The most revealing conversations about crypto economics don’t happen on stages. They happen in the boring places where someone is trying to make a number behave.

The developer keeps clicking the same cell—average fee per transaction—and changing it by a few cents, then watching the monthly total jump by thousands. Not because the app suddenly got bigger, but because the token that pays for gas decided to have a week.

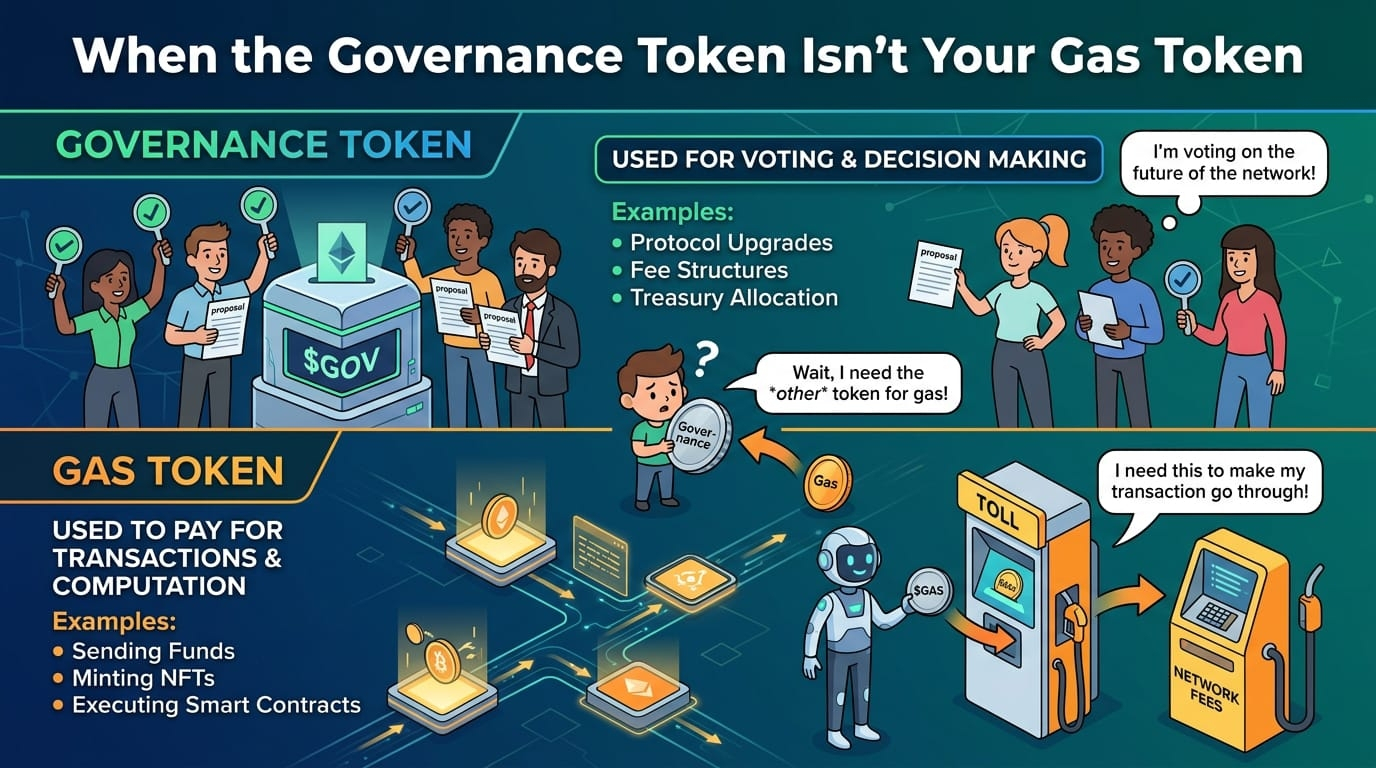

If you’ve built on a chain where the governance token is also the fee token, you recognize the rhythm. When the market is calm, everything feels fine. When attention spikes, fees spike, too. Then the people who actually use the network—the ones clicking “send,” “submit,” “mint,” “verify”—become collateral damage in a price fight they didn’t start and can’t finish.

The awkward truth is that “gas” is not a philosophy. It’s plumbing. It should be priced like a utility, not like a lottery ticket. But on many networks, the token that’s supposed to pay for that plumbing also carries every other meaning: ownership, governance, speculation, identity, status. One asset, too many jobs.

That’s why the idea of separating the governance token from the gas token keeps resurfacing. It’s not a new moral stance. It’s a response to a pattern that repeats so reliably you can set your watch by it: when the same token is used for security, governance, and fees, every incentive and every surge hits the same choke point.

