A Deep Structural Analysis of Bitcoin-Centric Markets

Crypto in 2026 looks mature on the surface.

There are thousands of tokens trading across dozens of categories. We have decentralized exchanges processing billions in volume. Lending protocols generating real fees. Layer-1 and Layer-2 networks hosting millions of users. Institutional products like ETFs, custodians, and regulated onramps now exist in the open.

From the outside, crypto appears diversified.

But markets don’t care about appearances.

Markets care about how assets behave under stress.

And when you look honestly at price behavior, correlations, and capital flows, a difficult truth emerges:

Crypto still behaves like a single macro asset dominated by Bitcoin.

This is not a failure of innovation.

It’s a consequence of how liquidity, risk, and human behavior work.

To understand why diversification still doesn’t exist, we need to break the problem down layer by layer.

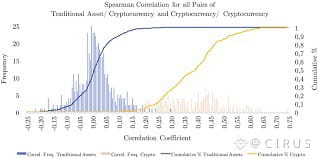

What Diversification Actually Means (And Why Crypto Fails It)

Diversification is not about owning many assets.

It is about owning assets that respond differently to the same shock.

In traditional finance:

Bonds can rise when equities fall

Commodities can hedge inflation

Cash can reduce volatility

Certain equities can outperform during downturns

Diversification is behavioral independence.

Now ask a simple question:

When Bitcoin falls 10%, what happens to the rest of crypto?

The answer is uncomfortable:

Ethereum falls

Solana falls

DeFi tokens fall

Infrastructure tokens fall

Gaming tokens fall

AI tokens fall

Often harder.

That is not diversification.

That is leverage through complexity.

Crypto portfolios often look diversified, but they move as one unit.

The Origin of Bitcoin-Centric Behavior

To understand why this hasn’t changed, we need to go back to crypto’s foundations.

Bitcoin was the first liquid crypto asset.

It became:

The unit of account

The liquidity anchor

The psychological reference

Everything else grew on top of it, not alongside it.

Even today:

BTC pairs dominate liquidity

BTC charts dictate sentiment

BTC dominance defines risk appetite

Altcoins are not independent markets.

They are derivatives of Bitcoin liquidity.

This structural dependency has never been broken.

“But We Have Real Fundamentals Now” — Why That Argument Fails

One of the most common counterarguments is:

“This time is different. Protocols have revenue. Users exist.”

That statement is true — and still incomplete.

Yes, many protocols generate real revenue.

Yes, some have more users than mid-sized fintech apps.

But markets do not price absolute fundamentals.

They price relative certainty under stress.

When fear enters the system:

Cash is preferred over risk

Liquidity is preferred over yield

Simplicity is preferred over complexity

Bitcoin wins all three.

Even a revenue-generating token:

Has governance risk

Has protocol risk

Has smart contract risk

Has narrative risk

Has regulatory uncertainty

Bitcoin, by comparison, is simple:

Fixed supply

Clear narrative

Deep liquidity

Institutional acceptance

So when capital gets nervous, it doesn’t ask:

“Which protocol earns fees?”

It asks:

“Where can I park without thinking?”

That answer is Bitcoin or stablecoins.

Sector Labels Don’t Matter to Capital

Crypto loves categories:

DeFi

Infrastructure

Computing

AI

RWAs

Gaming

But capital doesn’t trade labels.

It trades liquidity and correlation.

