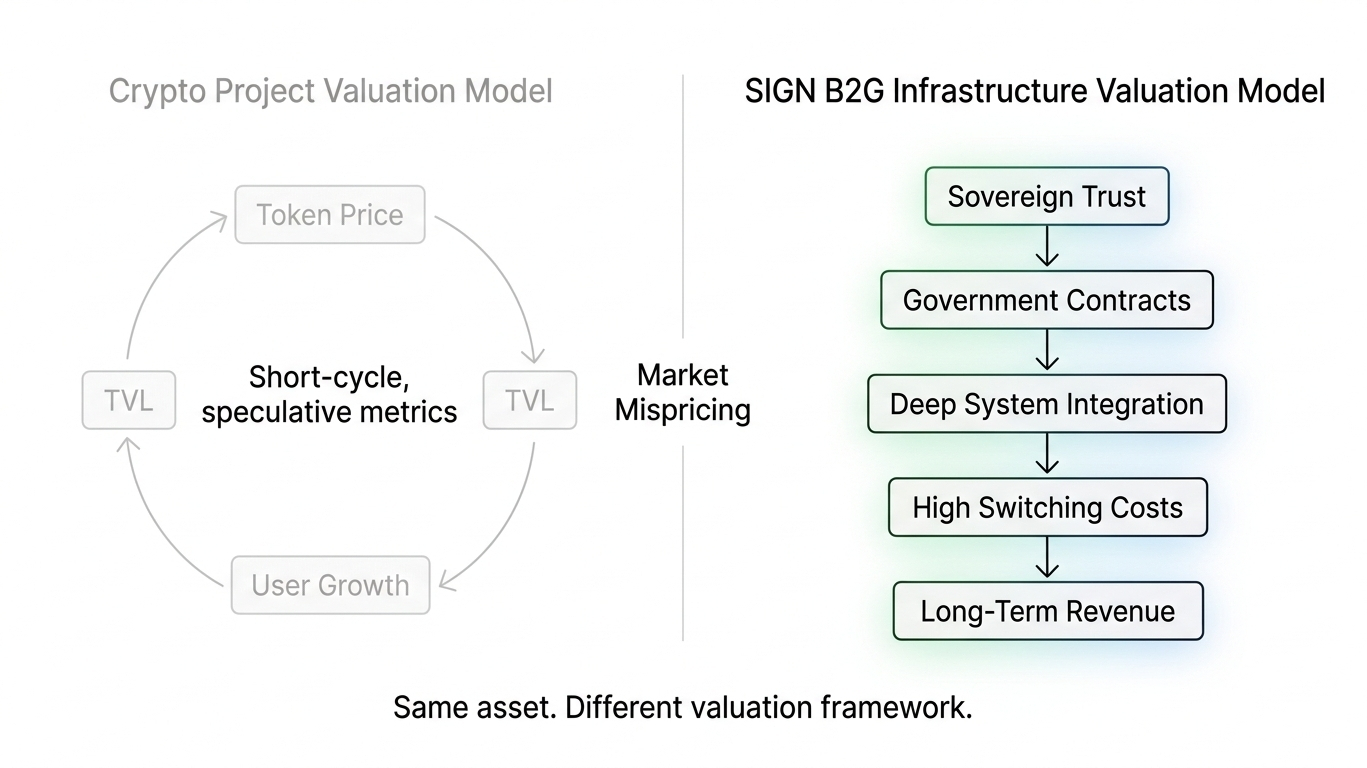

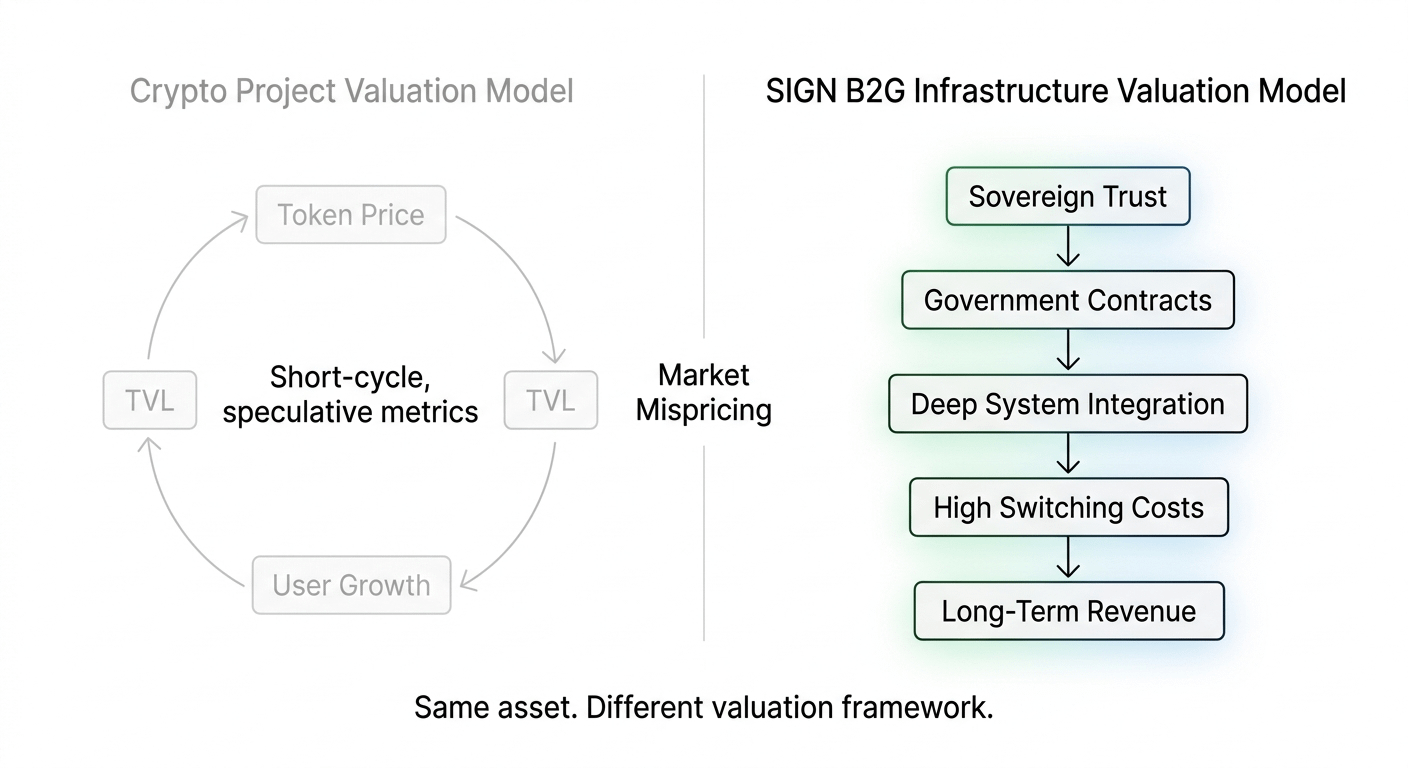

I have noticed something about the way most people position Sign Network in their mental model of the crypto landscape. They place it next to other attestation protocols, other identity layers, other token distribution platforms — and they compare market caps, token unlocks, and TVL figures as if Sign is competing in that category. It is not. Sign's own documentation makes this explicit, and the framing it uses is not subtle. Sign describes itself as a B2G proprietary technology company. Not a protocol. Not a DeFi primitive. A business-to-government technology company — the same structural category as Palantir, Anduril, and SpaceX. That comparison is not aspirational. It is architectural. And the gap between how crypto prices B2G proprietary technology companies and how public markets price them is one of the most significant mispricings in the current cycle.

