I didn't plan to write about remittances and Midnight in the same sentence. My mental model of privacy blockchains placed them firmly in the DeFi and developer category, interesting to a specific audience, irrelevant to the person sending money home from a warehouse job in Dubai to a family in Manila.

Then I found the MoneyGram partnership, and my mental model needed updating.

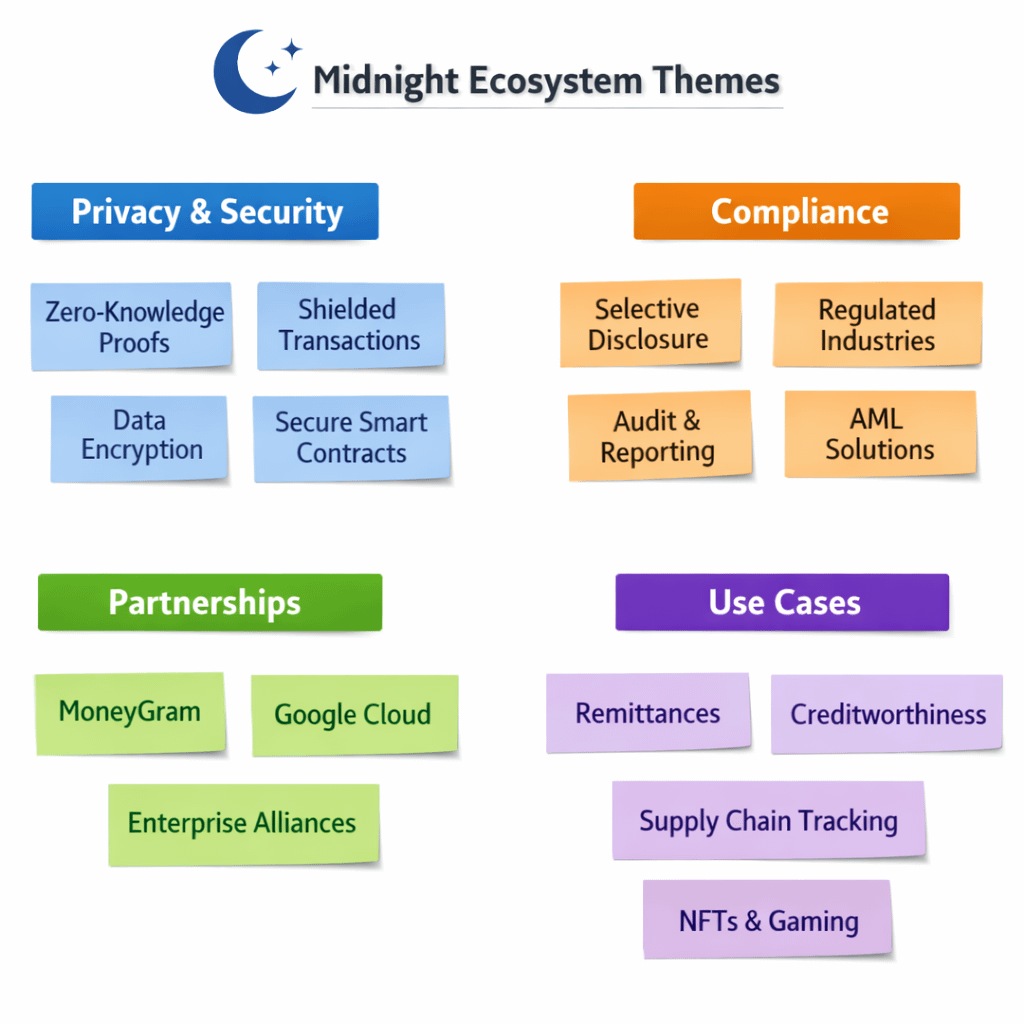

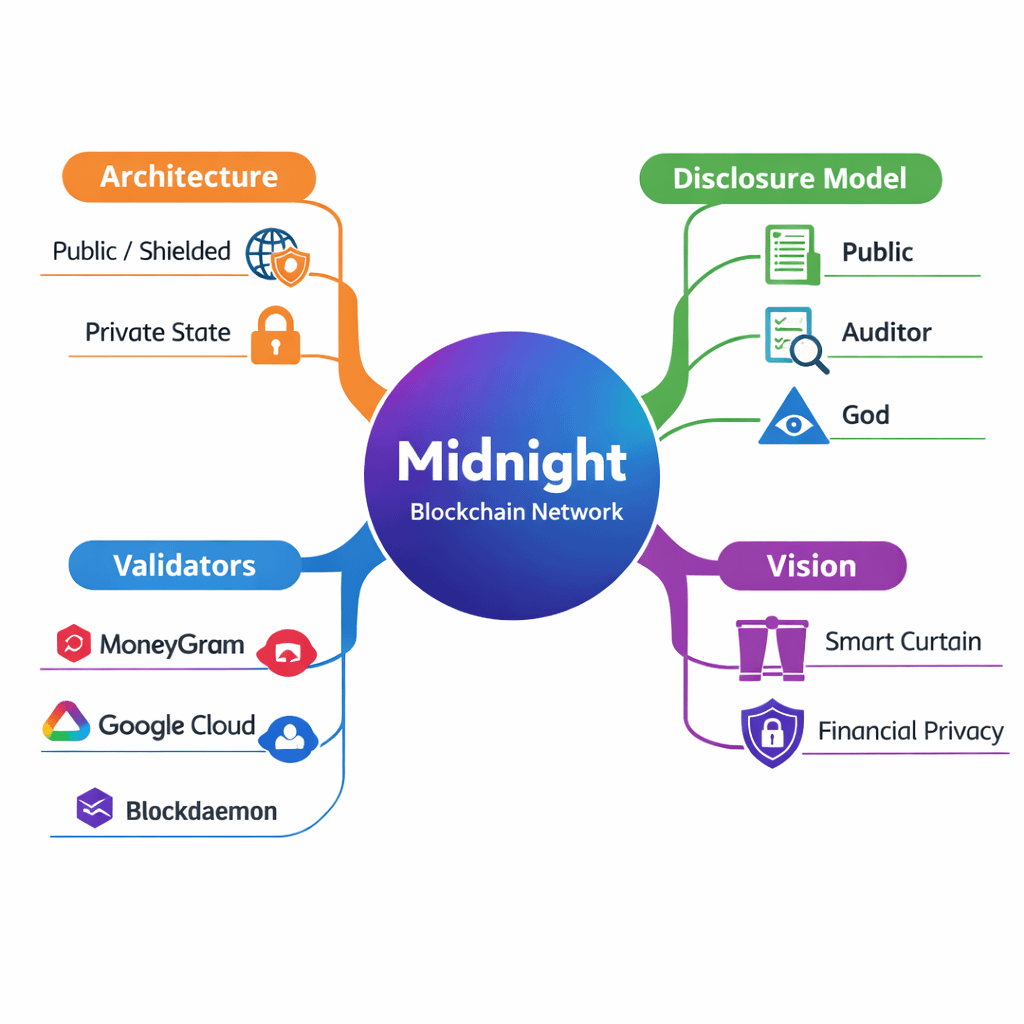

Midnight's institutional validator list includes Google Cloud, Blockdaemon, Shielded Technologies, AlphaTON Capital, and MoneyGram. MoneyGram is not a blockchain-native company chasing a trend. They process remittances for millions of people in corridors where financial privacy isn't a philosophical preference it's a safety requirement. The fact that they're running a validator node on Midnight tells me something I couldn't learn from a whitepaper.

Let me explain why remittances are the use case I keep returning to.