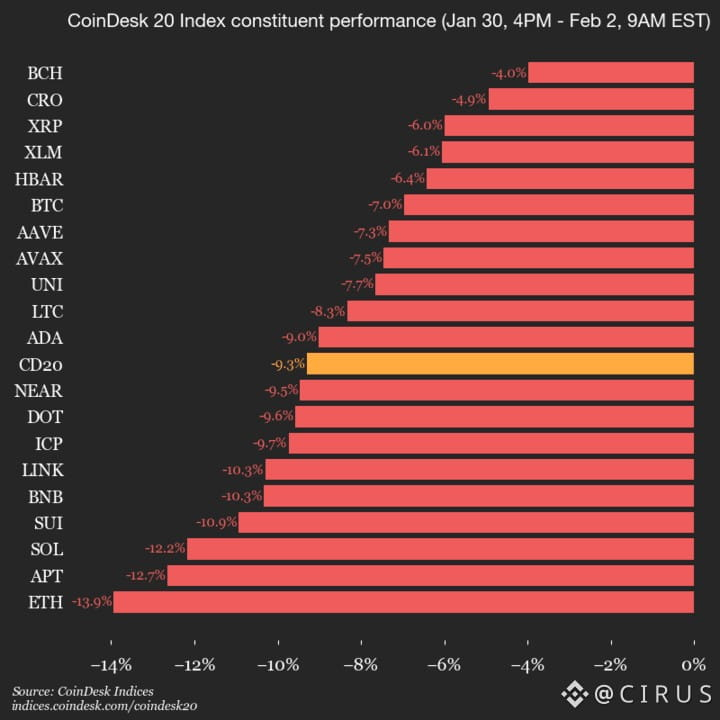

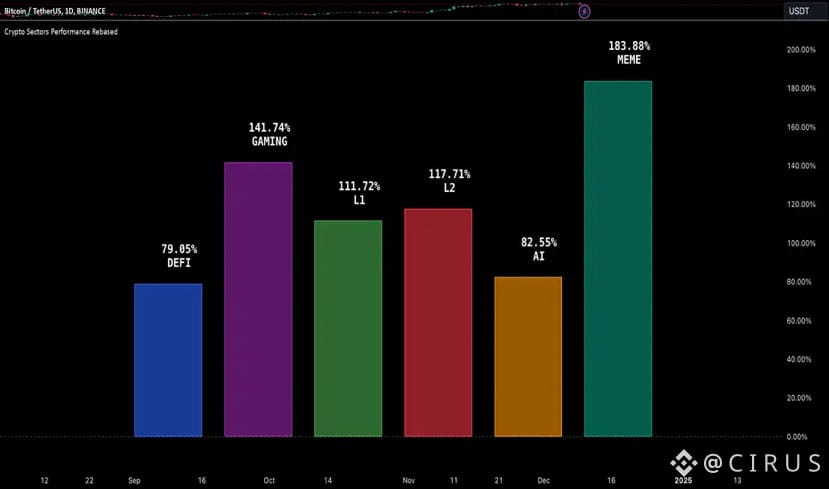

This is why CoinDesk’s sector indices are so revealing.

Sixteen different indices.

Different token sets.

Different narratives.

Yet almost all are down 15–25% together.

That tells us something fundamental:

Sectors exist in marketing.

Correlation exists in reality.

Until assets respond differently to stress, sectors are cosmetic.

Macro Pressure Exposes the Truth

The strongest evidence against crypto diversification appears during macro stress.

Look at recent events:

Asian equity sell-offs

Sharp drops in gold and silver

Rising real yields

Dollar volatility

How did crypto respond?

It didn’t hedge.

It didn’t diverge.

It followed risk lower.

Bitcoin declined alongside equities.

Altcoins declined more.

This behavior aligns Bitcoin closer to:

High-beta equities

Growth assets

Liquidity-sensitive instruments

Not to defensive hedges.

Calling Bitcoin “digital gold” is aspirational — not descriptive.

Why Revenue Tokens Still Sell Off

Let’s address the most frustrating part for long-term believers.

Protocols like:

Aave

Jupiter

Aerodrome

Tron

Base

Generate real economic value.

Yet their tokens:

Sell off during BTC drawdowns

Correlate with macro risk

Fail to protect capital

Why?

Because token ownership is not the same as equity ownership.

Token holders:

Do not have guaranteed cash flows

Do not control capital allocation

Do not have liquidation preference

Do not receive dividends by default

So when markets de-risk, these tokens are treated as:

speculative instruments, not businesses.

Until token design changes meaningfully, this behavior persists.

The Hyperliquid Exception — And Why It’s Rare

Hyperliquid stands out because it breaks some of these rules.

Its outperformance happened due to:

Extreme concentration of usage

Clear value capture

Direct alignment between activity and token demand

But this is not the norm.

Most protocols:

Distribute value slowly

Dilute incentives

Depend on long-term belief

Markets under stress don’t reward belief.

They reward immediacy.

Hyperliquid is an exception because it provided immediacy.

That’s why it survived — not because fundamentals suddenly mattered broadly.

