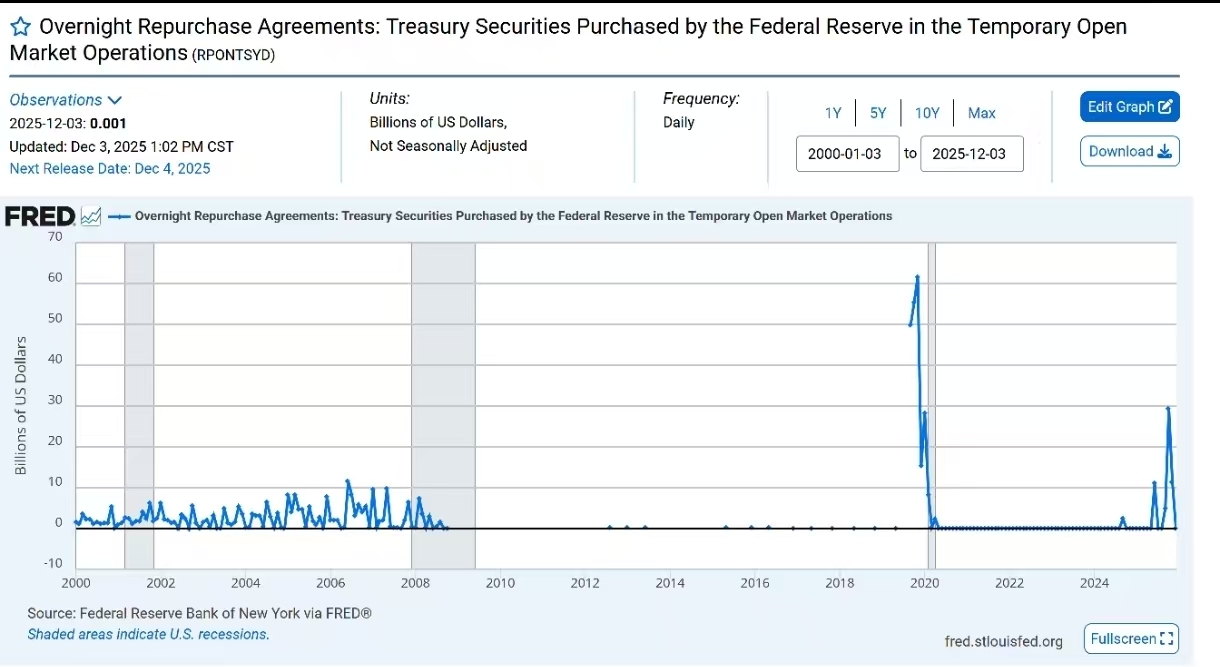

In fact, this is not the first large overnight repo recently. In June this year, there was a $11 billion repo, and in October there was a $29.4 billion repo, plus the recent $13.5 billion temporary output to the banking system, indicating that the U.S. commercial banking system is currently experiencing significant funding pressure.

In fact, after 2000, there was a similar situation that occurred between November 2019 and April 2020, which was also at the beginning of rate cuts. However, at that time, the scale of overnight repos was larger, and the rate cuts that started in 2020 almost brought rates down to 0, while also initiating unlimited QE.

Therefore, the funding shortage that appears during the banking system's settlement, from this perspective, gives the Federal Reserve a certain motive for rate cuts.

╰┈✦ Weakness in the job market is the second motive for rate cuts.

Secondly, the two key factors affecting the Federal Reserve's path for rate cuts are employment and inflation.

Although the U.S. government is in a shutdown, economic data releases are delayed. However, third-party institutions will still have data and reports to publish.

The U.S. ADP employment figures are published jointly by the Automatic Data Processing Company and Stanford University's Digital Economy Laboratory, which is what we usually refer to as the small non-farm payroll. Basically, the overall trend is not much different from the non-farm employment data, both showing a general downward trend. Furthermore, the November ADP employment figure was far below expectations and was negative.

Together with previous reports from Goldman Sachs, they all point to one thing: the weakness of the U.S. job market.

Therefore, unless CPI rebounds, the Federal Reserve will likely adopt an easing monetary policy.

There are three potential paths for the Federal Reserve in the first half of 2026:

First, continuous rate cuts. If the job market is very poor and there is a massive wave of layoffs as reported by Goldman Sachs, then the Federal Reserve may lean towards this.

