According to CoinMarketCap data, the global cryptocurrency market cap now stands at $2.15T, up by 0.86% over the last 24 hours.

Bitcoin (BTC) has been trading between $60,605 and $62,200 over the past 24 hours. As of 09:30 AM (UTC) today, BTC is trading at $62,685, up by 0.33%.

Most major cryptocurrencies by market cap are trading mixed. Market outperformers include TLM, ARPA, and ZKP, up by 61%, 39%, and 34%, respectively.

Jobs Shock Sends Rate-Hike Odds Tumbling — Dow Hits a Record, Hang Seng Reaches a One-Week High, and Bitcoin ETFs Post Their Best Inflow Day Since May

June payrolls came in at just 57,000 — roughly half the forecast — and markets responded across the board: the Dow closed at a record high, Hong Kong's Hang Seng hit a one-week high with HSBC reaching an all-time high, gold extended gains for a third straight session, and Bitcoin ETFs snapped a 10-day outflow streak with $221.7M in net inflows — the first day above $200M since early May.

The soft jobs data cut Fed rate-hike odds from 65% to 50% in minutes, giving risk assets the macro relief they've been waiting for. Bitcoin climbed to $61,600 (+6.5% from Tuesday's near two-year low), SOL surged 17%, and altcoin selling pressure hit a near five-year low. Citi sees Brent at $60 by year-end — and if they're right, the inflation narrative that crushed crypto in H1 may be unwinding faster than consensus expects.

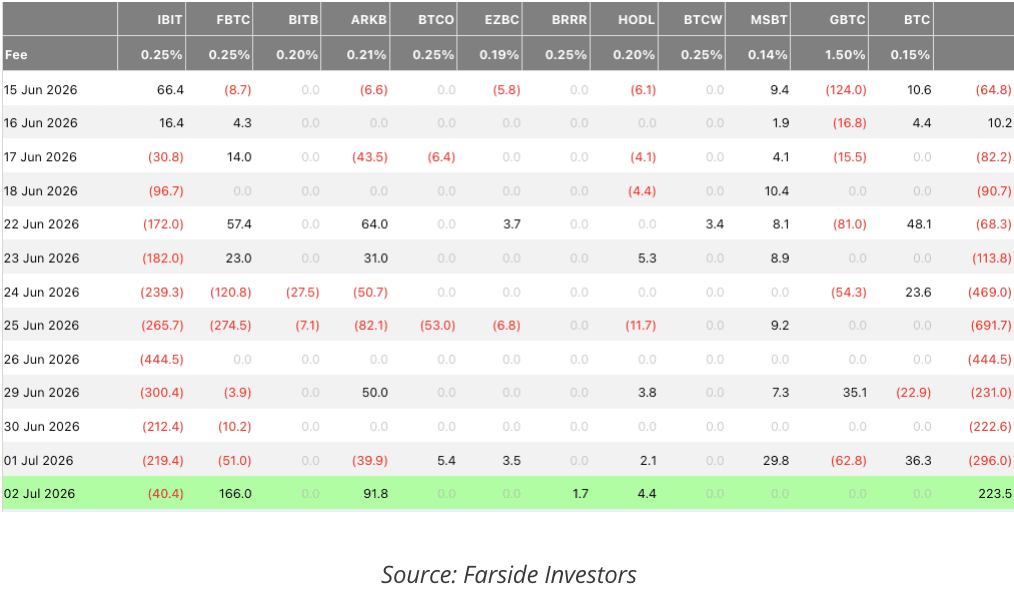

Bitcoin ETFs Record $221.7 Million in Daily Inflows — First Day Above $200 Million

Key Takeaways:

US spot Bitcoin ETFs recorded $221.7M in net inflows Thursday — the strongest single-day intake since early May and the first above $200M in over six weeks, snapping a 10-day outflow streak that had totaled $2.7B+

Fidelity's FBTC led with $166M (75% of the day's total, its largest single-fund daily inflow in weeks); ARK 21Shares followed with $91.8M; VanEck's HODL added $4.4M; Valkyrie's BRRR added $1.7M

The critical divergence: BlackRock's IBIT posted $40.4M in net outflows — its 11th consecutive session of redemptions since June 17, with cumulative outflows now exceeding $2.2B; Fidelity and ARK buyers skew crypto-native; IBIT's base is more heavily weighted toward traditional financial institutions and RIA platforms — institutional re-engagement is not yet broad-based

