1. Why Layer 2 Became the Main Battleground

After years of “up and down with the cycle”, the Ethereum story is no longer just about high gas fees. The real question now is:

Which Layer 2 becomes the main street for users and liquidity?

L2s are no longer “experiments” – total TVL across L2s is now in the tens of billions of USD.

Rollups are roughly split into two major camps:

Optimistic Rollups: Arbitrum, Optimism, Base, etc.

zk-Rollups / zk-EVM: zkSync Era, Starknet, Linea, etc.

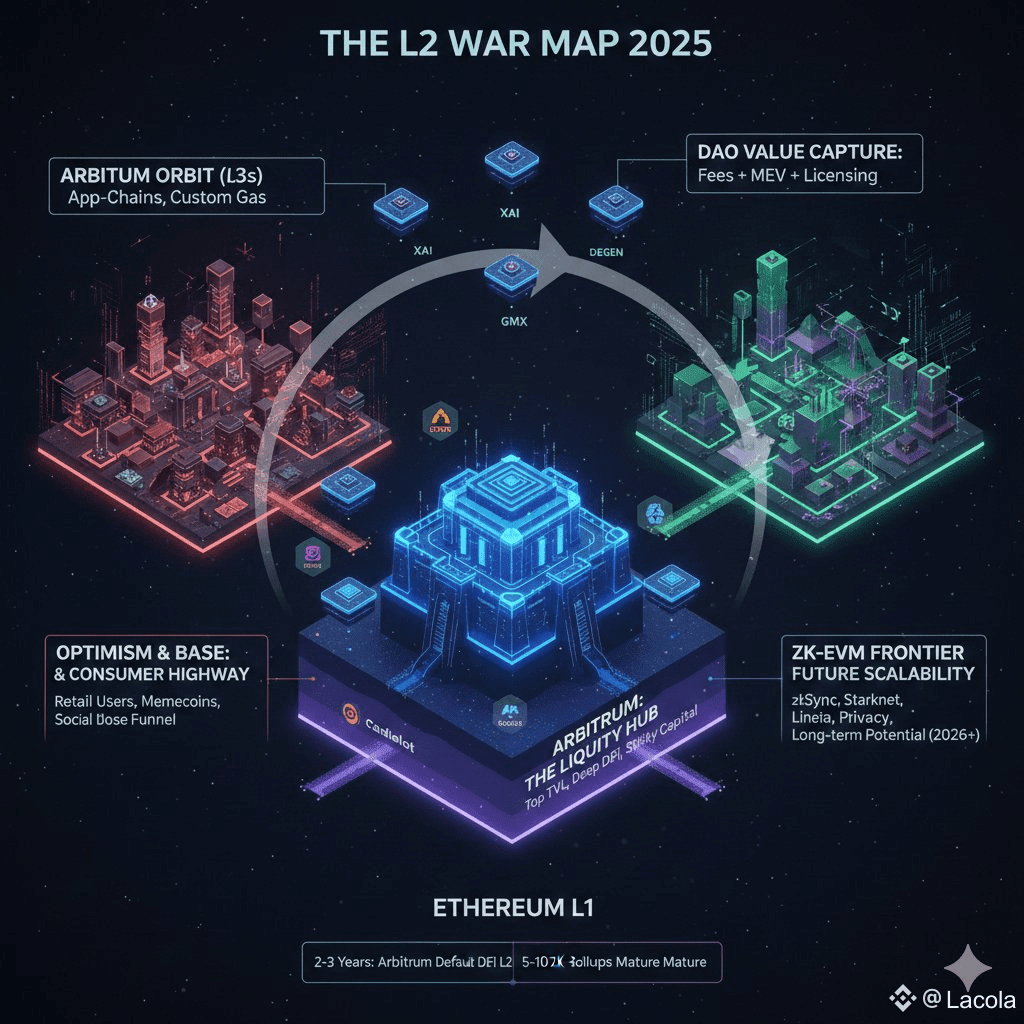

In that picture, Arbitrum used to be the clear dominant player, and even in 2025 it remains one of the top L2s by TVL and ecosystem depth—although the game is no longer the “one-horse race” it was in 2023–2024.

2. By the Numbers: Where Does Arbitrum Stand Among L2s?

Looking at recent aggregates:

Arbitrum consistently ranks as one of the top L2s by TVL, often in the #1–#2 range, depending on methodology.

Base and Optimism follow behind, while zkSync, Starknet, Linea and others are catching up from a lower TVL base.

Different data sources (L2Beat, DeFiLlama, CoinGecko, etc.) show different absolute TVL because they track slightly different things (TVL vs “secured value”, what they count as DeFi TVL, etc.).

The exact leaderboard (whether Arbitrum is #1 or #2 on a given day) is less important than this fact:

Arbitrum is firmly in the top tier of L2s by security, TVL, trading volume and number of active DeFi protocols.

In practice, it behaves as a core hub for DeFi liquidity on Ethereum L2, not a small satellite chain.

3. Arbitrum Within the Optimistic Rollup Camp (vs Optimism & Base)

Inside the Optimistic Rollup camp, the big three are Arbitrum, Optimism and Base.

