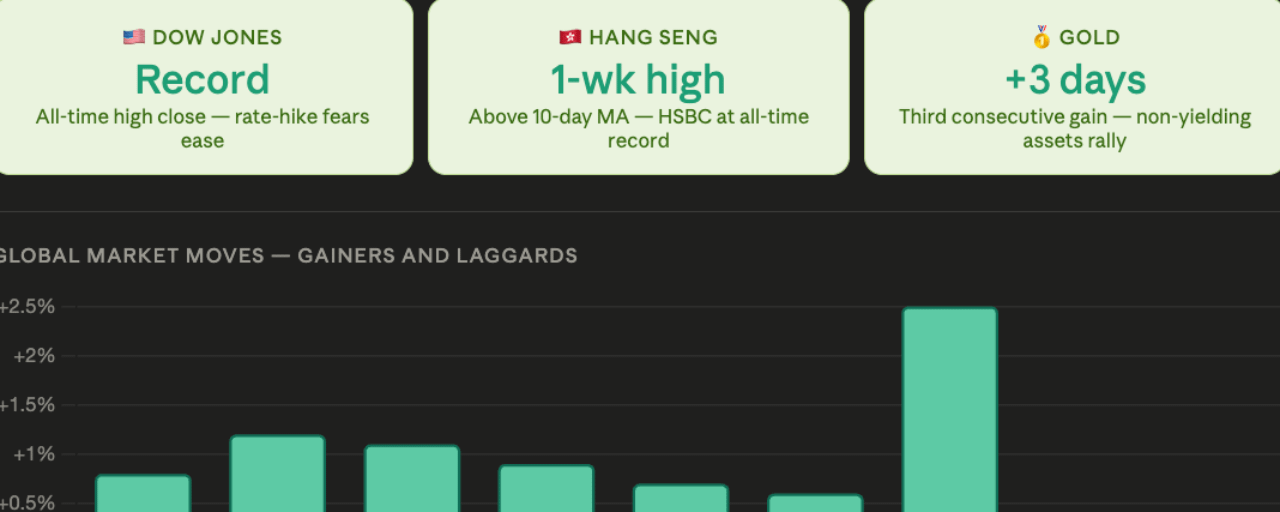

The Dow Jones Industrial Average closed at a record high overnight as June nonfarm payrolls came in far below the 110,000 consensus forecast at just 57,000 — easing concerns about further Federal Reserve rate hikes and triggering a broad risk-on response across global equity markets. US stock index futures extended gains into Friday morning. Japan, China A-shares, Hong Kong stocks, and South Korea's KOSPI all advanced. Gold extended its rally for a third consecutive session. Hong Kong's Hang Seng Index and Hang Seng China Enterprises Index hit one-week highs, with both breaking above their 10-day moving averages and HSBC climbing to an all-time record.

The US Session — Dow Record, Mixed Broader Picture

US stocks were mixed overnight despite the Dow's record close — a split that reflects the specific composition of the Dow Jones Industrial Average relative to the broader S&P 500 and Nasdaq. The Dow's 30 blue-chip components skew toward industrials, financials, and consumer staples that benefit more directly from rate-hike fears easing — sectors where lower-for-longer rates improve earnings multiples and reduce financing costs. The broader indices showed a more mixed response as tech and growth stocks digested the payrolls data alongside lingering uncertainty about whether a single soft jobs print changes the Fed's fundamental policy trajectory.

US markets will be closed on Friday for the July 4 holiday — meaning Thursday's record Dow close is the final US session data point before markets reopen next week with June CPI as the next major scheduled catalyst.

Hong Kong — Hang Seng and HSCEI at One-Week Highs, HSBC at Record

Hong Kong's equity markets responded constructively to the combination of the US jobs miss and the resulting rate-hike repricing. The Hang Seng Index and the Hang Seng China Enterprises Index both hit one-week highs, with the Hang Seng Index and Hang Seng Tech Index breaking above their respective 10-day moving averages — a short-term technical signal that suggests momentum has shifted from the bearish configuration that dominated June's Asian market selloffs.

HSBC's climb to an all-time record high is the standout individual move in the Hong Kong session. As one of the most rate-sensitive large-cap stocks in the Hang Seng — with earnings directly tied to the interest rate environment across the UK, Hong Kong, and Asian markets — HSBC's record high reflects precisely the mechanism through which the payrolls miss feeds into financial sector valuations: lower rate-hike probability reduces the ceiling on net interest margin expectations while simultaneously reducing the credit risk embedded in HSBC's loan book.

The Broader Asian Picture — Japan, A-Shares, KOSPI Advance

The positive reaction extended across major Asian markets. Japan and China A-shares both advanced alongside Hong Kong, while South Korea's KOSPI gained — a notable reversal from the three severe single-session crashes that characterized the KOSPI's June performance, including a 10% crash and two separate 6-9% declines that followed Samsung and SK Hynix's AI chip demand fears. Taiwan stocks and South Korea's KOSDAQ declined — the exceptions in an otherwise broadly positive Asian session, with Taiwan's index reflecting continued caution around semiconductor valuations even as the broader AI trade finds some stabilization.

Gold's Third Consecutive Gain

Gold extended its gains for a third straight session following the payrolls miss — continuing the same mechanism that lifted Bitcoin above $61,000 and silver back above $62. Lower rate-hike expectations reduce the opportunity cost of holding non-yielding assets like gold, while a weaker dollar removes the currency headwind that had pushed gold below $4,100 as recently as last week. Goldman Sachs had cut its year-end gold target to $4,900 and Deutsche Bank had reduced its Q3 target to $4,300 — both on the assumption of no 2026 Fed cuts. Three consecutive days of gold gains following the softest jobs print since the post-COVID recovery period suggests those targets may be revised upward if the labor market deceleration continues through subsequent months.

The Read-Through for Crypto

The Dow record, Hang Seng one-week high, and gold's third consecutive gain collectively describe a global risk-on response to the June payrolls miss that is broader and more sustained than a single-session US equity bounce. For crypto, the global equity and gold rally provides the "broader asset confirmation" that QCP Capital identified as the missing condition for Thursday's Bitcoin recovery above $60,000 to be classified as a genuine trend shift rather than a temporary rebound. Bitcoin at $61,600 heading into a long US holiday weekend, with Asian markets advancing and the Dow at a record, represents the most constructive macro backdrop the asset has faced since the June 17 FOMC meeting established the hawkish framework that drove $4.06 billion in June ETF outflows.