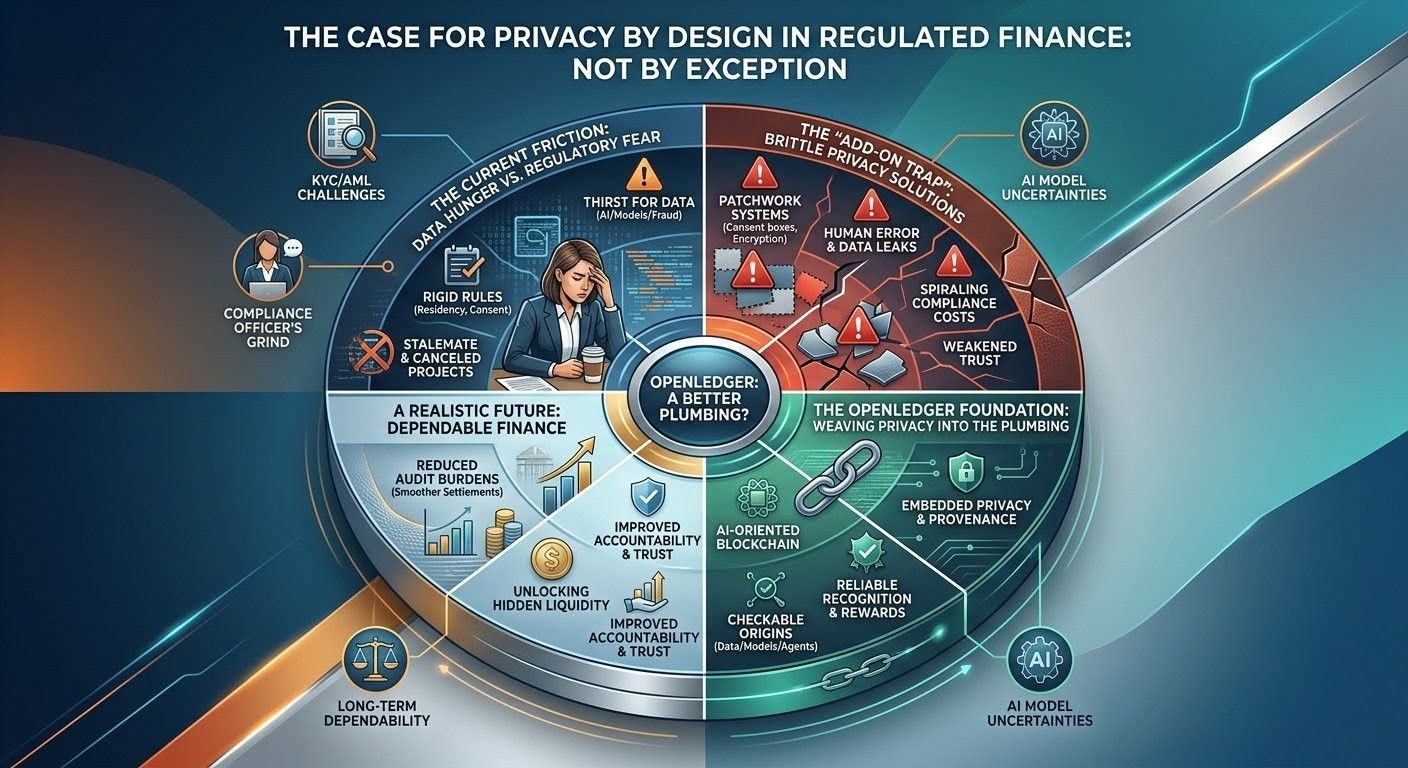

Lately I keep coming back to this tension I see playing out in back offices and risk meetings everywhere. I picture a tired compliance officer at a mid-sized lender—maybe in London, or Singapore, or even right here in Karachi where cross-border wires bring their own pile of extra worries. She's sitting there, coffee going cold, staring at another promising dataset she needs to train a decent credit model or flag odd payment patterns. On paper it looks useful, maybe even game-changing for the team, but the moment she thinks about bringing it in, her stomach tightens. One sloppy data merge, one missed consent line, and she's the one in the hot seat explaining it to regulators or calming down customers whose information somehow leaked through a vendor chain.

