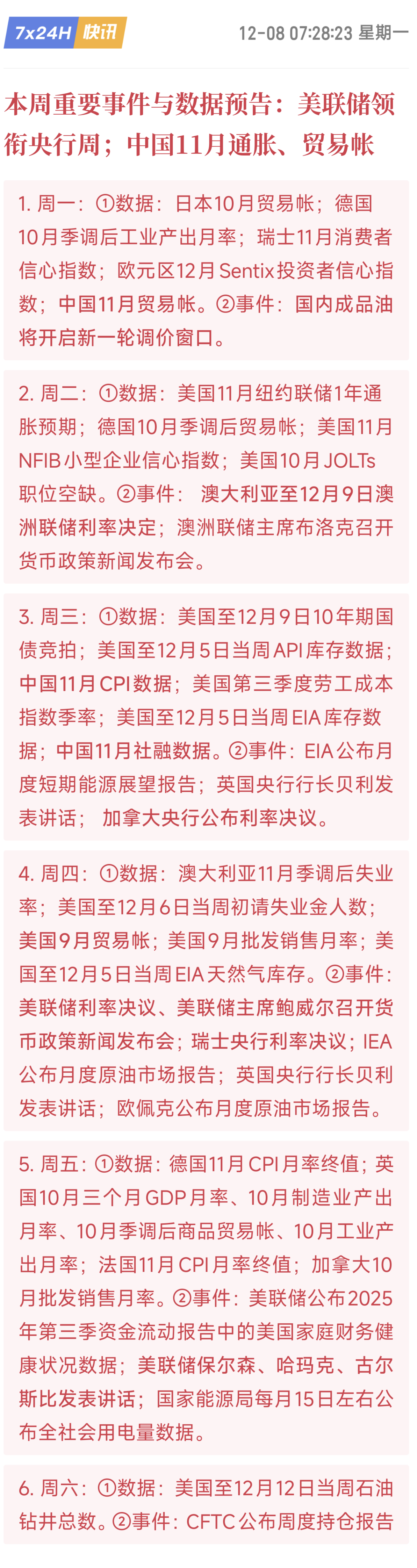

The second week of December will become a key window for the global financial markets at the end of 2025. Centered around the Federal Reserve's interest rate decision, the central banks' intensive actions, combined with the concentrated release of inflation, trade, and employment data from major economies such as China, the U.S., and Europe, will comprehensively affect market trends from the perspectives of liquidity, fundamentals, and commodity pricing, with the volatility of various assets likely to rise significantly.

1. Federal Reserve Decision: The 'anchor' of the market this week

Thursday (December 11) the Federal Reserve interest rate decision and Powell's press conference are the absolute core events of this week. The current market pricing for interest rate cuts is relatively sufficient, but the key points of the decision are three:

1. Rate Adjustment Magnitude: The mainstream market expectation is a 25 basis point cut, but we need to be wary of “holding steady” or “unexpectedly cutting 50 basis points” black swans;

2. Dot Plot Guidance: The description of the rate cut path for 2026 will directly affect the US dollar index, US Treasury yields, and risk asset pricing; if it signals a “slowing rate of cuts”, it may trigger a pullback in risk assets;

3. Inflation and Employment Statements: Powell's evaluation of US inflation stickiness and labor market resilience will change the market's judgment on the monetary policy cycle, which will then transmit to cryptocurrencies, crude oil, stock markets, and other areas.

Historically, before the Federal Reserve's decision is made, the market is usually cautious; after the decision, there is often volatility driven by “expectation gaps” — if the policy is dovish, a weaker dollar will benefit dollar-denominated crude oil and cryptocurrencies; if hawkish, it may trigger a global sell-off in risk assets.

2. Intensive Actions by Multiple Central Banks: Global Liquidity Pattern Rebalancing

Besides the Federal Reserve, this week the Reserve Bank of Australia (Tuesday), the Bank of Canada (Wednesday), and the Swiss National Bank (Thursday) will successively announce their interest rate decisions, forming a “Central Bank Week” pattern:

Reserve Bank of Australia: Current market expectations suggest it will maintain interest rates, but we need to pay attention to Chairman Philip Lowe's statements on Australian inflation and economic growth; if he signals a hawkish stance, the Australian dollar and Australian commodities may react.