Second, intermittent rate cuts. Cut rates while observing. If the job market is somewhat poor, the Federal Reserve may lean towards this situation.

Third, there will be no rate cuts in the first half of 2026. If CPI rebounds, the Federal Reserve may lean towards this situation.

╰┈✦ CPI poses a slight resistance to rate cuts.

From the perspective of the job market, as long as there are no rate cuts, the probability of a short-term rebound in CPI is low. Logically, with poor employment, consumption will not be very strong; after all, poor employment generally means that consumer income is not optimistic.

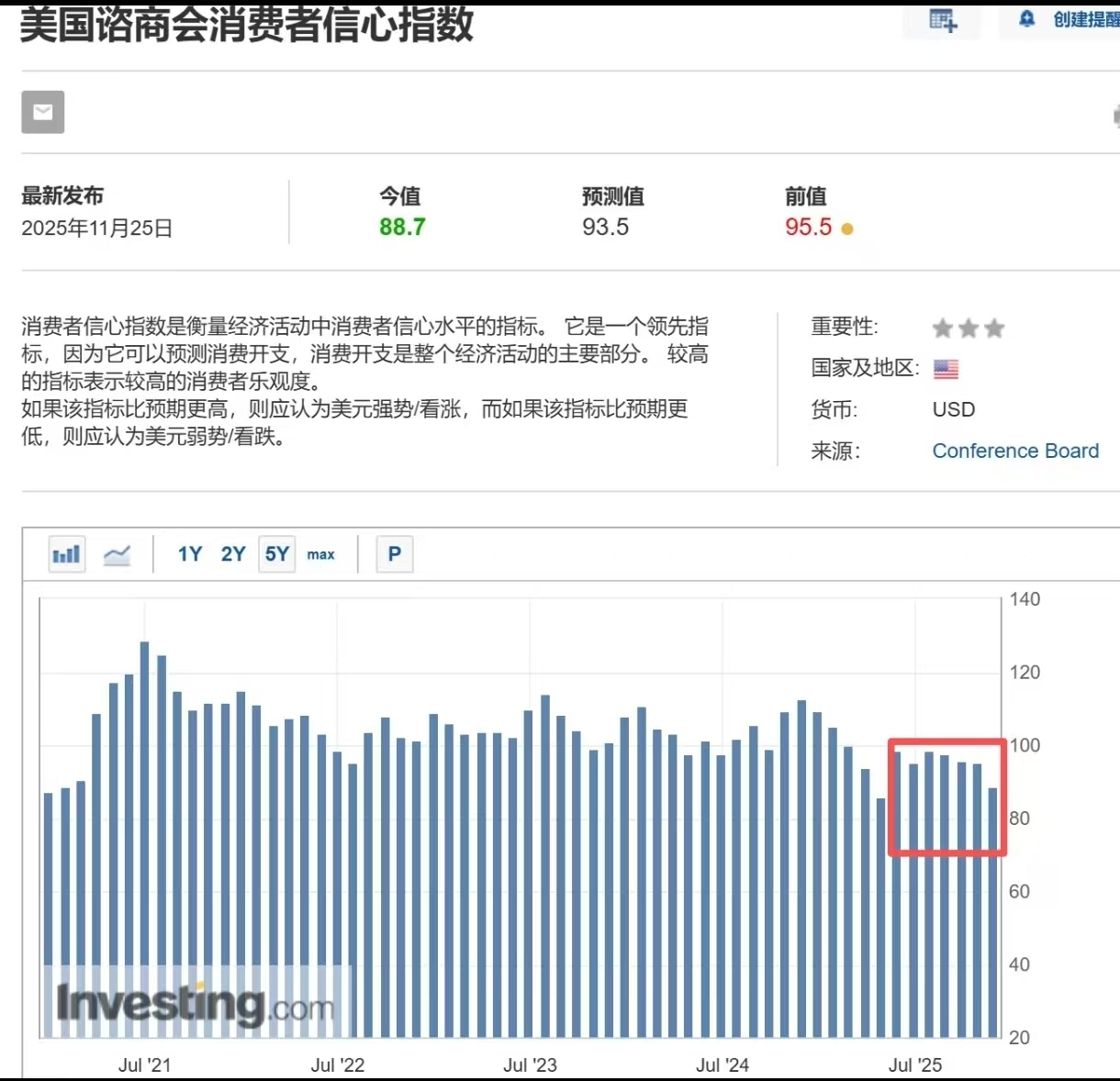

The consumer confidence index shows that since May of this year, consumer confidence has been relatively low.