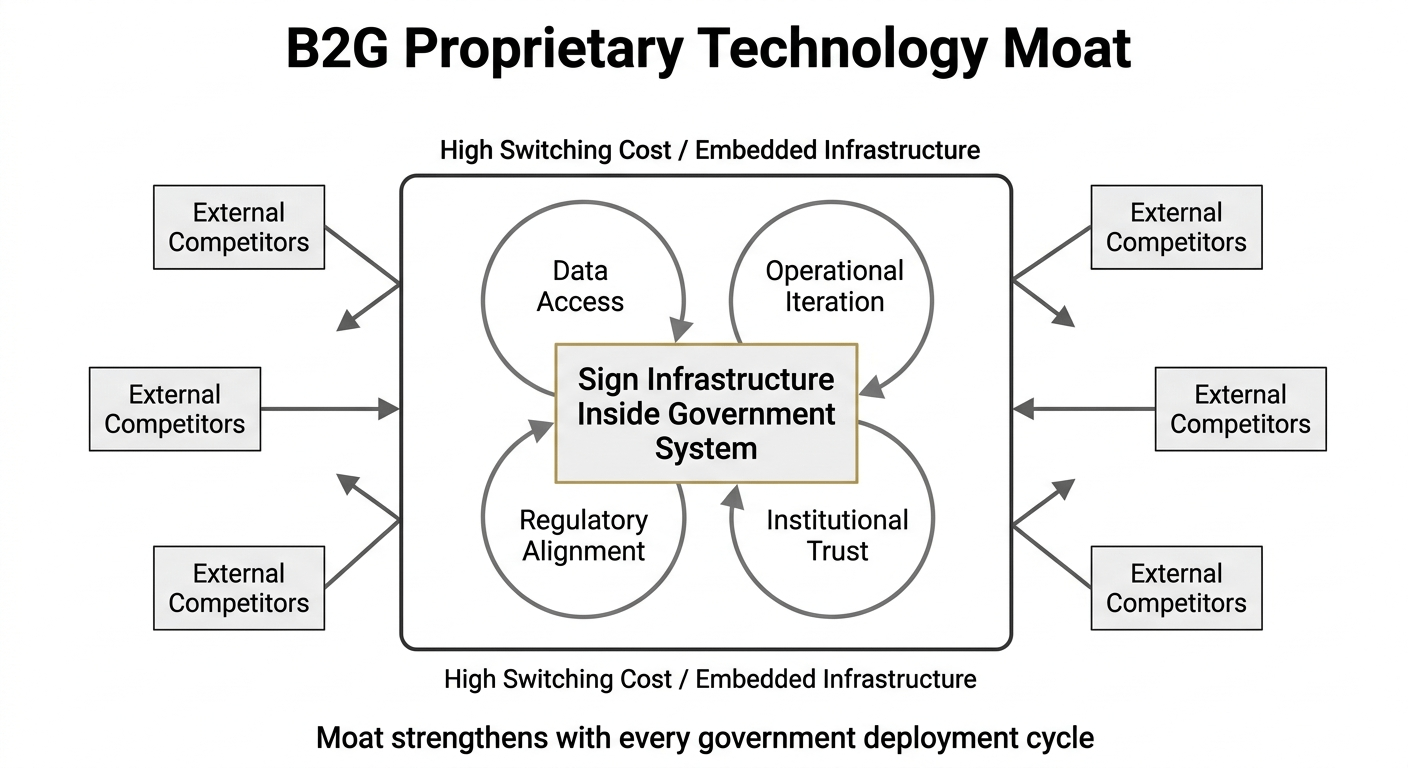

The B2G model works differently from everything else in crypto. In B2B or B2C markets, the primary challenge is product-market fit — building something people want and distributing it efficiently. In B2G, the primary challenge is trust. Governments do not take risks on unknown vendors. They do not integrate new infrastructure because the whitepaper is technically elegant. They integrate after years of relationship building, legal review, security auditing, and procurement processes that filter out every company that cannot demonstrate sovereign-grade reliability. That barrier is extraordinarily high. Sign has already crossed it. The Kyrgyz Republic's National Bank signed a technical service agreement — not an MOU, not a letter of intent, but a technical service agreement — for Sign to build the Digital SOM CBDC. That crossing of the government trust barrier is not a milestone. It is a moat. Because once Sign is inside a sovereign system, the switching costs are so high, the integration so deep, and the institutional relationships so embedded that the contract effectively becomes permanent infrastructure.

This is what Palantir understood before anyone else in the enterprise technology space. Proprietary technology does not compound because you own the code. It compounds because you own the systems that cannot be replicated without operating at the same scale, in the same context, with the same iteration loop running continuously inside the same sovereign institution. Every government contract Sign executes teaches Sign something about sovereign digital infrastructure that no competitor can learn from the outside. How do you bridge traditional banking systems with stablecoin infrastructure while maintaining AML compliance? How do you issue cryptographically signed identity credentials that clear across agencies in real time without creating centralized data silos? These problems are invisible unless you are operating inside the system. Sign is operating inside the system. The data, the iteration loop, and the sovereign context compound into a moat that cannot be purchased or replicated — only earned through deployment.