The Bank of Canada: Canadian inflation is still above target; if this decision suggests a rate hike or delays a rate cut, it may strengthen the Canadian dollar, thus affecting the pricing of crude oil (Canada being a major oil producer);

Swiss National Bank: Having previously cut rates multiple times to release liquidity, if it continues to ease this time, the Swiss franc's depreciation may indirectly boost demand for safe-haven assets.

The differentiation of policies among central banks in various countries will exacerbate volatility in the foreign exchange market, while exchange rate fluctuations will inversely affect cross-border capital flows, creating secondary transmissions to stock markets and major commodities.

3. Core Economic Data: The “Two-Way Verification” of US and China Fundamentals

This week, key data from the US and China will be unveiled, becoming an important basis for judging the economic fundamentals:

1. China Data: Inflation, Trade, Social Financing Three Lines of Force

November Trade Balance (Monday): Export data reflects external demand resilience, while import data reflects internal demand recovery; if exports exceed expectations, RMB assets may receive support.

November CPI (Wednesday): The CPI trend relates to domestic inflation expectations and monetary policy space; if it remains low, market expectations for “increased stability growth policies” will heat up;

November Social Financing (Wednesday): The scale and structure of social financing directly reflect the strength of credit expansion; if the increment of social financing exceeds expectations, it will boost market confidence in China's economic recovery.

2. US Data: Employment and Inflation Expectations Become Key

November New York Fed 1-Year Inflation Expectations (Tuesday), Q3 Labor Cost Index (Wednesday): Inflation expectations and wage costs are core concerns for the Federal Reserve; if data increases, it may strengthen hawkish expectations;

October JOLTs Job Openings (Tuesday), Initial Jobless Claims (Thursday): Employment data reflects the heat of the labor market; if job openings decrease and initial claims increase, it suggests a cooling labor market, increasing pressure on the Federal Reserve to cut rates.

The “one increase and one decrease” or “double strong and double weak” in US-China economic data will directly affect the market's judgment on global economic growth, thus changing risk preferences — if Chinese data is good and US data is weak, funds may flow into emerging market assets; conversely, they may revert to dollar assets.

4. Key Data on Major Commodities: Reassessing the Logic of Crude Oil Pricing

This week, the crude oil market will face multiple data/event shocks:

EIA Inventory Data (Wednesday), EIA Short-Term Energy Outlook Report (Wednesday): Changes in inventory reflect the supply-demand structure, and the outlook report influences the market's judgment on the medium- to long-term trends in oil prices;

IEA, OPEC Monthly Oil Reports (Thursday): The forecasts of the two major institutions regarding global oil supply and demand will directly dictate short-term oil price trends; if they lower demand expectations, oil prices may come under pressure;

US Total Oil Rig Count (Saturday): The number of rigs reflects the willingness to produce shale oil in the US; if the number increases, it suggests increased pressure on the supply side, which is bearish for oil prices.

With the impact of the Federal Reserve's decision on the US dollar, crude oil prices this week are likely to experience volatility driven by both “policy and supply-demand” factors, and we need to be wary of the intense fluctuations caused by the interplay of bullish and bearish factors.

5. Market Operation Insights: Focus on Core Conflicts, Prevent Volatility Risks

1. Short-Term Rhythm: Before the Federal Reserve's decision, prioritize observation or light positions to avoid premature speculation; after the decision, adjust positions based on the “policy expectation gap”;

2. Asset Allocation: If the Federal Reserve is dovish, focus on dollar-denominated assets like crude oil and Bitcoin; if hawkish, prioritize allocation to safe-haven assets like gold;

3. Data Focus: Key tracking of China's CPI/social financing and US inflation expectations/employment data; when fundamentals exceed expectations, adjust judgments on related assets in a timely manner.

Overall, the core contradiction in the market this week is the “Federal Reserve policy expectation gap”, coupled with the resonance of multiple central banks and core data, the volatility elasticity of various assets will significantly increase, and investors need to focus on core variables while hedging risks.