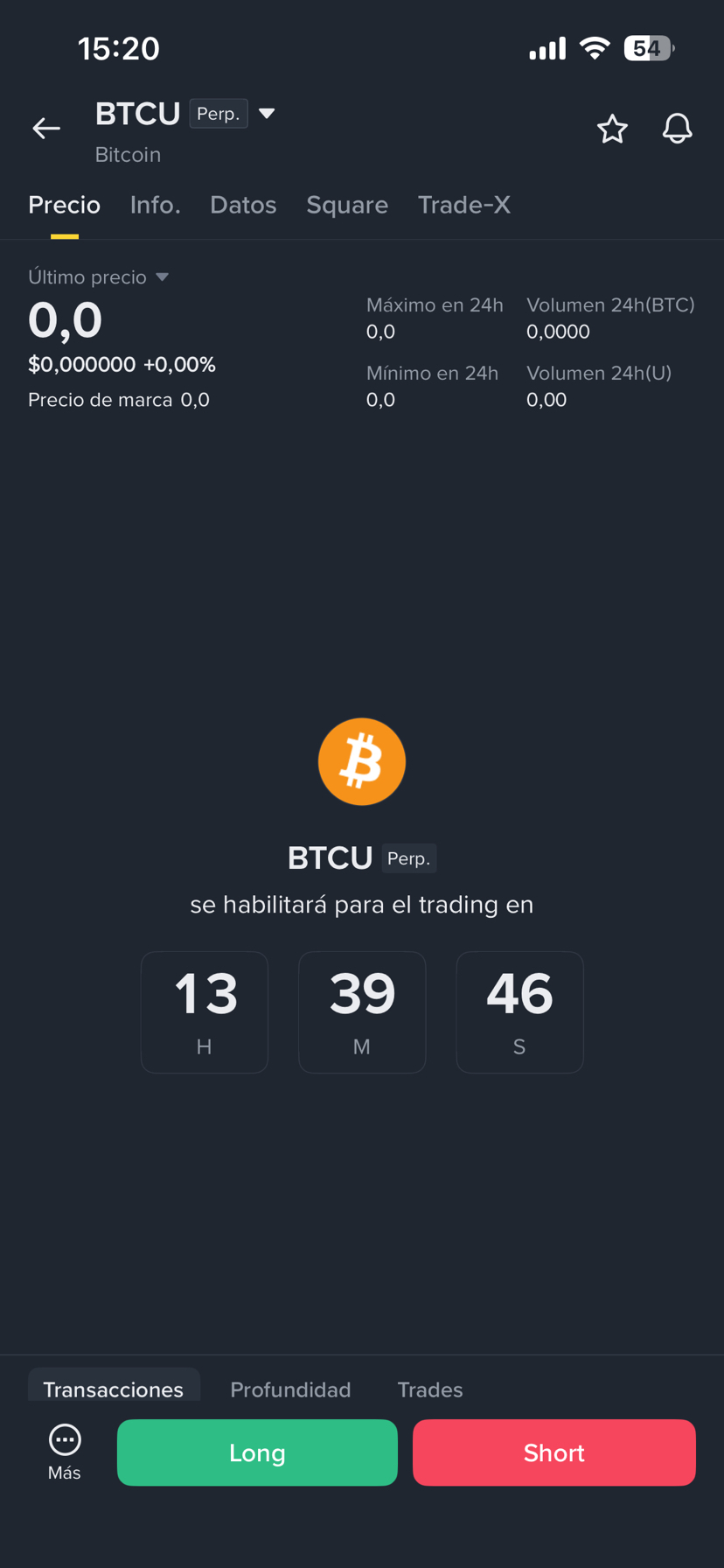

As the countdown shown in image.png reaches T-minus zero, the $BTCU Perpetual contract opens a high-leverage window for structural alpha. Due to initial market maker absence, expect a severe cross-asset liquidity discontinuity. Do NOT use naive market orders. 🧵👇

2/4 📊 The Math Behind the Basis Premium

Our high-frequency models are tracking the real-time spread deviation between the Mark Price (P_m) and Index Price (P_i). With BTCU's structural 2X daily leverage profile, historical tracking exhibits a fat-tailed distribution (kurtosis > 5.4). Localized mispricings will be highly volatile.

3/4 🛠️ Executing Strategy A: Cointegration Arbitrage

Our execution routers are live-calculating the rolling cointegration vector:

When z_t breaches the \pm2.5 standard deviation boundary, automated systems will long/short the legs to harvest pure structural delta.

4/4 🛡️ Risk Boundaries Calibrated

Initial Margin (IMR): 5.00% (20x Max Leverage limit)

Maintenance Margin (MMR): 2.50%

Realized Volatility: 74.2% Annualized

Action: Direct API routing utilizing strictly Post-Only limit flags to avoid immediate orderbook slippage. Let's print. 💻⚡