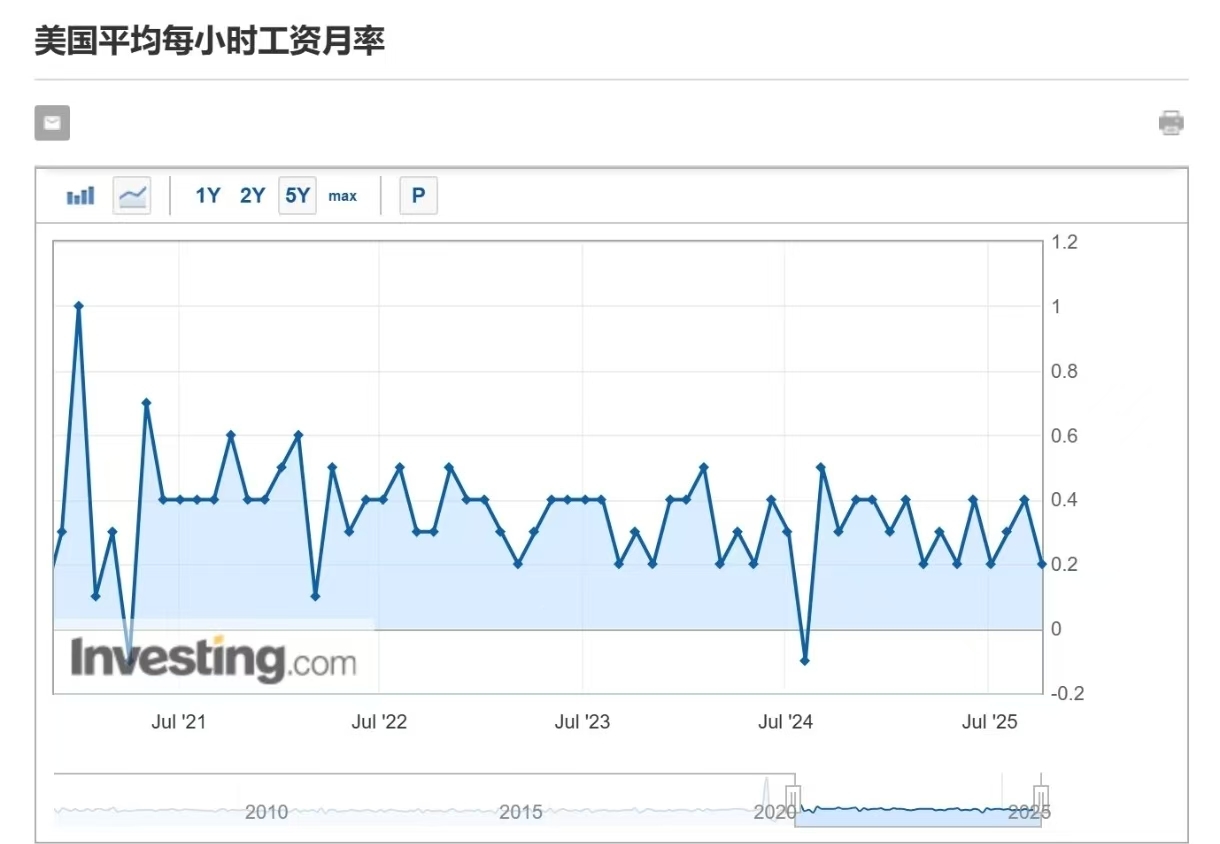

Additionally, wages are one of the main components of production costs. There is no growth trend in monthly wage rates.

All of these indicate that there will be no rate cuts and it will be difficult for CPI to rebound.

However, removing the high inflation phase of 2021 to 2022, wages also do not show a significant downward trend. Therefore, CPI still poses some resistance to rate cuts, and there is concern that rate cuts will lead to a rebound in CPI.

It is speculated that the Federal Reserve is more likely to adopt the second plan mentioned earlier, which involves intermittent rate cuts.

Cut the rate a bit and then observe the recovery of the job market and whether inflation rebounds before considering the next steps.

┈┈➤ The trade war has cooled down.

The trade war between Trump and other countries has cooled down. Ultimately, the U.S. imposed a 20% tariff on China, and China imposed a 10% tariff on the U.S. Trump is very likely to visit China in the first half of next year.

