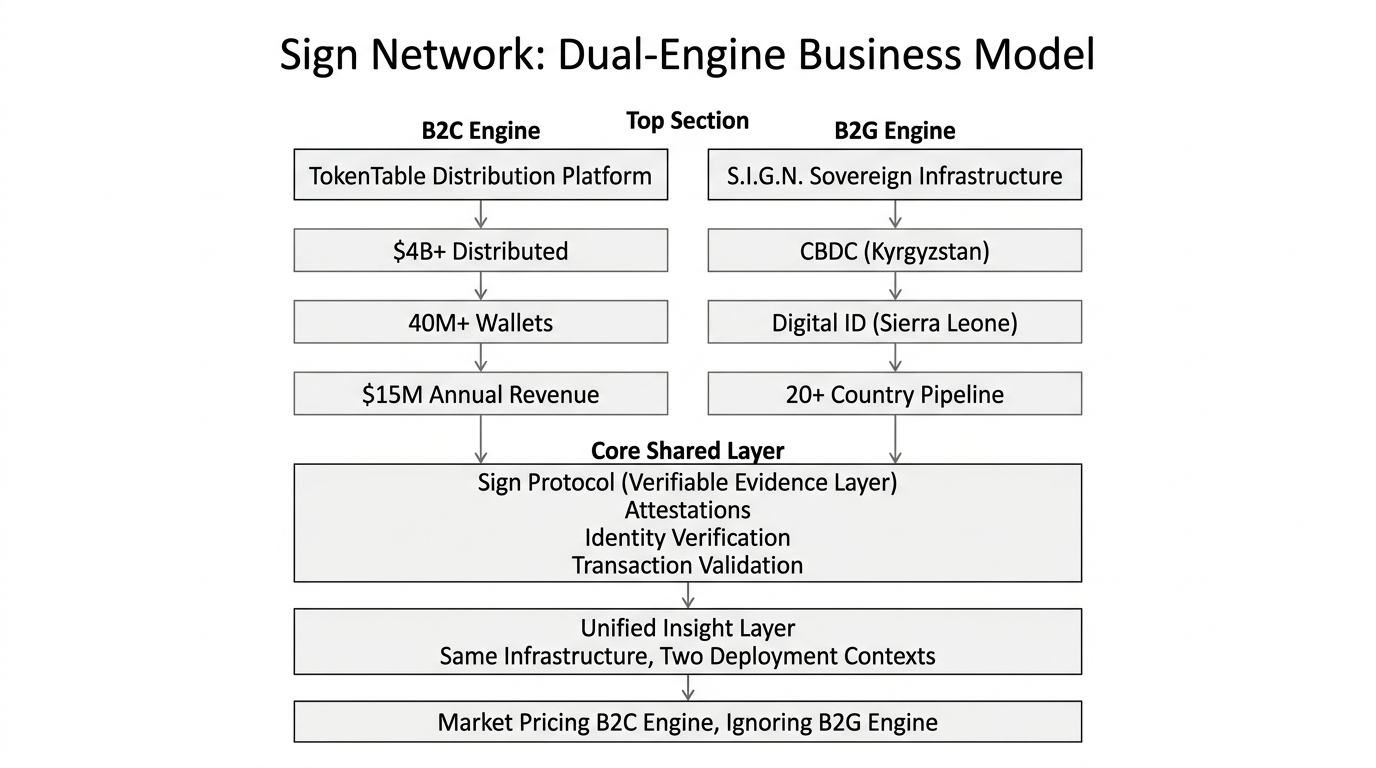

I have noticed something about the way most people analyze Sign Network. They pick a lane — either Sign is a sovereign infrastructure play targeting governments, or Sign is a token distribution platform serving crypto projects — and they build their entire thesis around that lane. What they consistently miss is that Sign is running both businesses at the same time, that the two businesses feed each other structurally, and that the market is currently pricing only the smaller of the two while the larger one sits in plain sight, unpriced.