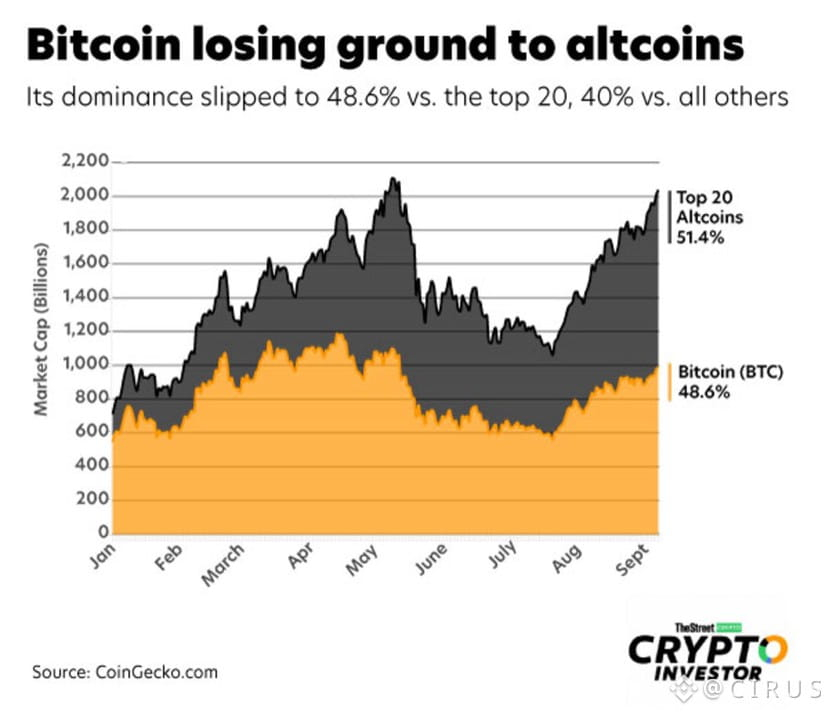

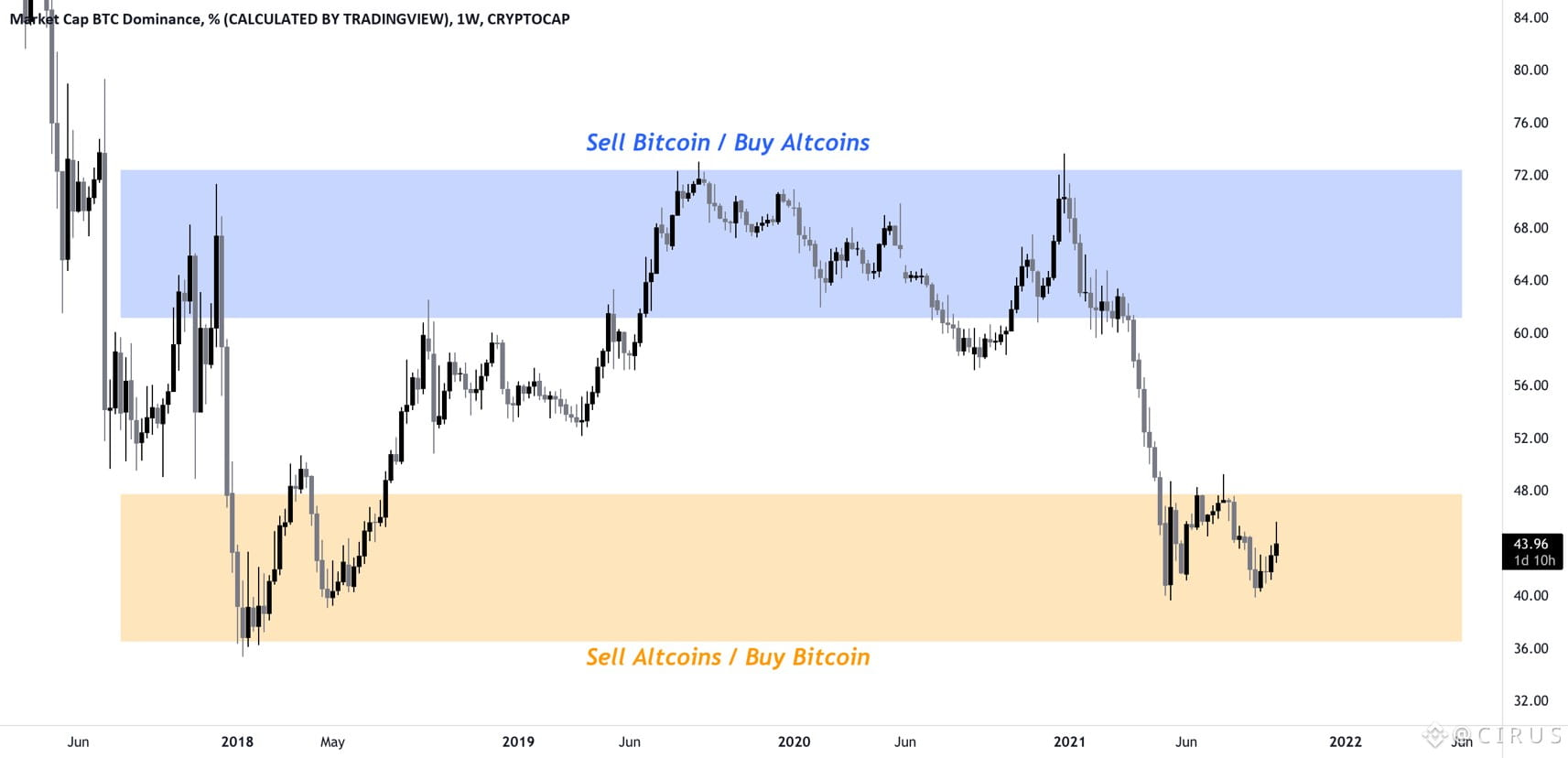

Institutions Didn’t Fix Correlation — They Reinforced It

Many expected institutions to diversify crypto.

