Look, I understand why projects like Open Ledger are suddenly getting attention.

Accounts payable is boring. Painfully boring. It is full of invoices nobody wants to process, approvals nobody wants to chase, and finance teams buried under spreadsheets that should have died sometime around 2007. So when a company walks into the room promising AI automation, blockchain verification, real-time settlement, fraud reduction, and “shared trust infrastructure,” executives lean forward immediately.

That pitch writes itself.

And honestly,@OpenLedger on the surface, it sounds reasonable. Companies lose money through invoice fraud. Vendors get paid late. ERP systems barely communicate with each other. Finance departments waste thousands of hours reconciling records across disconnected software. The entire process feels old because, in many cases, it is old.

So Open Ledger arrives and says: let’s put a distributed ledger underneath payable AI systems so everyone shares the same transaction truth. Suppliers, buyers, finance teams, AI agents, payment processors. One synchronized record layer. One verification system. Less fraud. Less reconciliation. More automation.

Clean story.

The first thing you learn after covering enterprise technology for twenty years is that every infrastructure startup claims the same thing: “We reduce complexity.” What they usually mean is that they are adding a fresh layer of abstraction on top of old complexity and hoping nobody notices the stack getting taller.

That is the first catch here.

Because payable systems are already complicated enough before you inject AI models, distributed ledgers, token incentives, verification nodes, governance mechanisms, and cross-platform coordination protocols into the picture.

People outside enterprise finance do not fully appreciate how messy these environments actually are. A large corporation may operate across fifty countries using different tax systems, banking relationships, invoice standards, procurement software, and compliance frameworks. Some divisions are still running software written when George Bush was president.@OpenLedger Others are using cloud systems stitched together after acquisitions. Half the integrations barely work. The other half are maintained by consultants nobody can afford to lose.

Now imagine dropping a blockchain coordination layer into that ecosystem.

It sounds tidy. On paper, at least.

But once you peel back the marketing, the glue starts to melt.

