Why This Filing Matters, How the Product Works, and What It Says About the Next Phase of Institutional Bitcoin

For a long time, every major Wall Street move into Bitcoin was treated as a symbolic event, almost as if the name on the door mattered more than the structure of the product itself, but that phase is fading now, because the more revealing question is no longer who is entering the market, but how they are choosing to package their exposure once they arrive. Goldman Sachs has now filed with the U.S. Securities and Exchange Commission for the Goldman Sachs Bitcoin Premium Income ETF, a proposed fund designed to give investors bitcoin-linked exposure while also generating income through options premiums, and that alone tells you this is not a plain-vanilla spot Bitcoin product. Reuters reported the filing on April 14, 2026, describing it as Goldman’s first bitcoin ETF product, while the preliminary prospectus confirms the fund’s name, objective, and structure.

This Is Not a Simple Bitcoin ETF, and That Difference Is the Entire Story

The first thing to understand is that this filing is not built around the cleanest version of Bitcoin ownership. The prospectus states that the fund seeks current income while maintaining prospects for capital appreciation, which already places it in a different category from the straightforward spot products that simply aim to track bitcoin as directly as possible. Under normal circumstances, the fund intends to invest at least 80% of its net assets in investments that provide exposure to bitcoin, but that exposure can come through spot Bitcoin exchange-traded products, options on those products, and options on indices tied to those products, rather than through direct ownership of bitcoin itself. The filing explicitly says that neither the fund nor its Cayman subsidiary will invest directly in bitcoin.

That distinction may sound technical, but it changes the meaning of the product completely. A direct spot wrapper says, in effect, “Here is bitcoin in a regulated investment format.” An income-oriented options wrapper says something much more specific: “Here is bitcoin transformed into a product for investors who want a cash-generating strategy and are willing to exchange part of the upside for that feature.” Goldman is not just offering access here. Goldman is translating bitcoin volatility into something that fits a very familiar asset-management language.

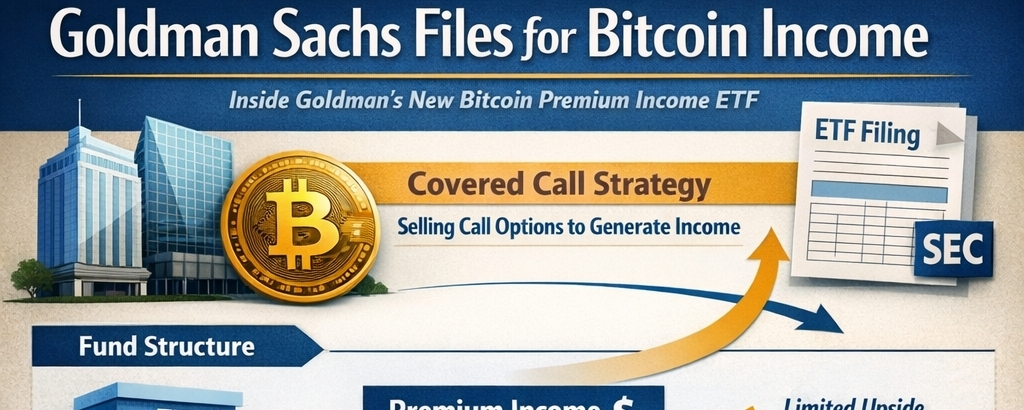

The Core Strategy Is an Options Overwrite, Which Means Income Comes First and Full Upside Comes Second

According to the prospectus, the fund gains bitcoin exposure by owning shares in one or more spot Bitcoin ETPs and by purchasing and selling Bitcoin ETP options, while primarily generating income through what it calls a dynamic options “overwrite” strategy. In simple terms, the fund plans to sell call options on bitcoin-linked instruments and collect premiums from buyers of those options. The document says Goldman expects the overwrite level, meaning the ratio of the notional value of call options sold, to range between 40% and 100% of the value of the bitcoin exposure in the portfolio.

That range matters because it shows how aggressive the strategy can become. If the overwrite is closer to 100%, the fund is monetizing a very large share of its exposure through call selling, which may increase distributable income but also increases the chance that a strong upside move in bitcoin will not fully pass through to shareholders. The prospectus is direct about that tradeoff. It says the strategy may outperform an equivalent unhedged portfolio when bitcoin is flat, declining, or only modestly rising and the income from premiums is large enough to offset that environment, but it may underperform when bitcoin rises sharply and the appreciation above the options’ strike prices exceeds the premium collected. That is a sophisticated way of saying the product is built to smooth and monetize volatility, not to preserve the full character of raw bitcoin upside.