Ether ETFs attracted $29.1M (second consecutive positive session); XRP ETFs returned to $6.6M net inflows — simultaneous recovery across BTC, ETH, and XRP ETFs signals a broader sentiment shift rather than rotation between assets

Context: Bitwise CIO Matt Hougan publicly suggested the market may be nearing a bottom; the Fear and Greed Index is at "extreme fear" — historically a reliable accumulation signal

Summary:

A $221.7M inflow day is the most constructive ETF data point of the entire June correction — but IBIT's 11th consecutive outflow session is the caveat that keeps it from being a definitive inflection point. The institutional re-engagement visible in Fidelity and ARK flows needs to eventually include IBIT to constitute a genuine reversal of the institutional exit that defined June. A single strong day is a necessary condition for confirmed recovery; it is not yet sufficient on its own, particularly while IBIT's RIA and financial advisor base remains in withdrawal mode.

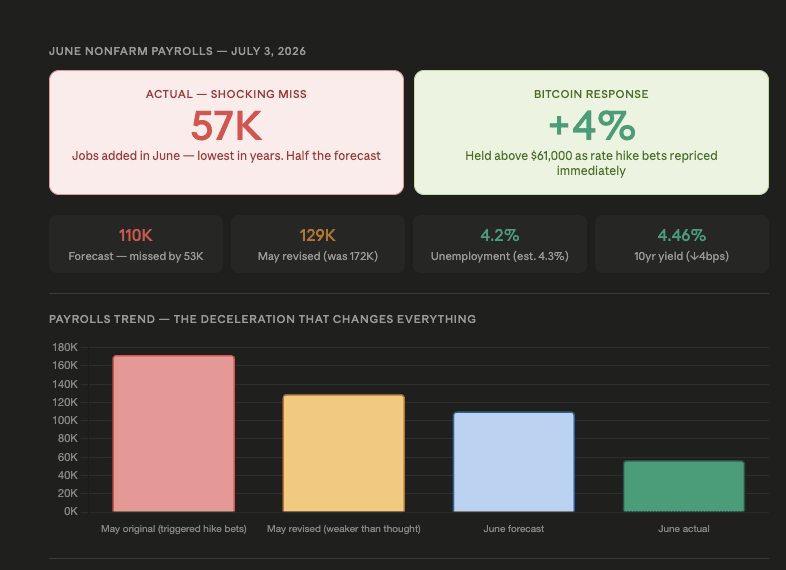

June Payrolls Shock at 57,000 — Half the 110,000 Forecast — Rate Hike Odds Drop From 65% to 50%

Key Takeaways:

June NFP came in at 57,000 — roughly half the 110,000 consensus and the softest monthly addition in years; May was revised down from 172,000 to 129,000, meaning the month that justified the hawkish June dot plot was materially weaker than reported

The unemployment rate fell to 4.2% vs 4.3% expected — but driven by the labor force participation rate declining from 61.8% to 61.5%, meaning fewer people looked for work rather than more finding it; the weakest possible version of an unemployment rate beat

CME FedWatch: rate-hike probability for September dropped from ~65% to ~50% in minutes; the 10-year Treasury yield dipped 4bps to 4.46%; Nasdaq 100 futures moved from flat to +0.7% immediately following the release

This is the first genuine data-driven pressure on the $34.5B net long dollar positions (seven-year high) and $700B in notional SOFR shorts (record 2.97M contracts) — both built on the assumption of a strong labor market justifying the Fed's hawkish trajectory; 57,000 is not the number that sustains that assumption

Summary:

57,000 jobs is the macro permission slip Bitcoin's accumulation signals have been waiting for since June 5. A miss of this magnitude — half the forecast, plus a prior-month revision that retroactively weakens the hawkish dot plot's data justification — is the first genuine case for the crowded dollar-long and rate-hike-bet trade to begin unwinding. One jobs report does not reverse months of macro repricing, but it changes the direction of travel: the question is no longer "when does the Fed hike?" but "how long can it hold?" — and that framing is meaningfully more constructive for Bitcoin.