They share similar roots but have very different positions and strategies:

Arbitrum

Clearly positioned as a DeFi & liquidity hub: GMX, Radiant, Camelot and a long tail of DEXs, perp DEXs, lending and derivatives make up a large chunk of TVL.

Focuses on a deep protocol ecosystem catering to traders, farmers, perp degens, LSD/LRT users and structured products.

Its liquidity is relatively sticky: TVL remains meaningful even after big incentive programs cool down.

Optimism

Leans heavily into the Superchain + public goods narrative.

OP Stack is open for many chains, and RetroPGF is a major pillar of its brand.

Its ecosystem skews more toward “Ethereum-aligned infra and public goods”, with DeFi TVL typically lower than Arbitrum or Base.

Base

Has a major advantage via the Coinbase funnel: strong on-ramp, retail users, memecoins, social apps, NFTs and consumer-facing products.

Base has grown extremely fast, and at times has overtaken Arbitrum on certain DeFi TVL metrics, but its TVL profile is more skewed toward memecoins and consumer apps.

Simplifying the Optimistic camp:

Arbitrum = DeFi & liquidity depth

Optimism = Superchain + public goods + governance experiments

Base = Coinbase-powered consumer highway

Arbitrum’s role in this trio is the “DeFi-native L2”—the home of capital-intensive and more complex financial protocols.

4. What About zk-Rollups & zk-EVM?

On the zk-rollup / zk-EVM side, names like zkSync Era, Starknet and Linea are growing fast but still start from a smaller base in terms of DeFi TVL and ecosystem maturity.

Technically, zk-Rollups are strong on:

Proof-based finality and strong security guarantees.

Long-term potential for privacy, scalability and cross-rollup composability.

But if we take a snapshot of today:

UX & tooling are often rougher than Optimistic L2s (bridges, wallets, dev tooling, ecosystem integrations, etc.).

Their DeFi ecosystems are not as deep as Arbitrum’s: fewer battle-tested blue-chips, thinner liquidity, many protocols still in early stages.

The key nuance:

Over a 5–10 year horizon, zk-rollups may become the “default” infrastructure layer.

Over the next 2–3 years, Arbitrum is still a production-ready default for DeFi with real volume and real fee-generating DApps.

5. Arbitrum’s Unique Edge: Beyond a Single L2, It’s a Stack

Arbitrum is not just Arbitrum One. It’s an entire stack:

Arbitrum One – the main general-purpose L2 with heavy DeFi presence.

Arbitrum Nova – optimized for ultra-low fees, suited for gaming, social and content-heavy apps.

Orbit & L2/L3-as-a-Service – teams can spin up their own chains using the Arbitrum tech stack, while still connecting to Arbitrum’s infrastructure and liquidity.

From the DAO & revenue point of view, Arbitrum is starting to diversify its income streams:

Transaction fees from blockspace.

Timeboost auctions – selling transaction ordering priority, capturing part of MEV.

Orbit licensing fees – revenue from projects using the Arbitrum stack.

Potential treasury yield from managing the DAO’s large capital base.

This shifts Arbitrum’s role from “just another L2” to an ecosystem of chains and infra stack—closer to an “L2 platform” than a single network.

6. The Challenges: This Is No Longer a Winner-Takes-All Game

Even though Arbitrum’s current position is very strong, the L2 war has clearly moved into a new phase:

Direct competition from Base & Optimism

Base has grown extremely quickly, sometimes overtaking Arbitrum in certain DeFi TVL snapshots.

Optimism is pushing the Superchain vision, with many appchains/L2s building on OP Stack and reinforcing its network effect.

Long-term pressure from zk-Rollups

Starknet, zkSync, Linea and others are growing at high percentage rates from a small base.

As their UX improves and more blue-chip apps migrate or deploy there, liquidity can gradually shift.

Liquidity and user fragmentation

The more L2s, L3s and appchains exist, the more liquidity and users get fragmented.

Arbitrum needs to maintain its role as a liquidity hub, instead of allowing TVL to be overly diluted across many competitor chains and its own Orbit/appchain ecosystem.

7. Conclusion: Where Does Arbitrum Sit on the L2 Map?

If we draw the L2 war map today, we can summarize:

On TVL & DeFi depth:

→ Arbitrum remains firmly in the top tier (#1–#2) and acts as a DeFi hub for Ethereum L2.

On ecosystem strategy:

→ Arbitrum is no longer just a single rollup. It is an Arbitrum stack: One, Nova, Orbit, plus emerging fee/MEV/licensing and treasury strategies.

On future competition:

→ Over the next 2–3 years, Arbitrum is likely to remain the default L2 for DeFi.

→ Over the next 5–10 years, it will have to compete hard with zk-Rollups and high-performance L1s / Parallel EVM chains to avoid being commoditized as just one L2 among many.

From the perspective of a researcher or airdrop/retroactive hunter:

The key question is no longer “Will Arbitrum win?”

It’s “How much of the multi-L2 world’s liquidity and fees will Arbitrum capture — and who actually captures that value?”

ARB holders?

DeFi protocols on Arbitrum?

Or the Orbit/appchain layer built on top of the Arbitrum stack?

That’s where the real alpha lies.