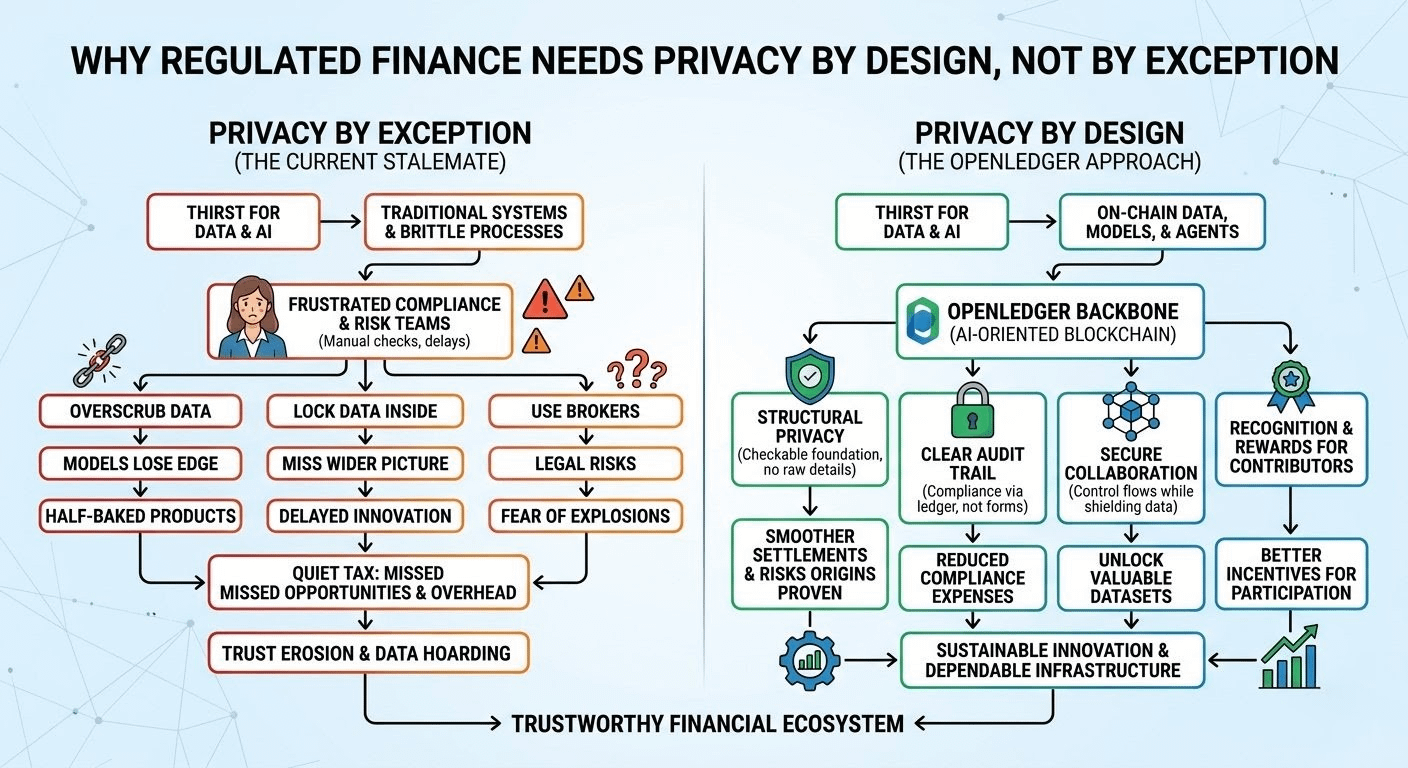

That's the everyday kind of friction that really sticks with me after all these years. Regulated finance has grown incredibly thirsty for data. Loan approvals, balancing portfolios, catching fraud, or letting AI agents run market simulations—everything leans on pulling in richer, fresher information. Yet the privacy rules, residency laws, and audit demands feel like they were written for simpler times, before AI started reshaping everything. So people muddle through with compromises that never sit quite right. You scrub the data so hard the model loses its edge. You lock it all inside your own four walls and miss the wider picture. Or you sign thick contracts with brokers and hope nothing explodes later. I've watched solid product ideas get delayed for months because legal couldn't sign off on the data trail. The builders get worn out, trim their ambitions, and ship something safe but half-baked. Customers feel the caution and hold back, sharing less than they might, and the whole system ends up a bit weaker for it.