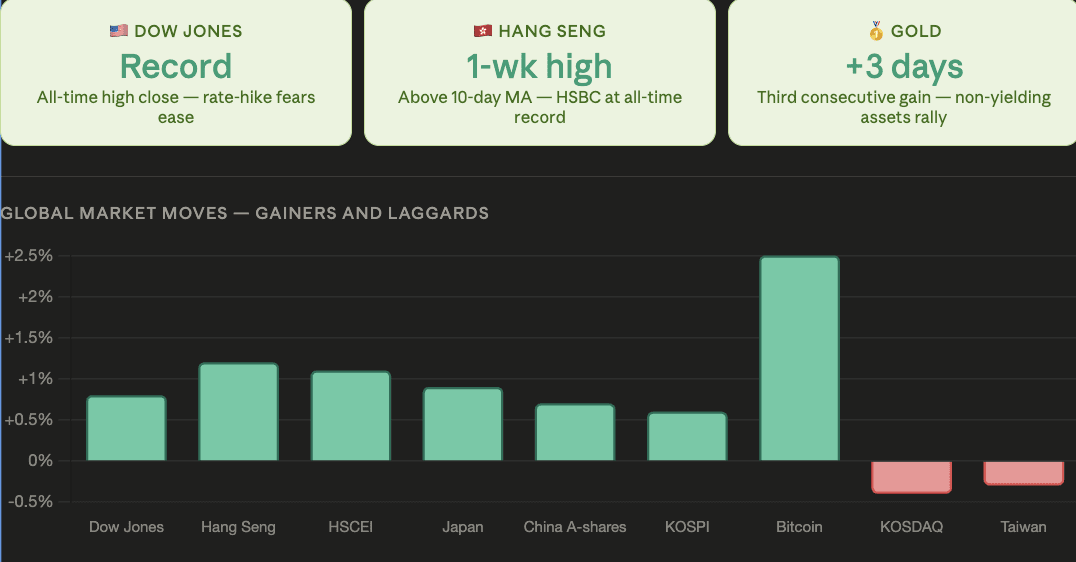

Dow Hits Record High, Hang Seng Reaches One-Week High as June Payrolls Miss Eases Rate-Hike Fears

Key Takeaways:

The Dow Jones Industrial Average closed at a record high overnight; US stock index futures rose further this morning; Japan, China A-shares, Hong Kong, and South Korea's KOSPI all advanced; Taiwan stocks and South Korea's KOSDAQ fell

Hong Kong's Hang Seng Index and Hang Seng China Enterprises Index hit one-week highs; both the Hang Seng Index and Hang Seng Tech Index broke back above their 10-day moving averages; HSBC (0005) climbed to an all-time high

Gold extended gains and is on track for a third straight daily rise — the soft jobs data reducing the opportunity cost of holding non-yielding assets simultaneously benefiting both gold and Bitcoin

US markets are closed today for the July 4 holiday — reduced liquidity across futures markets; any Iran or macro developments over the long weekend will be the primary price driver in early Asian trading Monday

Summary:

The global equity rally on the back of the US jobs miss is the clearest signal that markets read 57,000 as a rate-hike de-escalation event rather than an economic growth scare. When a weak jobs number lifts the Dow to a record rather than triggering risk-off selling, it confirms the dominant market concern was the Fed hiking too aggressively — not that the economy is collapsing. For Bitcoin, a risk-on global equity environment heading into a US holiday weekend is the most favorable backdrop for the ETF inflow recovery to continue in Monday's session.

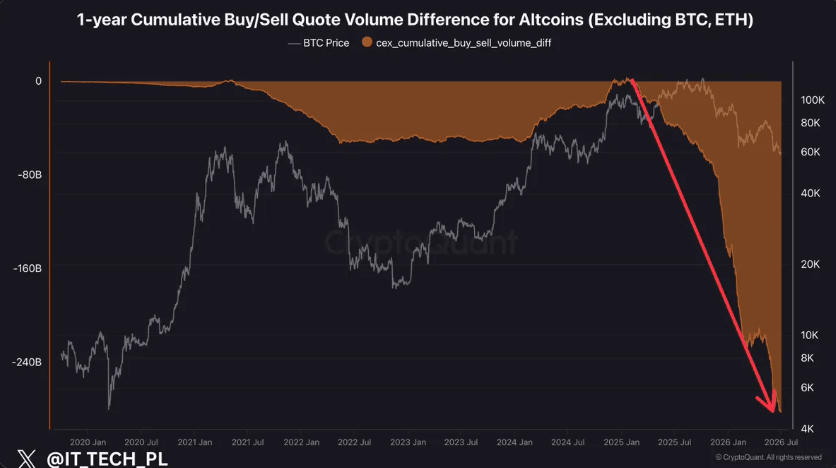

Key Takeaways:

The cumulative buy-sell volume difference for altcoins (ex-BTC and ETH) has fallen to a near five-year low per CryptoQuant — rivaling or exceeding every comparable period since approximately 2021, including the 2022 bear market that saw BTC fall to $15,500 and ETH to $880