Why Goldman Is Taking This Route Instead of a Pure Spot Structure

This is where the filing becomes more interesting than the headline. Wall Street institutions do not usually stop at simple access products once a market becomes large enough, liquid enough, and operationally safe enough to structure. They move from access to segmentation. First comes the basic wrapper, then come the variations tailored to different investor psychologies, client needs, and portfolio frameworks. That pattern is visible all over the ETF market, and Reuters connected Goldman’s filing to its recent acquisition of Innovator Capital Management, the options-focused ETF provider known for defined outcome strategies. Goldman completed that acquisition on April 2, 2026, and Reuters said the deal added about $31 billion in assets and 171 ETFs, lifting Goldman’s ETF assets under supervision to roughly $90 billion. Goldman’s own press release described Innovator as a leader in defined outcome ETFs and framed the transaction as a major expansion of Goldman Sachs Asset Management’s ETF business.

Once you place the bitcoin income filing next to that acquisition, the logic becomes much clearer. Goldman did not merely step into crypto at random. It first deepened its internal capability in options-based ETF construction, then almost immediately filed a bitcoin-linked income product using exactly the kind of toolkit Innovator is known for. In that sense, the filing is not just a crypto event. It is a product-manufacturing event. Goldman is applying a familiar active-ETF design language to bitcoin exposure, which suggests the bank sees crypto less as a one-off thematic allocation and more as a raw ingredient that can now be reshaped for different portfolio objectives.

The Cayman Subsidiary Is a Quiet but Important Part of the Structure

The prospectus also states that the fund may hold positions directly and/or through a wholly owned Cayman Islands subsidiary called the Goldman Sachs Bitcoin Premium Income Portfolio CFC. That is not an incidental detail. It reflects the way some U.S. funds handle certain derivatives and commodity-linked exposures within existing tax and regulatory constraints. The fund may use the subsidiary to hold exposure that would be less efficient or less practical inside the main registered fund itself, while also holding fixed-income instruments and other collateral-supporting assets.

For ordinary investors, the takeaway is not that something is hidden, but that the product is structurally more layered than a simple spot ETF. A more layered structure usually means more moving parts, more tax nuance, and more operational dependencies. The filing itself acknowledges Subsidiary Investment Risk, noting that investors are indirectly exposed to the risks of the subsidiary’s investments and that there is no assurance the subsidiary’s objectives will be achieved. That does not make the structure defective, but it does mean this product belongs to the engineered side of the ETF world rather than the simplest side.

The Word “Income” Makes the Product Sound Calmer Than It Really Is

One of the easiest mistakes investors can make with products like this is to let the word “income” do too much emotional work. Income sounds stable, measured, and defensive, but the filing goes out of its way to remind investors that this remains a volatile and risky strategy. The prospectus says the investment is not a bank deposit, is not insured by the FDIC, and may lose money. It lists a broad series of principal risks, including Bitcoin Risk, Bitcoin ETP Options Risk, Bitcoin ETP Options Writing Risk, Spot Bitcoin ETP Risk, Derivatives Risk, Covered Call Strategy Risk, Volatility Risk, Tax Risk, and Subsidiary Investment Risk, among others.

The product remains deeply tied to bitcoin’s underlying behavior. The filing describes bitcoin as a relatively new innovation whose market is subject to rapid price swings, speculation, and uncertainty, and it notes that spot Bitcoin ETPs themselves have only a short operating history. It also warns that if arbitrage and creation-redemption processes in those underlying ETPs are disrupted, their market prices may trade at wider premiums or discounts to net asset value, which can then affect the Goldman fund that holds them. In other words, this ETF does not eliminate bitcoin’s fragility. It layers option income on top of exposure that is still vulnerable to the same market, liquidity, and structural dislocations that define crypto-related instruments.

The Fund May Pay Monthly, but Monthly Does Not Mean Predictable

The prospectus says distributions from net investment income and options premium are normally declared and paid monthly, while net long-term capital gains, if any, are normally paid annually. That monthly schedule will likely be central to how the product is marketed, because it gives advisors and retail investors a familiar frame through which to understand a highly unfamiliar underlying asset. Yet the same filing immediately qualifies that appeal by warning there is no guarantee distributions will always be paid or paid at a relatively stable rate.

There is another complication, and it is an important one. Goldman says a significant portion of those distributions may be treated as return of capital for tax purposes. That does not automatically mean something negative, but it does mean investors cannot lazily treat every monthly payment as pure earned income in the ordinary sense. A return of capital reduces an investor’s basis in the shares, which can alter the tax outcome when the shares are eventually sold. The prospectus repeatedly notes that the future tax character of distributions cannot be guaranteed, and that under some market conditions there may be little or no return of capital at all, with distributions instead taxed as ordinary income.

The Product Reflects a Broader Industry Shift, Not Just a Goldman Experiment

Reuters noted that this filing arrived only days after Morgan Stanley launched its own spot bitcoin fund, the Morgan Stanley Bitcoin Trust ETF, which helps frame what is happening at the industry level. Big institutions are no longer deciding only whether to participate in bitcoin. They are increasingly deciding what form of participation fits their brand, their distribution model, and the temperament of their clients. One firm chooses direct spot exposure. Another chooses income-enhanced exposure. This is what market maturity looks like inside finance: the asset stops being a single story and starts becoming a shelf of differentiated products.