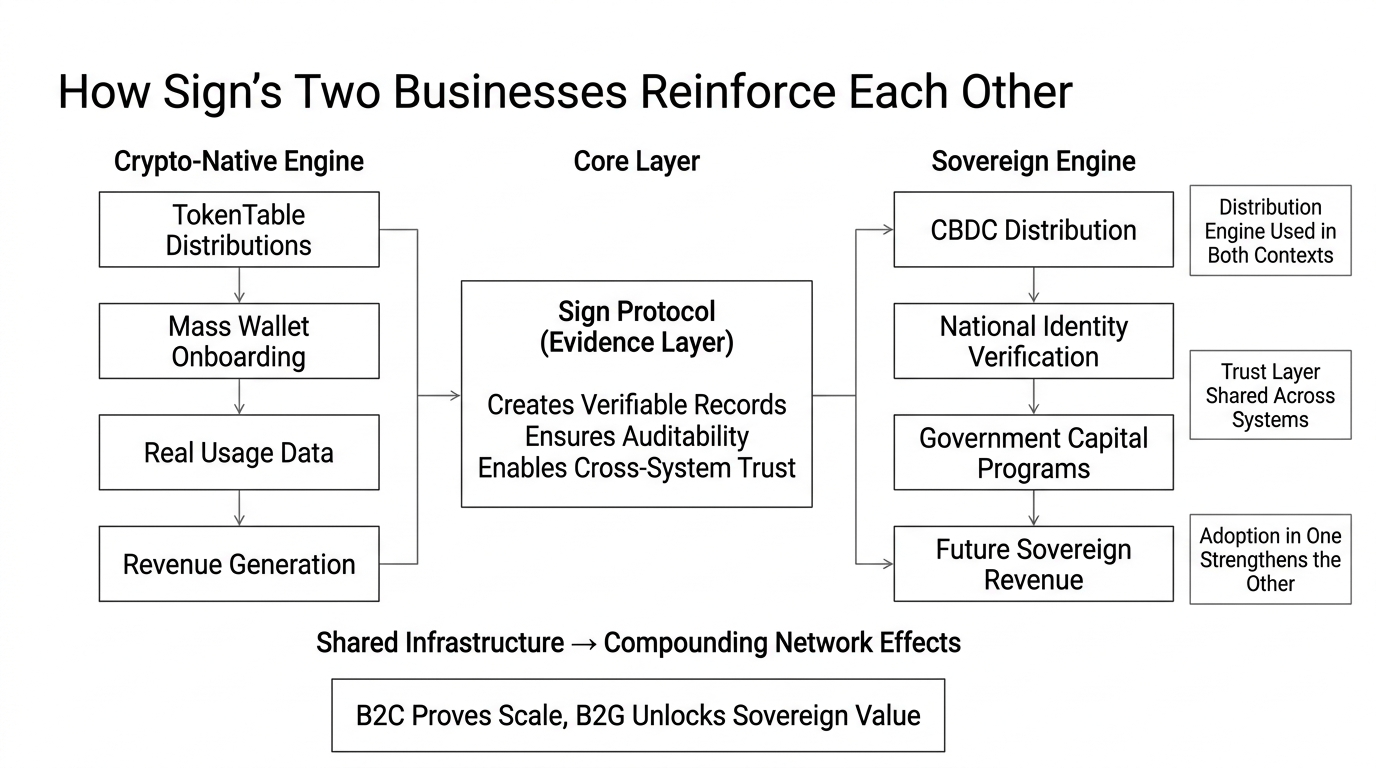

Sign's B2C engine is the one the crypto market sees. TokenTable has distributed over $4 billion in tokens across more than 40 million on-chain wallet addresses, serving over 200 projects including Starknet, ZetaChain, and Notcoin. The TON ecosystem alone made TokenTable its primary distribution infrastructure, helping onboard 20 million new wallet addresses within three months — the most successful mass crypto onboarding event in history. Sign generated $15 million in annual revenue in 2024 almost entirely from this engine. That is not a pilot. That is a working, revenue-generating, scaling distribution business that operates independent of any government contract and produces real income regardless of where Sign's sovereign ambitions sit on the deployment timeline. Most infrastructure protocols would consider that their entire company. For Sign, it is half of it.

Sign's B2G engine is the one the crypto market has not yet priced. The S.I.G.N. framework — Sovereign Infrastructure for Global Nations — is Sign's technical architecture for deploying its stack inside national systems. The Kyrgyz Republic's Digital SOM CBDC sits inside this framework, with Sign holding a live technical service agreement with the National Bank and the currency already carrying legal status ahead of a full issuance decision at end of 2026. Sierra Leone's national blockchain-based digital identity system sits inside this framework, with Sign holding an MOU with the Ministry of Communication, Technology, and Innovation. The UAE and Thailand are active deployments. Over 20 countries are in the expansion pipeline. Government budgets do not depend on crypto market cycles. Once a sovereign system is adopted, switching costs are so high that the contract effectively becomes permanent revenue. Sign's B2G engine is not a speculative future. It is a signed, legally structured, sovereign-scale business that has not yet reached the revenue activation stage — but is structurally closer to that stage than any price near $0.05 reflects.