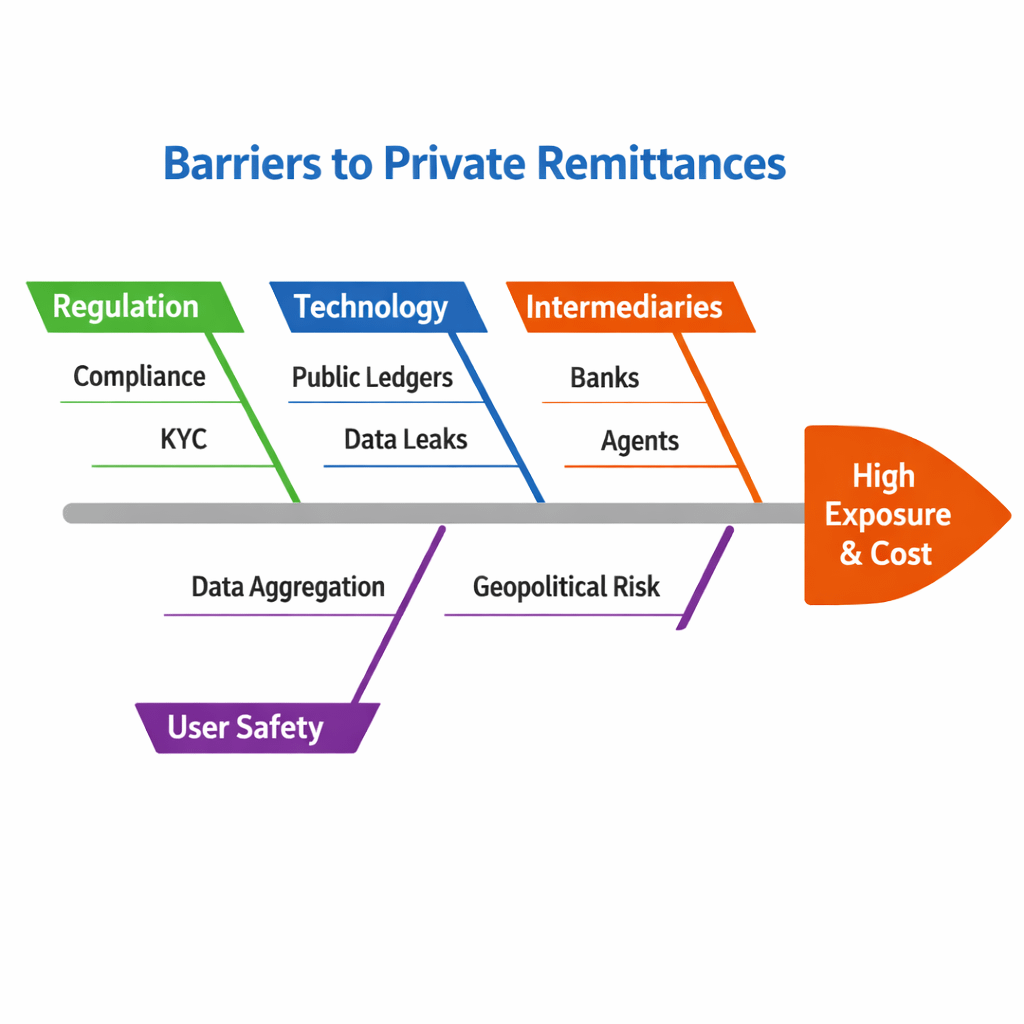

The global remittance market runs on a painful irony. The people who most need affordable, private money transfers are exactly the people most exposed on traditional systems. A construction worker in Qatar sending money home has their transaction amount, timing, and frequency permanently recorded by every intermediary in the chain. That data gets aggregated, analyzed, and occasionally used in ways the sender never consented to. In some geopolitical contexts, that exposure is dangerous. In most, it's simply unfair.