Instead, they:

Bought Bitcoin

Ignored most alts

Used stablecoins for defense

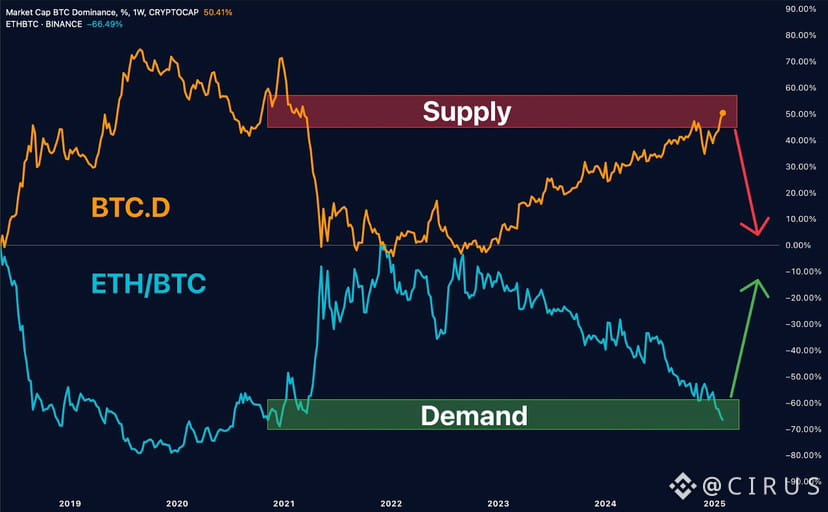

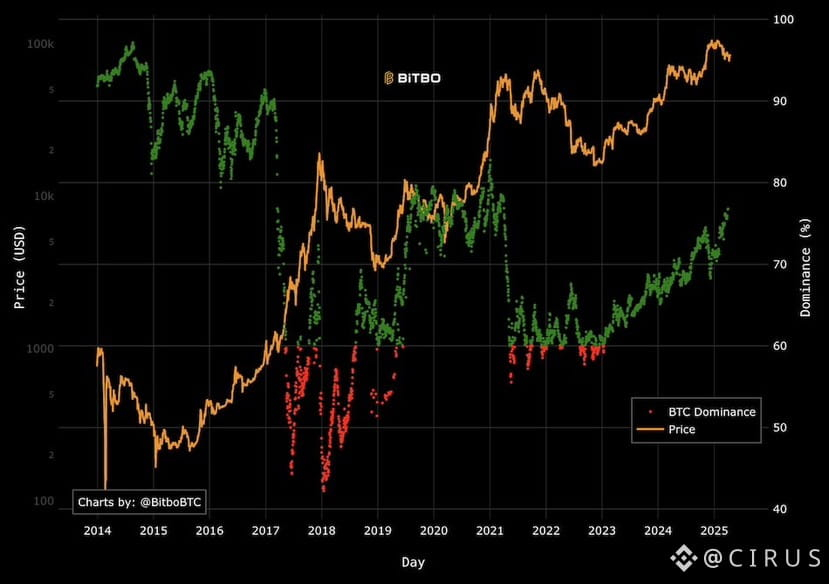

Spot BTC ETFs concentrated capital into the most dominant asset.

Bitcoin dominance staying above 50% is not accidental.

It reflects institutional preference for simplicity.

When volatility spikes:

Institutions don’t rotate into DeFi

They rotate into BTC or cash

This behavior sets the tone for the entire market.

Retail follows liquidity, not conviction.

Stablecoins: The Real Defensive Asset

One of the most important shifts in crypto is rarely discussed:

Stablecoins replaced altcoins as the hedge.

When risk rises:

Capital exits alts

Capital enters stablecoins

Sometimes flows back into BTC

This creates a loop:

BTC ↔ Stablecoins ↔ Alts

But alts are always the shock absorber.

This is not diversification.

It’s hierarchical risk.

The Hard Truth So Far

By this point, the picture is clear:

Crypto in 2026 is not a collection of independent assets.

It is:

One macro trade (Bitcoin)

One liquidity buffer (stablecoins)

Many speculative satellites (alts)

Owning many alts does not reduce Bitcoin risk.

It magnifies it.

#BinanceBitcoinSAFUFund #PreciousMetalsTurbulence #MarketCorrection #squarecreator #GoldSilverRebound

#BinanceBitcoinSAFUFund #PreciousMetalsTurbulence #MarketCorrection #squarecreator #GoldSilverRebound