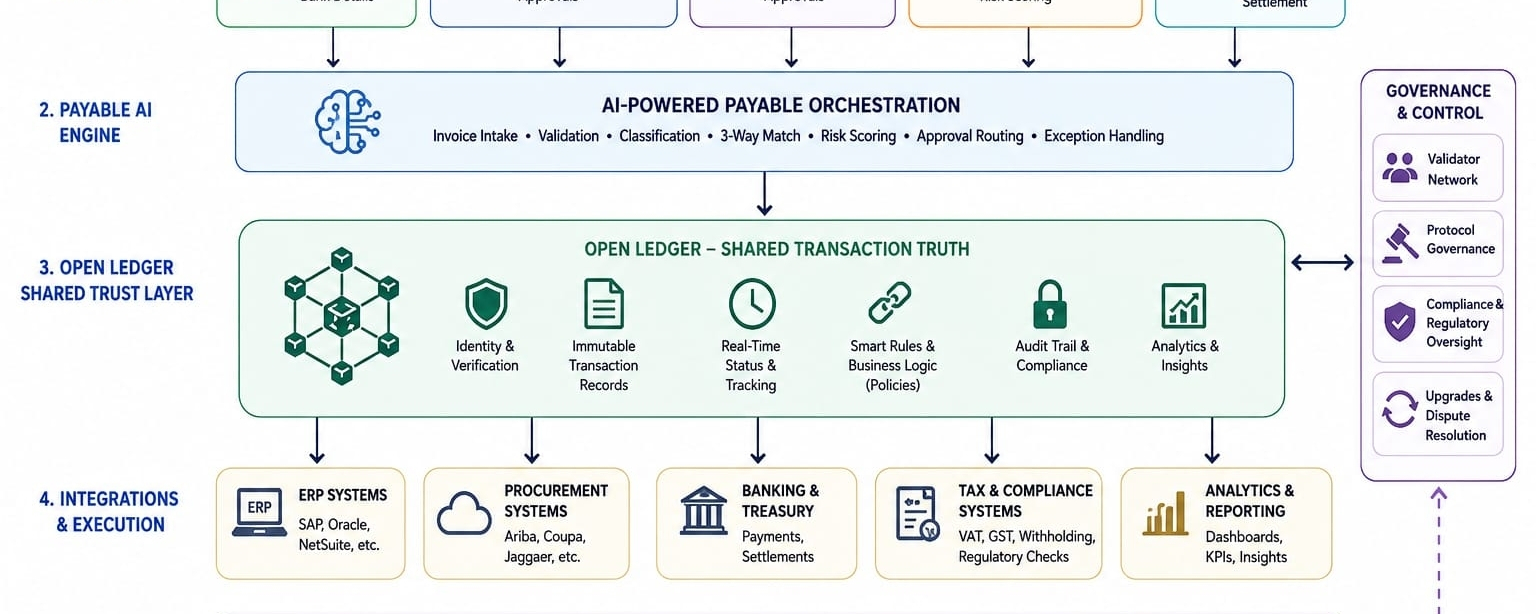

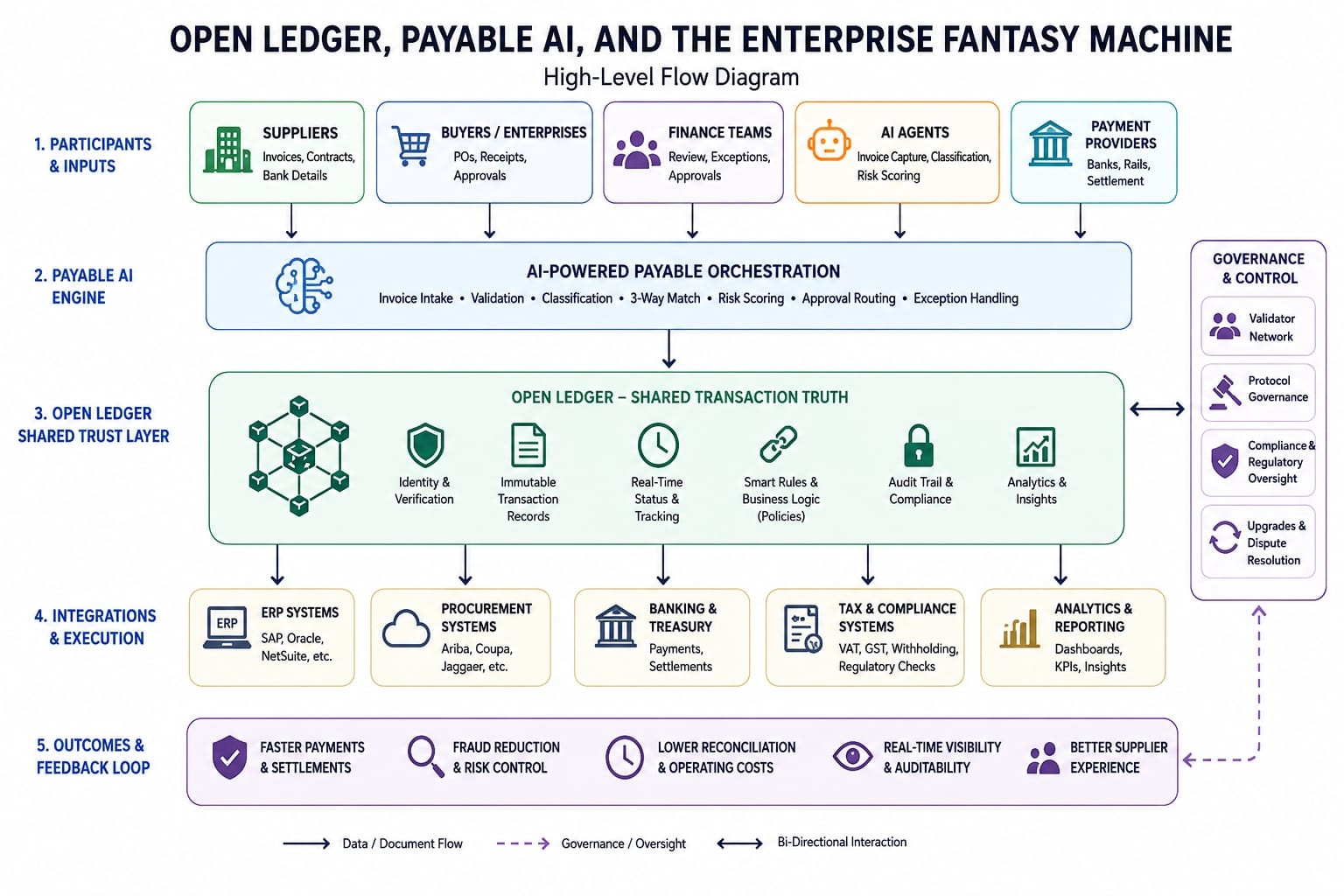

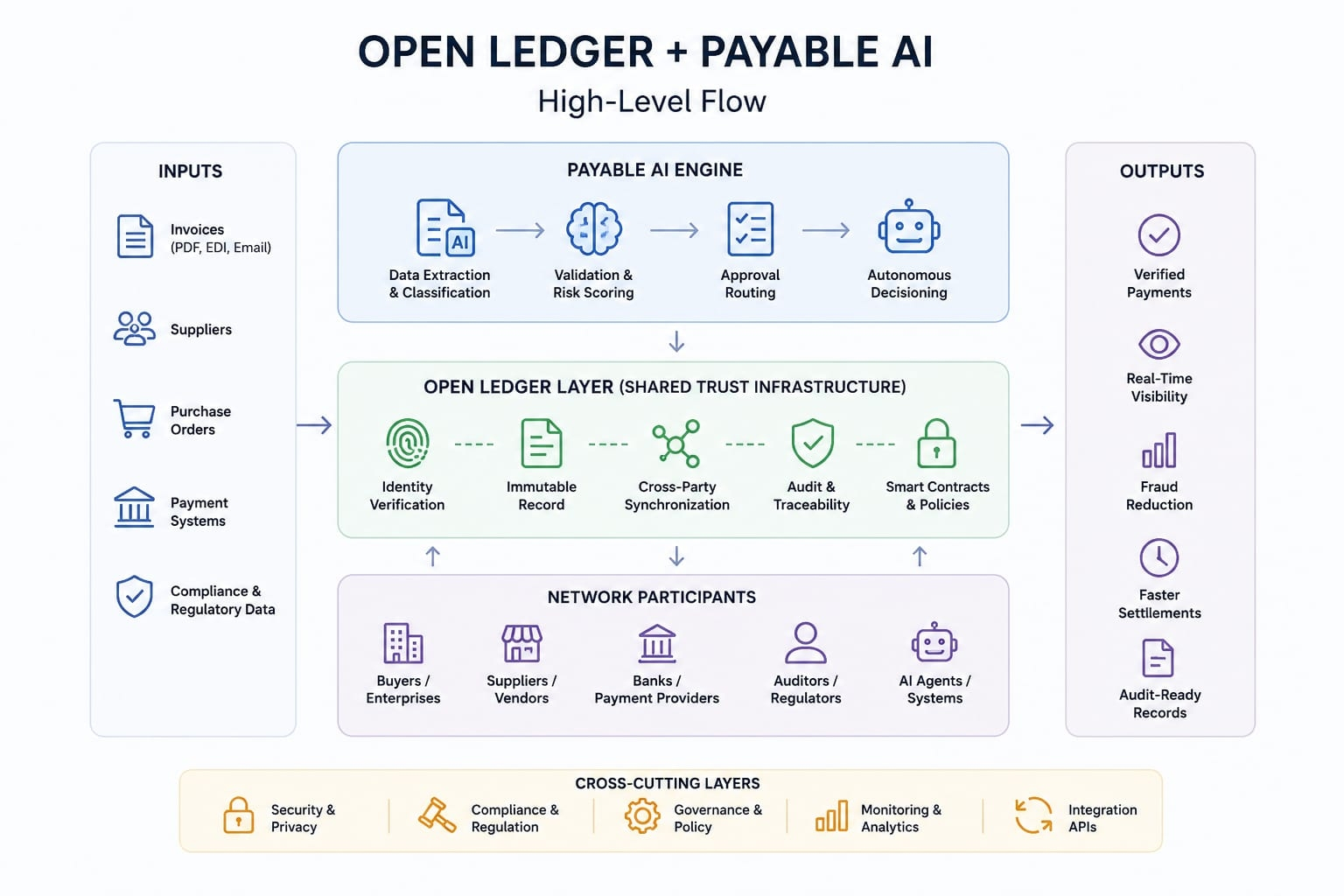

The core problem Open Ledger claims to fix is trust fragmentation. Their argument is that AI-powered payable systems cannot function properly if transaction records remain siloed across disconnected databases. So the ledger becomes the shared source of truth. Suppliers get verified identities. Invoice approvals become traceable. AI systems operate against synchronized records instead of fragmented internal systems.

Fine. Reasonable enough.

But here is what the pitch quietly avoids mentioning: most enterprise finance problems are not caused by a lack of cryptographic verification.

They are caused by humans.

Humans entering wrong invoice data. Humans bypassing approval chains. Humans negotiating weird supplier contracts. Humans forgetting compliance steps. Humans sending payment requests through email because the “official system” takes too long. Humans improvising around broken workflows because the real world never behaves like the software diagram.

Technology companies hate admitting this because it ruins the fantasy of elegant automation.

The reality is uglier. Most corporate finance departments operate through a combination of software, tribal knowledge, temporary workarounds, and institutional memory held together by exhausted employees who know which buttons not to press.

Open Ledger does not remove that chaos. It records the chaos more systematically.

That distinction matters.

Then there is the decentralization question. Let’s be honest here. Most enterprise blockchain projects are decentralized in the same way airport food courts are “global cuisine.” Technically true. Spiritually questionable.