Sign's documentation is precise about what it is building at the foundational level. Two systems. A digital money system — a sovereign digital currency rail supporting CBDCs and regulated stablecoins, with Sign's digital currency system targeting national-scale deployment by Q3 2026, serving millions of users as the core financial infrastructure of entire economies. And a digital identity system — a national identity and verifiable credentials layer where governments issue cryptographically signed claims covering identity, licenses, and permissions that verify across agencies and regulated operators in real time, without requiring centralized data storage. Those two systems are not products. They are the foundational infrastructure layer on top of which every other public service module — taxation, welfare distribution, voting — can be built. Sign is not building an app. It is building the operating system that government applications run on.

The price today is $0.05308, up 2.89% on the session and holding gains from yesterday's 9.56% surge. Volume came in at 187.05 million SIGN. RSI is at 69.78 — the highest reading in Sign's entire recovery cycle, pressing directly at the overbought threshold without yet crossing it. The EMA structure shows Sign trading above its 20-period at $0.05007, its 50-period at $0.04718, and its 200-period at $0.04075 simultaneously, with MACD DIF at 0.00250 against DEA at 0.00223 — the strongest momentum reading this recovery has produced. The chart confirmed its bottom at $0.03906 and has not looked back. The technical picture is not predicting what Sign is building. It is beginning to reflect that the market is finally reading it correctly.

Here is the risk I would sit with honestly. The B2G model that Sign is executing is the most defensible business model in technology — but it is also the slowest to generate revenue at the scale the architecture implies. Sign has three new initiatives launching in 2026: a Bank-Stablecoin Integration Middleware that bridges traditional banking systems with stablecoin infrastructure through virtual accounts and verifiable KYC systems; a Regulatory OS that maps real-world identities to on-chain activity and applies regulatory rules in real time across licensed platforms; and a Data Exchange Layer that records inter-agency data interactions as verifiable, append-only logs without storing raw data. Each of those initiatives requires government procurement approval, regulatory sign-off, and integration cycles that do not compress regardless of how ready the technology is. Sign is asking the market to hold through the deployment timeline — and that is a different psychological demand than holding through a protocol launch.

The second risk is the sovereign AI thesis that Sign's documentation introduces as the long-term endgame. As governments become fully digitized on Sign's infrastructure, AI systems gain real-time visibility into state data and the ability to act through programmable interfaces — enabling a new model of governance that is real-time, data-driven, and automated. That vision is architecturally coherent and the UAE's own digital government strategy supports the direction. But sovereign AI governance running on Sign's infrastructure is a 2028 or 2030 story, not a 2026 story. Anyone pricing SIGN today primarily on the sovereign AI thesis is extending their time horizon beyond what the current deployment pipeline can validate. The Q3 2026 digital currency deployment is the signal that matters now. The sovereign AI thesis is the signal that matters later.

What would make me more constructive on Sign's B2G thesis is specific. I want to see the Q3 2026 digital currency system deployment happen on schedule — because a national-scale CBDC going live is the moment Sign's proprietary technology moat becomes visible to markets that currently cannot see it. I want to see at least one of the three 2026 initiatives — the Bank-Stablecoin Middleware, the Regulatory OS, or the Data Exchange Layer — enter live deployment with a named sovereign partner before year end. And I want to see Sign's revenue reflect B2G income appearing alongside its existing $15 million B2C baseline, because the moment government contracts generate a distinct revenue line, the entire valuation framework for SIGN has to change.

Do not watch where SIGN is trading. Watch whether Sign's Q3 2026 digital currency system deploys on schedule at national scale. Palantir traded at a fraction of its eventual valuation for years while its government contracts were in deployment. The rerating happened when the sovereign systems went live and the moat became undeniable. Sign is at that same inflection point. The market has not yet priced what a B2G proprietary technology company with sovereign contracts, a Q3 2026 deployment deadline, and a compounding iteration moat is actually worth.

@SignOfficial #SignDigitalSovereignInfra $SIGN