That shift matters because it changes the tone of institutional crypto adoption. The early stage was about validation. The next stage was about access. This stage is about customization. Once firms start building buffered, capped, leveraged, yield-oriented, or options-overwritten versions of an asset, the conversation has moved beyond legitimacy and into product engineering. Bitcoin is no longer only being sold as conviction. It is being sold as a configurable exposure. Goldman’s filing is one of the clearest examples of that transition.

The Timing Also Tells You Something About the Demand Goldman Is Chasing

Reuters reported that bitcoin was down nearly 15% year to date and trading far below its previous peak at the time of the filing, while risk sentiment more broadly had been pressured by weak tech stocks, precious-metal volatility, and geopolitical tension involving the United States, Israel, and Iran. In that kind of market environment, income strategies often become easier to pitch than pure upside narratives, because investors are more willing to hear about premium collection, partial cushioning, and distribution flows than they are to simply embrace raw volatility and wait for price appreciation to resume.

That does not mean the strategy becomes easy to sell. Reuters cited Morningstar ETF analyst Bryan Armour, who argued that while the additional income can sound appealing, the product may still be a difficult sell because investors retain significant downside exposure. That is a fair warning, and it goes to the heart of the product’s tension. The structure can make bitcoin exposure feel more tolerable on paper, but it cannot erase the fact that investors are still allocating into a volatile asset with meaningful downside and structurally limited upside participation once the overwritten calls start biting.

There Are Still Important Unknowns, Including the Fee

For all the attention on the filing, several commercial details remain unfinished. The prospectus leaves the ticker, exchange, and management fee blank, and Reuters separately noted that Goldman had not yet disclosed the proposed fee structure. That is not a small omission. In a competitive ETF market, fee levels often shape adoption as much as strategy descriptions do, especially when advisors are comparing a more complex income product against cheaper and simpler spot alternatives. Until the final fee is known, no one can fully assess how aggressive Goldman intends to be in positioning the product.

The prospectus also makes clear that the fund is newly organized and has not commenced operations, which means investors do not yet have live portfolio behavior, historical turnover, or actual distribution records to evaluate. Everything for now rests on the prospectus, the adviser’s design, and the assumptions investors make about how the strategy will behave once exposed to real market conditions. That uncertainty is normal for a new fund launch, but it matters even more when the strategy is built around an asset as volatile as bitcoin and a derivative overlay that can materially affect outcomes.

What This Filing Really Says About Bitcoin’s Place Inside Traditional Finance

The deepest significance of this filing is not that Goldman Sachs has suddenly “embraced” bitcoin in some emotional or ideological way. The more interesting point is that Goldman now appears comfortable treating bitcoin as material for familiar institutional manufacturing. That may be the clearest sign yet that bitcoin has crossed into another stage of financial normalization. Once an asset is being carved into income products rather than merely wrapped for access, the industry has already moved beyond the first argument about whether it belongs.

There is something revealing in that progression. Bitcoin began as an outsider asset, then became a speculative macro trade, then became a regulated ETF holding, and now it is being reshaped into an option-income strategy designed for investors who want exposure without accepting the full emotional burden of exposure. That does not make the product unimportant. It arguably makes it more important, because it shows how the financial system absorbs unfamiliar assets over time. It does not merely admit them. It rebuilds them into forms that suit existing habits. It trims the edges, adds the overlays, and gives the final result a narrative that can sit more comfortably in a diversified portfolio.

Final Take

Goldman Sachs filing for the Bitcoin Premium Income ETF is not just another headline about institutional crypto. It is a sign that the market has moved into a more advanced and more revealing stage, where the biggest firms are no longer asking only how to offer bitcoin, but how to redesign bitcoin for different client appetites. This proposed fund seeks current income, uses spot Bitcoin ETPs and related options rather than direct bitcoin ownership, may employ a 40% to 100% overwrite ratio, expects monthly distributions, and warns that a significant share of those payments may be return of capital rather than simple investment income. It is a product built around compromise by design: less raw upside, still real downside, more engineered cash flow, and a much more familiar institutional shape.

That is why #GoldmanSachsFilesforBitcoinIncome matters. The real story is not just that Goldman wants a bitcoin-linked ETF on the shelf. The real story is that bitcoin is now being treated as something Wall Street can slice, hedge, monetize, and distribute in forms tailored to investor comfort. Whether that looks like progress, dilution, or simple inevitability depends on how one has always viewed bitcoin, but as a market signal, the message is hard to miss: institutional finance is no longer standing outside the asset class trying to understand it. It is now inside the structure, redesigning it.