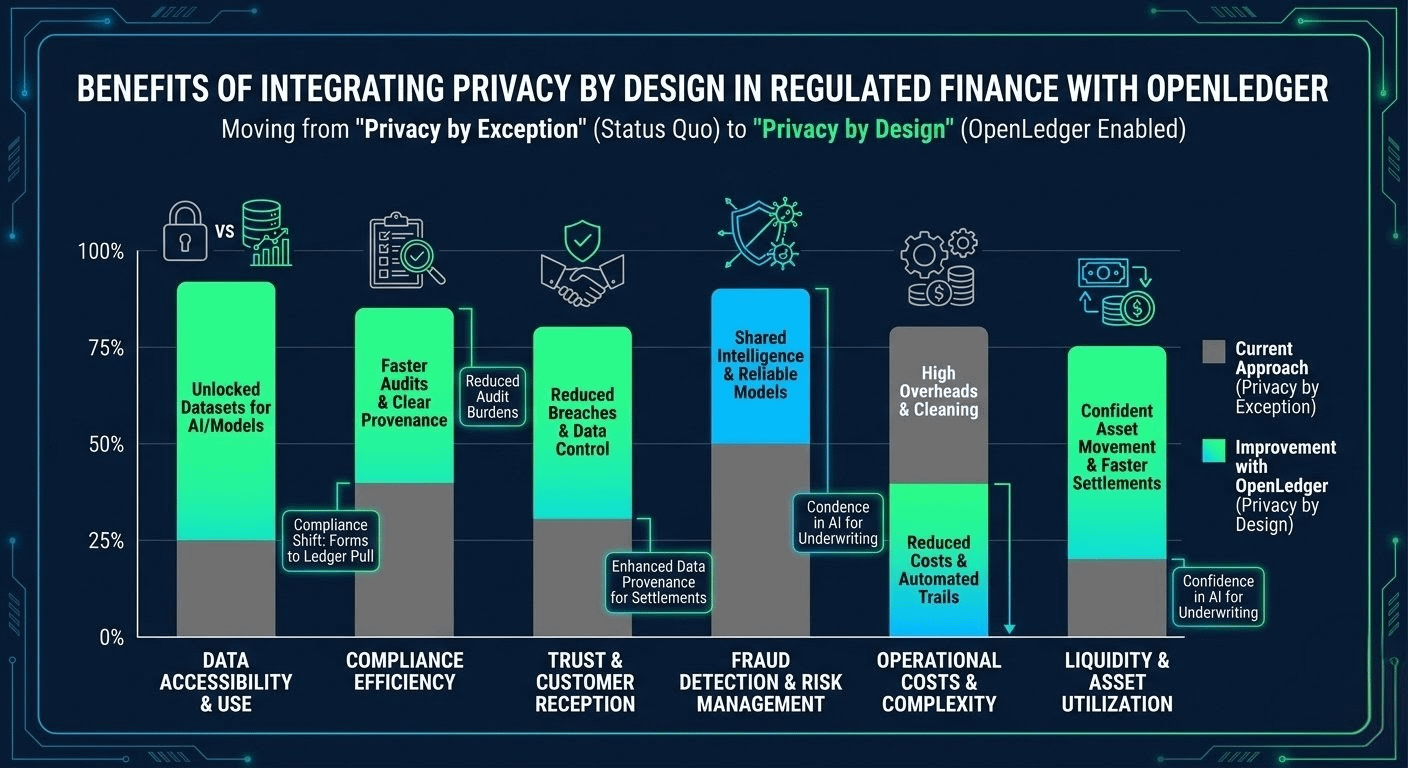

What really bothers me is how most so-called solutions treat privacy as an add-on, something you scramble to activate when the auditors arrive. You design the core for speed and smarts first—quick calculations, shared liquidity, team model training—then patch on logs, consent checkboxes, and whatever encryption fits the budget. In practice, it frays fast. Someone pulls a data slice for "quick testing," a contractor's login stays active too long, or a model update quietly swallows fields it shouldn't. Settlements drag on because reconstructing events becomes a messy investigation. Compliance expenses keep rising with all the hand-checking and insurance. And humans being humans, we cut corners under pressure. Every big breach in the headlines chips away at trust, so institutions just cling tighter to their own mediocre internal data rather than risk real collaboration.