You can see it on the user side first. Someone wants to try an app. They don’t want to “enter an ecosystem.” They want to do a simple thing—sign a message, prove eligibility, store a record, pay an invoice. Instead, they’re sent on a scavenger hunt for the right token. Not because the app needs it, but because the chain does.

Then you see it in the governance layer, where the cost of “doing anything” becomes tied to a market price that has nothing to do with network health. A proposal to adjust parameters—fees, limits, throughput—gets interpreted through the lens of token price, because token price is what everyone can easily measure. Technical discussions slide into tribal ones. People argue about upgrades the way they argue about sports teams.

And you see it most painfully in operations. If your company runs an application that relies on steady transaction throughput, you don’t just want low fees. You want predictable fees. You want to tell customers what something costs without adding an asterisk that says “depending on market conditions.” You want to budget and move on.

So when Midnight describes its economic design—publicly, at least—as splitting roles between a governance/security token (often referred to as NIGHT) and a separate spendable unit used for transaction capacity (often described as DUST), it’s responding to that lived experience. The point is not that two tokens are inherently better than one. The point is that mixing utility and speculation in the same asset has a habit of turning ordinary usage into a trading problem.

When the governance token isn’t your gas token, a few things change immediately, and they’re all practical.

The first is psychological. Holding a governance token becomes a choice about participation and long-term alignment, not a requirement imposed on every user who just wants to transact. That matters if you’re trying to build systems that normal people might use without adopting a new financial identity.

The second is financial. If the spendable resource is designed to behave more like a consumable capacity unit than like the network’s flagship speculative asset, the fee experience can be made steadier. In the best case, builders can price services in something closer to actual resource use—how much computation and storage a transaction consumes—rather than in whatever the token is doing this week.

The third is political. Governance can, at least in theory, have its own cadence, rather than being constantly yanked around by fee pain. If users aren’t directly paying with the governance token every time they do anything, governance can be argued about on its merits a little more often. Not always. But more often.

None of this is automatic, and it’s worth saying that out loud because token design in crypto is often treated like a magic trick: pick the right model and the incentives will behave. They won’t. They just behave differently.

Splitting tokens introduces complexity, and complexity always charges rent.

There’s a wallet experience to think about. Two assets means two balances, and two balances means more chances for users to feel lost. If the system is designed well, that complexity is mostly hidden. If it’s designed poorly, you get a new version of the old problem: not “you need our token,” but “you need to understand our unit system.”

There’s also the question of how people acquire the spendable capacity. Midnight’s publicly described “capacity exchange” idea—letting users pay using assets from other ecosystems and converting that into usable transaction capacity—is a direct attempt to avoid the usual fee-token scavenger hunt. It’s also an area where the tradeoffs get sharp. Somebody has to provide liquidity. Somebody has to price the conversion. If that “somebody” is too centralized, you’ve built a choke point. If it’s too fragmented, you’ve built a system that works on paper and fails under load.

Then there’s governance itself. Separating tokens doesn’t fix capture. It can even complicate it. If NIGHT governs the rules that determine how capacity is issued, priced, or allocated, then governance decisions can still have major economic consequences. People will still show up with agendas. They’ll still coordinate. They’ll still attempt to shape the system in their favor. The difference is that usage doesn’t have to be the immediate battleground where those fights play out.

This is where the “infrastructure” mindset becomes more than a tagline. Infrastructure is allowed to be dull. It is supposed to be boringly reliable. The best economic designs aim for that: costs you can anticipate, mechanisms you can audit, and incentives that don’t create constant emergencies for the people trying to build and use real applications.

A two-token model is one way to chase that boringness. It’s a way of admitting that governance and fees are different kinds of problems. Governance is about power—who decides, how decisions change, and how the network defends itself. Fees are about throughput and resources, the everyday cost of asking the network to do work. When you glue those together, you don’t get elegance. You get interference.

The real test, for Midnight or anyone else attempting this separation, won’t be whether the diagrams make sense. It will be whether ordinary moments get easier.

Does a developer still need to explain token volatility to a finance lead who just wants a budget? Does a user still need to buy a special asset just to submit a private transaction? Does governance still get hijacked by fee panic every time the market heats up? And when something goes wrong—because something always goes wrong—can people trace the mechanics clearly enough to fix them without breaking trust?

If the answer to those questions is even slightly better than what we’ve come to accept as normal, then “the governance token isn’t your gas token” stops being a clever idea and starts being what it should have been all along: basic design hygiene.

#night $NIGHT @MidnightNetwork