A cashier doesn't usually wait for money to physically arrive before handing over your groceries.

That sounds obvious, yet it's something I never really thought about until I started comparing traditional payment networks with blockchain infrastructure. When you tap a bank card, the payment isn't instantly settled between banks. First, an authorization decision happens. The network checks whether the payment meets a series of conditions, and only after approval does the settlement process continue.

For years, I've heard people describe blockchain as a replacement for traditional financial rails. After spending time reading Newton Protocol's documentation, I came away with a different conclusion.

Maybe blockchain already solved settlement.

Maybe what it never fully solved was authorization.

That's an important distinction because settlement and authorization answer completely different questions.

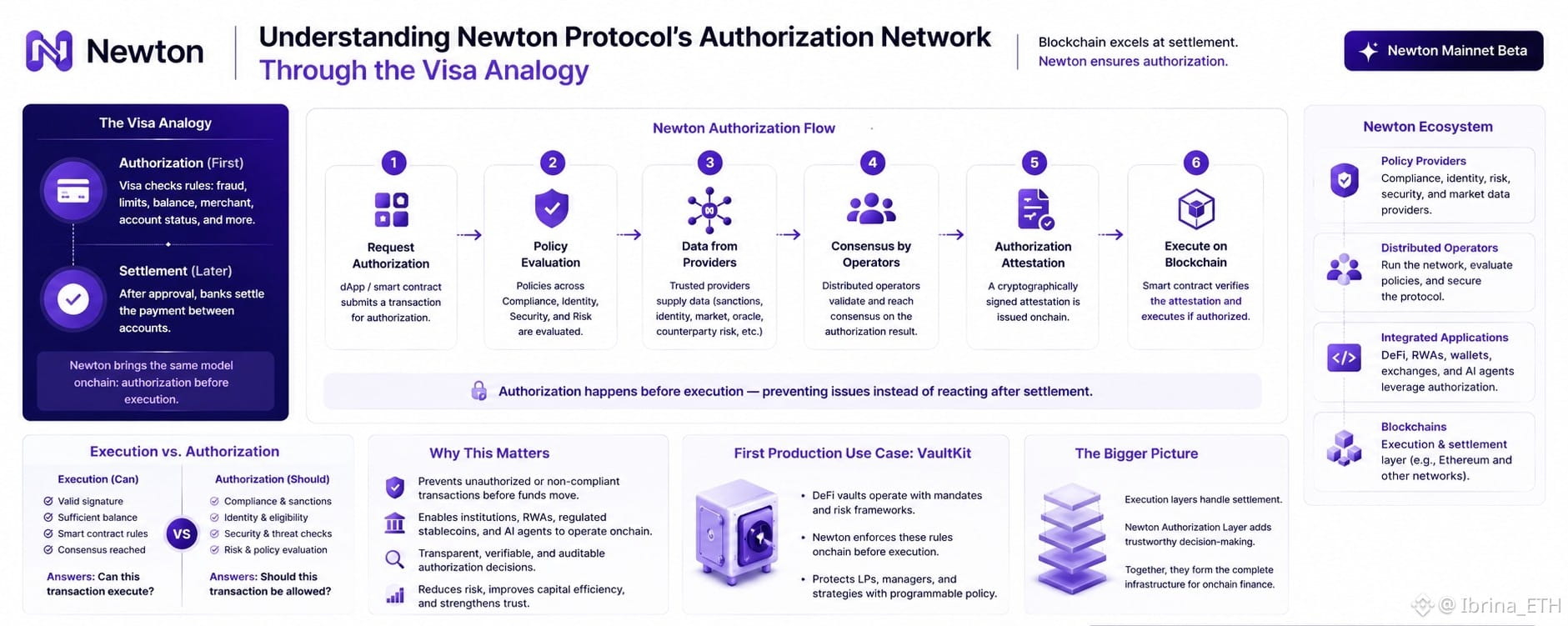

Settlement answers, "Can ownership be transferred?"

Authorization answers, "Should this transfer be allowed under the active rules?"

Traditional finance separates those responsibilities because they solve different problems. A payment network isn't simply checking whether money exists. It's evaluating fraud signals, spending limits, merchant restrictions, account status, and numerous risk controls before allowing value to move.

Public blockchains, on the other hand, intentionally avoid making those contextual decisions. If a transaction has a valid signature, enough balance, and satisfies consensus rules, execution proceeds.

That design has been one of blockchain's greatest strengths.

It's also one of its biggest limitations as institutional finance moves onchain.

Imagine two transactions that look identical at the protocol level.

Both have valid signatures.

Both have sufficient balances.

Both interact with the same smart contract.

The blockchain treats them equally.

An institutional asset manager probably wouldn't.

One wallet may belong to an approved client.

The other could violate sanctions requirements, exceed portfolio risk limits, fail eligibility checks, or interact with a compromised protocol.

From the blockchain's perspective, they're identical.

From a financial institution's perspective, they're completely different decisions.

This is exactly where Newton Protocol positions itself.

The Visa comparison isn't about becoming another payment processor or replacing blockchains.

It's about introducing a decentralized authorization layer before settlement, much like authorization networks have existed in traditional finance for decades.

The difference is that Newton performs those authorization decisions through programmable policies that are transparent, verifiable, and designed for decentralized applications.

When an integrated application requests authorization, Newton evaluates policies across compliance, identity, security, and risk. Depending on the policy, external providers can contribute information such as sanctions screening, identity verification, oracle health, market conditions, or counterparty risk. Distributed operators then reach consensus and generate a cryptographically signed authorization attestation that applications can verify before executing the transaction.

One architectural decision stood out during my research.

Newton doesn't attempt to move execution away from existing blockchains.

Ethereum and other execution layers continue doing what they already do extremely well.

Newton focuses on a completely different responsibility.

That separation matters because it allows each layer to specialize instead of forcing one protocol to solve every problem.

It's similar to how the internet evolved. Communication protocols, cloud infrastructure, identity systems, and content delivery networks all developed independently because each solved a distinct challenge. Financial infrastructure may be following the same path, where authorization becomes its own specialized layer rather than another feature added onto smart contracts.

The first production implementation through VaultKit also reflects this philosophy. DeFi vaults already operate with investment mandates, compliance requirements, and risk management policies that frequently exist outside blockchain infrastructure. Newton doesn't invent those rules; it gives applications a decentralized mechanism to enforce them before assets move.

Of course, there are trade-offs.

Adding authorization introduces another layer that developers must integrate. Some builders will argue that permissionless systems should avoid additional decision points altogether. That's a valid perspective, especially for applications that intentionally prioritize minimal restrictions.

But the opposite argument is equally compelling.

Institutional capital, tokenized real-world assets, regulated stablecoins, and autonomous AI agents all operate within environments where authorization already exists. Today, much of that logic happens offchain through manual reviews, compliance teams, or proprietary systems that users cannot verify.

Newton's approach isn't about creating new rules.

It's about making existing rules programmable, decentralized, and cryptographically verifiable before settlement occurs.

The more I studied the protocol, the less I viewed the Visa analogy as a marketing comparison.

Instead, it became an architectural explanation.

Blockchains transformed how value settles.

Newton is exploring how decentralized systems can also determine whether value should move in the first place.

If settlement became the defining innovation of the first generation of blockchain infrastructure, perhaps authorization will become one of the defining innovations of the next.

That's the question I keep coming back to—not whether blockchain can execute transactions faster, but whether future financial systems will need decentralized networks capable of making trustworthy decisions before execution ever begins.