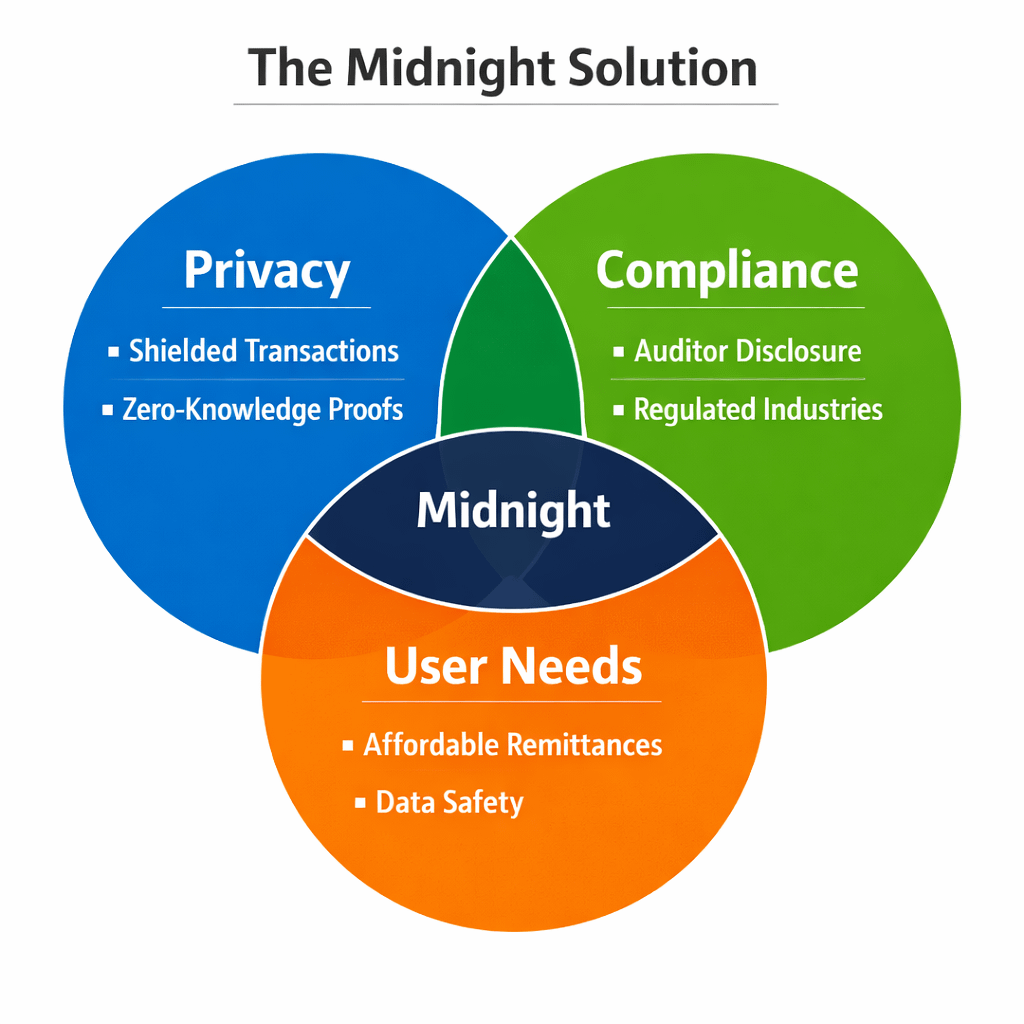

Midnight addresses this through selective disclosure the ability to prove facts about data without revealing the data itself enabling blockchain adoption in regulated industries like finance and government services where data protection is not just important but legally required. That framing matters for remittances specifically. The compliance requirement isn't going away. Regulators need to know that money isn't funding prohibited activity. The question is whether proving compliance requires exposing every financial detail of every sender's life. Midnight's answer is no, and the technical architecture backs that up.

The network processes two types of transactions: standard public transactions that function like traditional blockchain operations, and shielded transactions that use zero-knowledge proofs to maintain privacy. Private state is stored locally by users and never exposed to the network. In practical terms, a remittance sender could prove they're a verified account holder and that the transfer meets compliance thresholds without broadcasting their transaction history to anyone running a node. That's a meaningful privacy improvement over every existing corridor.

Here's where I slow down because I've been too positive for two paragraphs.

Midnight's federated mainnet launch is expected in late March 2026, which will transition the project from test environments to a production chain where early private smart contracts and dApps can go live. That launch hasn't happened yet as I write this. The MoneyGram partnership exists at the validator level, not at the application layer. There's a meaningful distance between "MoneyGram runs a node" and "MoneyGram routes remittances through Midnight's privacy infrastructure at scale." I want to be careful not to collapse that distance prematurely.

One project in the Midnight ecosystem aims to let users demonstrate creditworthiness and repayment history while keeping specific loan amounts and merchant interactions private, anchoring identity in verifiable economic behavior rather than exposed transaction records. That's the shape of what a privacy-preserving financial product could look like on this network. It's still early. It's still conceptual in places. But the direction is correct.

Hoskinson described Midnight as a smart curtain for blockchain data, letting users share only what they choose while keeping the rest private balancing transparency and confidentiality through multiple disclosure views categorized as public, auditor, and god each with different access levels. The three-tier disclosure model is the detail I find most interesting for regulated remittances. A compliance auditor sees what they need without seeing everything. A recipient confirms receipt without exposing their full wallet history. A sender proves identity without surrendering their financial biography.

Whether that model survives contact with actual regulators in actual jurisdictions is still an open question.

But MoneyGram doesn't run validator nodes on projects they've dismissed.

That's the data point I keep coming back to.