15 consecutive months of uninterrupted net selling since early 2025 — almost no sustained selling exhaustion or buyer return windows during that stretch; consistent with the prolonged structural bear phases of 2018-19 and 2022, not the briefer corrections of 2021 and early 2024

No bottom signal has formed: CryptoQuant selling pressure indicator silent for 1,256 days; UTXO ratio in historical bottoming range but 365-day MA requires further deterioration; on-chain demand metrics (active addresses, transfer values, fees) show no demand surge consistent with genuine bottom formation

What changes the picture: the same macro catalysts every other framework has identified — sustained Fed communication shift on softer inflation data, dollar and yield unwind from historically crowded positioning, stablecoin liquidity returning to exchanges in volume sufficient to provide buy-side depth

Summary:

Fifteen months of uninterrupted altcoin net selling at near five-year extreme levels is the structural backdrop against which this week's SOL and UNI outperformance should be read. Those are specific-catalyst moves in specific tokens, not evidence that the cumulative buy-sell imbalance is reversing. Until the aggregate net selling trend stabilizes and buyers return in sustained volume — the precondition for genuine bottom formation — altcoin price recovery remains dependent on individual catalysts rather than the broad structural demand turn that a five-year low in buy-sell differential would require to reverse.

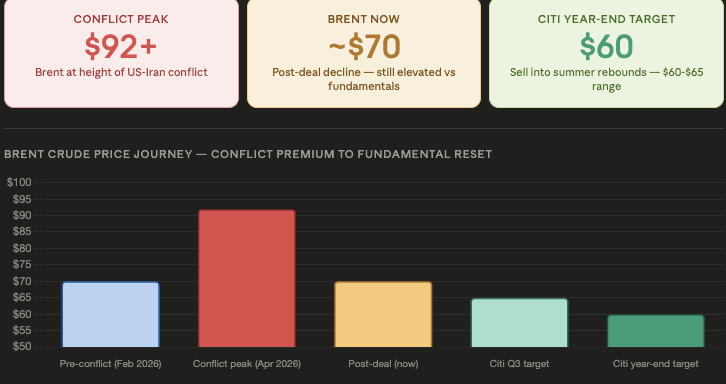

Key Takeaways:

Citi projects Brent crude falls to ~$60 by year-end — recommending selling into summer rebounds within a $60-$65 target range; the bank explicitly separates the geopolitical premium that drove Brent from $70 to $92+ during the conflict from the underlying supply-demand balance that will govern pricing as that premium dissipates

Four drivers: Hormuz shipping flows returning to normal; major crude buyers still absent from market; physical crude markets weakening significantly; inventory declines running far below the expectations that justified peak pricing above $90

The macro chain for crypto: Brent at $60 → energy-driven CPI decelerating → Reuters poll "no cuts through 2027" consensus forced to revise → $700B in SOFR shorts and $34.5B in dollar longs begin unwinding → Bitcoin's primary macro headwind of 2026 structurally reversed

Thursday's NFP at 57,000 already pushed rate-hike odds from 65% to 50%; if Citi's oil trajectory materializes through H2, the June CPI print and subsequent data could shift the Fed communication that Warsh's Sintra comments had begun to soften — a sequential disinflationary setup Bitcoin has not had since early 2026

Summary:

Citi's $60 year-end Brent forecast is the most consequential macro call of the week for Bitcoin — more so than the NFP miss, which is a single data point. If oil grinds toward $60 through H2 as the Hormuz premium fully fades, it provides the sustained headline inflation deceleration that would force the most hawkish rate-path consensus in years to revise. That revision — not any single jobs or CPI print — is the mechanism that converts Bitcoin's structural accumulation floor into an institutional re-engagement cycle. The Standard Chartered-Kendrick thesis that the Iran deal's oil impact is Bitcoin's recovery catalyst has now received its most concrete institutional validation from one of the largest banks in the world.

Market movers:

NVDAB: $196.08 (-0.08%)

MSFTB: $389.77 (+0.92%)

SPCXB: $160.5 (+2.46%)

METAB: $589.63 (-3.72%)

TSLAB: $399.35 (-6.51%)

MUB: $1020.09 (+0.36%)

AMDB: $531.29 (-0.74%)

INTCB: $122.79 (-2.82%)

LITEB: $751.42 (-4.65%)

QQQB: $723.04 (-0.34%)