I've sat through enough post-mortems on failed systems to stay deeply skeptical. The contradictions run deep. Regulators want stronger risk controls, which need good data, but they also push hard for data minimization that leaves models starving. It creates this exhausting stalemate where liquidity gets trapped. Valuable datasets and trained models gather dust because no one can confidently use or pay for them without legal risks hanging overhead. It feels like a quiet tax we're all paying in missed chances and unnecessary overhead.

This is the space where OpenLedger makes me pause—not as the next big crypto hype, but as possible background plumbing that might ease some of the grind. It's an AI-oriented blockchain meant to let data, models, and agents interact on-chain while keeping decent track of contributions and usage. I don't see it as magic. I look at it like I'd inspect new pipes in an old building: will it actually stop some of the daily leaks?

The part that feels promising is how it tries to weave privacy into the structure itself rather than slapping it on afterward. Instead of crossing your fingers that audit trails survive scrutiny, basic facts about where data came from, how models were shaped, and how they're used could be checkable at the foundation level. For teams handling settlements, that might translate to smoother closes when you can prove a risk score's origins without dumping raw sensitive details. Compliance could shift from endless forms to pulling a clear record off the ledger. Costs might lighten if you're not forever paying go-betweens or cleaning up messes. And for the people side, contributors of data or computing power might get more reliable recognition and rewards, which could slowly change habits away from the usual hoarding or free-riding.

Still, I know the real world pushes back hard. KYC and AML rules demand real names and identities in many cases, especially with the cross-border work that's everyday reality in places like this. Regulators won't accept on-chain evidence without kicking the tires thoroughly in live situations. True privacy by design would mean building smart, controlled flows—letting valuable stuff circulate while shielding what must stay protected—rather than naive all-open or all-locked extremes. Success hinges on the chain staying solid and laws gradually treating those proofs as valid.

I'm not completely convinced it all fits neatly. Blockchains carry transparency risks—if not handled carefully, they might enable new kinds of indirect snooping. AI models wander and get retrained in chaotic ways, so maintaining clean attribution through changes isn't straightforward. Bringing regulated players on board takes forever: endless testing, procurement mazes, and built-in suspicion of anything decentralized. If it stays too rooted in crypto culture, many will simply keep their old setups running in the background.

Even after all that, having watched too many brittle systems crack, this feels like a realistic angle. The people most likely to try it are the compliance and risk teams exhausted by today's constant drag—banks and insurers experimenting with alternative data, groups pooling fraud detection models, or developers building focused agents for underwriting or oversight. They'd reach for it when strong provenance eases real audit burdens or unlocks data that felt too dangerous before. It might succeed by treating privacy and liquidity as connected challenges instead of opposites—helping value move without the usual spills or paralysis. That could bring down long-term costs, improve accountability, and open doors for smaller contributors adding local flavor from markets big systems often ignore.

It could fall short in predictable ways: if plugging into legacy tech feels too painful, if regulators flatly reject the approach, or if incentives don't actually deliver for people putting in the work. Or it ends up as yet another side project the major players simply bypass for their private gardens.

In the end, this isn't revolutionary fireworks. It's more like gradually lightening the load that makes moving money and handling real risks feel heavier than necessary. I've been in enough late-night reviews where we all agreed the current setup was creaky but lacked a better base. If OpenLedger becomes steady, behind-the-scenes infrastructure that turns privacy from a daily workaround into something naturally part of the system, that would be meaningful. Not flashy. Just dependable. And in finance, the dependable, trustworthy pieces have a habit of lasting longer than the exciting ones.