Who actually controls the validators? Who controls protocol upgrades? Who maintains the APIs? Who decides compliance rules? Who can reverse transactions under regulatory pressure? Because the moment enterprise clients enter the picture, decentralization starts colliding with legal reality.

Large corporations do not want uncontrolled infrastructure. Regulators certainly do not. Banks absolutely do not.

So what usually happens? The system slowly recentralizes itself around a handful of major operators, infrastructure providers, or governance entities while continuing to market itself as decentralized because the word still attracts investors.

The token model deserves skepticism too.

Whenever a project introduces a token into enterprise infrastructure, you should immediately ask a very simple question: does the token exist because the system genuinely needs it, or because someone wanted an asset they could sell?

That question cuts through an enormous amount of noise.

Open Ledger supporters will argue the token coordinates incentives. Validators stake collateral. Participants pay network fees. Governance becomes distributed. Fine. Maybe.

But finance departments do not enjoy dealing with volatile digital assets. CFOs want predictable costs. Auditors want accounting clarity. Regulators want identifiable liability structures. Nobody managing corporate treasury operations wants to explain to the board why invoice processing costs suddenly moved with crypto markets.

That creates tension right at the center of the model.

Either the token becomes operationally irrelevant, in which case the blockchain layer starts looking decorative, or the token becomes deeply integrated, in which case enterprise adoption becomes harder because corporations dislike dependency on speculative assets.

There is another issue hiding underneath all this.

AI systems themselves are unreliable in subtle ways.

The marketing around payable AI makes it sound like machines can now understand financial workflows with near-human competence. They cannot. Not consistently. These systems still hallucinate classifications, misread invoices, struggle with edge cases, and fail in situations where context matters more than pattern recognition.

And payable environments are full of edge cases.

A supplier changes banking details after an acquisition. A contract amendment modifies payment terms mid-quarter. A regional tax exception applies to one shipment but not another. A procurement manager approves something verbally instead of through the official system because a factory shipment is stuck at customs.

Humans adapt to these situations through experience and improvisation. AI systems often do not.

So what happens when the machine makes the wrong call? Who carries liability when an autonomous payable agent approves fraudulent invoices because the verification layer trusted corrupted upstream data? The blockchain record may prove exactly what happened, but that does not recover lost money.

This is the uncomfortable part infrastructure startups rarely discuss publicly: transparency is not the same thing as reliability.

A ledger can record failure beautifully.

It cannot prevent failure automatically.

And then we get to the labor issue. This one always gets buried under the automation narrative.

A huge amount of “AI automation” still depends on invisible human intervention. Low-confidence invoice extractions get routed to human reviewers. Exceptions go to outsourced finance teams. Compliance ambiguities get escalated manually. Fraud investigations still require humans to interpret context.

The machine appears autonomous because people are cleaning up its mistakes quietly in the background.

Silicon Valley has been running this trick for years. Build software that looks intelligent, hide the human labor supporting it, then market the entire system as autonomous infrastructure.

The economics matter too.

Who gets rich if Open Ledger succeeds? Probably not the finance clerks losing their jobs to automation. Probably not the suppliers paying additional network fees. More likely the infrastructure operators, token holders, early investors, consultants, and integration vendors charging enterprises millions to stitch these systems into legacy environments.

Enterprise software history follows a predictable pattern. The promised efficiency gains often arrive eventually, but only after companies spend enormous amounts of money navigating years of implementation pain.

And that is assuming the system works at scale.

Because scale changes everything.

A demo environment processing clean invoices between cooperative parties is easy. A multinational enterprise operating across dozens of jurisdictions with conflicting regulations, legacy software, unreliable suppliers, and constant audit pressure is something else entirely.

This is where many “next generation infrastructure” projects quietly break apart.

Not because the core idea is stupid. Sometimes the idea is perfectly logical. The problem is that real-world business environments are chaotic systems filled with incentives, politics, compliance burdens, and operational compromises that software engineers rarely control.

That is why I remain cautious whenever a company claims it is rebuilding trust infrastructure for global finance.

Trust is not just a technical problem. It is a human one. A legal one. A political one. A liability problem. A governance problem. And sometimes a very ordinary problem involving somebody in accounting who forgot to update a supplier record before leaving for vacation.

Open Ledger may solve parts of the coordination issue. It may even improve visibility inside payable systems. But the deeper sales pitch — that shared ledgers and AI agents will somehow cleanly automate the messiness of enterprise finance — feels suspiciously familiar.

Because every decade, the industry invents another architecture that promises to remove friction from human institutions.

And every decade, the humans remain.