The tariffs imposed by the U.S. on Mexico and Canada mostly come with exemptions for many goods.

Since then, the risks posed by the trade war to U.S. prices and exports have basically been lifted.

┈┈➤ The negative impact of Japan's rate hike has already been released.

As a safe-haven currency, the yen's rate hike in Japan also has a certain impact. However, currently, this negative news has already been released in advance, and there is no need to wait until December 18. The U.S. stock market and crypto have already declined in advance.

The U.S. will cut rates by 25 basis points in December, releasing liquidity.

Japan will raise interest rates by 25 basis points in December, potentially absorbing liquidity as a safe-haven asset.

However, given the large scale of the U.S. economy, the liquidity released by rate cuts should be greater than that released by Japan's rate hike. Therefore, it should not have a very negative impact on market liquidity.

┈┈➤ Trump is about to enter the midterm election year.

Trump currently has a lawsuit regarding the legality of his tariff imposition by the Supreme Court. His tariff policy has basically stabilized. Therefore, whether he wins or loses, it is likely he will not impose additional tariffs. On the other hand, Trump has previously indicated that if he loses, he will push for legal amendments to give the president more authority in trade and other areas. However, this matter will not be passed immediately and may not have a direct impact on the economy, market, or U.S. stocks.

Although some people think Trump is like a child, and some think that as long as Trump is around, there will always be black swans.

However, in fact, Trump has indeed been more low-key recently. Even the latest threat to raise tariffs and call for rate cuts, made at the end of October, was from Treasury Secretary Mnuchin.

Trump's recent remarks are primarily aimed at pushing the stock market to new highs and announcing candidates for the new Federal Reserve chair. It seems Trump is beginning to shift his focus from tariffs, trade wars, and international politics to the U.S. stock market and rate cuts.

Trump even joked in late November that if Mnuchin could not solve the problem of the Federal Reserve not cutting rates, he should fire him.

Overall, it is speculated that Trump is preparing for the midterm elections by reducing extreme statements and actions while promoting rate cuts and other market and voter-friendly measures.

┈┈➤ There is some suspense regarding the healthcare-related budget bill.

The only remaining suspense is the previously contentious healthcare-related budget bill, which will be voted on this month. If no consensus can be reached by January 30, the short-term funding will run out, and the U.S. government will face another shutdown.

However, this possibility feels small, given that both parties do not want the government to shut down again.

However, this matter also has its suspense and requires continuous attention.

To summarize, the suspense surrounding a rate cut in December is quite small.

Significant event in December, the dot plot.

Currently, the CME's interest rate futures indicate that the market expects two rate cuts in 2026, in March and July. Yesterday, the prediction was for March and September.

This means that the market’s expectations for rate cuts have been brought forward.

If the dot plot on December 10 predicts that the interest rate at the end of 2026 will be below 3% to 3.25%, it would align with expectations and pose no negative news.

If the dot plot predicts that the interest rate at the end of 2026 will be between 2.75% and 3%, it is slightly better than expected, which is somewhat positive.

If the dot plot predicts that the interest rate at the end of 2026 will be between 2.5% and 2.75%, it is somewhat better than expected, which is positive.

If the dot plot predicts that the interest rate at the end of 2026 will be even lower than 2.5%, it would be much better than expected, which would be very positive.

Of course, the market expectations may change before December 10, which is something to note. But at this point in time, with poor employment, the Federal Reserve cannot predict only one rate cut in 2026. Therefore, disregarding the short-term impact of the dot plot on that day, the likelihood of the dot plot indicating bad news in December is quite low.

In the first half of 2026, it is speculated that the likelihood of intermittent rate cuts is high, while the likelihood of continuous rate cuts is low (but this probability is increasing), and the very small probability of no rate cuts or hikes in the first half of 2026. This kind of intermittent rate-cutting environment is certainly not conducive to a bull market, but it also does not align with a bear market.

While the trade war has cooled down, expectations for a rate hike in Japan have been released early, and Trump has begun preparing for the midterm elections. Although these matters cannot be said to be positive, macro-wise, it seems the bad news has been mostly exhausted.

In addition to paying attention to the voting on the healthcare budget-related bills from both parties, there should not be any significant negative news macro-wise in the near future.

Of course, even significant positives may not materialize; it will require continuous rate cuts from December to March to accelerate the release of liquidity.