The reason both engines matter together is that they are not actually separate businesses. They share the same underlying architecture. Sign Protocol is the attestation layer that both engines run on. When TokenTable distributes tokens to 40 million wallets, Sign Protocol is creating the on-chain verification records that make each distribution auditable and tamper-proof. When the Kyrgyz Republic issues Digital SOM to its citizens, Sign Protocol is the identity verification layer that confirms each recipient before the CBDC distribution executes. TokenTable is the distribution engine in both cases. Sign Protocol is the trust layer in both cases. The B2C business and the B2G business are not two separate products sharing a brand — they are two deployment contexts for the same integrated stack. Every dollar Sign earns from crypto-native distribution makes the sovereign infrastructure pitch more credible. Every government contract Sign signs makes the TokenTable distribution engine more defensible.

The price today is $0.05145, up 9.56% on the session — Sign's strongest single-day move in the current recovery. Volume came in at 185.77 million SIGN, expanding significantly alongside the price. RSI is at 68.62, approaching but not yet at overbought territory. The EMA structure shows Sign trading well above its 20-period at $0.04743, its 50-period at $0.04552, and its 200-period at $0.03998 simultaneously, with a MACD reading of 0.00211 DIF against 0.00151 DEA — the strongest MACD configuration Sign has shown in this recovery cycle. The chart confirmed its bottom at $0.03906 and has now built three consecutive days of gains. Binance has tagged $SIGN with both "Infrastructure" and "Gainer" labels simultaneously — a combination that tells you the market is beginning to connect Sign's fundamental category with its price momentum. The chart is measuring the beginning of a rerating. It is not yet measuring the full extent of what is being rerated.

Here is the risk I would sit with honestly. Running two businesses simultaneously at Sign's current scale is a resource allocation challenge that the company has not yet publicly resolved. The B2G pipeline requires sovereign-grade engineering, regulatory navigation, government relationship management, and compliance documentation across multiple jurisdictions in parallel. The B2C pipeline requires product velocity, developer ecosystem growth, and distribution infrastructure that scales with crypto market cycles. Those two demands compete for the same team, the same engineering bandwidth, and the same leadership attention. Sign has not yet demonstrated that it can accelerate both engines simultaneously without one constraining the other. The market should watch whether Sign's government deployment cadence slows as the B2C pipeline expands, or vice versa.

The second risk is the revenue gap between the two engines. Sign's $15 million in annual revenue is real and entirely B2C in origin. The B2G engine has not yet generated proportional revenue because the sovereign deployments are in pilot and MOU stages rather than full production. The market is being asked to price a dual-engine company where one engine is running at revenue and the other is running at potential. Until the B2G engine activates at scale — meaning a CBDC goes live, a national digital ID system reaches millions of citizens, and government contracts begin generating run-rate revenue — the dual-engine thesis remains partially theoretical. Partially theoretical at $0.05 is a different risk profile than partially theoretical at $0.15. The current price reflects that distinction. The question is whether it overreflects it.

What would make me more constructive on Sign's dual-engine thesis is specific. I want to see TokenTable's $4 billion in distributions cross $10 billion — because that number is the proof that the B2C engine compounds independently of government timelines. I want to see Kyrgyzstan's Digital SOM move from pilot to full legal tender issuance, because that event activates the B2G revenue engine in a way that no MOU or technical service agreement can substitute for. And I want to see Sign publish a revenue breakdown that shows B2G revenue appearing as a distinct line — even a small one — because the moment government contracts begin generating recognizable income, the market's entire valuation framework for SIGN has to change.

Do not watch where $SIGN is trading. Watch whether Sign's next earnings announcement shows B2G revenue appearing alongside B2C revenue for the first time. That line appearing on the income statement is the signal that Sign's dual-engine thesis has moved from architecture to reality — and it is the signal the current price has not yet priced in.

$SIGN #SignDigitalSovereignInfra @SignOfficial