TL;DR

1. Executive Summary

Naoris Protocol positions itself as a Sub-Zero Layer 1 blockchain designed to provide decentralized, post-quantum cybersecurity validation beneath existing L1/L2 stacks, transforming everyday devices into incentivized "TrustNodes" via its novel dPoSec (Distributed Proof of Security) consensus and Swarm AI anomaly detection. Launched mainnet in early April 2026 after a testnet processing 106M+ post-quantum transactions and mitigating 603M threats across 1M+ nodes, Naoris targets a convergence of DePIN, Web3 security, and enterprise cyber-defense amid accelerating quantum timelines (e.g., Google's 2029 CRQC projection).https://crypto.news/naoris-launches-first-nist-approved-quantum-resistant/https://www.coindesk.com/markets/2026/04/03/naoris-protocol-s-quantum-resistance-blockchain-goes-live-as-bitcoin-and-ethereum-face-q-day-threats

Core Thesis: Naoris aims to create a "Decentralized Trust Mesh" where infrastructure (validators, wallets, bridges, DeFi) continuously attests integrity using NIST-approved Dilithium-5 signatures, addressing "harvest now, decrypt later" risks without requiring chain forks or wallet migrations. Backed by $14.5M funding (Draper Associates, Mason Labs) and cited in a 2025 SEC submission as the PQFIF reference model, it has partnerships spanning AI (Cluster Protocol), RWA (Mova Chain, 400M NAORIS bridged), and industrial DePIN (Level One Robotics).https://thequantuminsider.com/2025/10/08/independent-sec-submission-cites-naoris-protocol-as-reference-model-for-quantum-safe-blockchain-infrastructure/

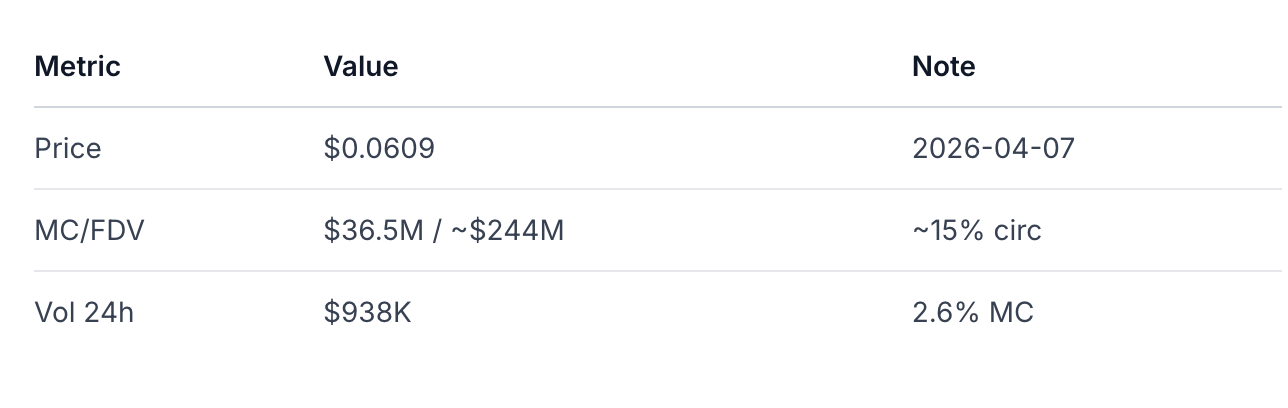

Current Snapshot (2026-04-07 UTC): NAORIS trades at $0.0609 (MC $36.5M, FDV ~$244M assuming 4B total supply), with 24h vol $938K (-0.5%). Highly concentrated (top 2 wallets ~76%), #7 Security mindshare, $37M derivs OI (neutral funding 0.36%). Testnet validates ambition, but invite-only mainnet yields no public TVL/fee/revenue/validator data—utility remains theoretical.

Investment View: High-conviction narrative beta blending post-quantum optionality (strong: NIST-native, SEC nod) with DePIN security middleware (medium: partnerships but no production density). Durable if trust mesh bootstraps real Web3/enterprise demand; fragile if remains speculative amid concentration risks and unproven economics. Accumulate on dips below $0.055 for 3-5x upside in bull; avoid if mainnet opacity persists. Scores: 3.2/5 overall (architecture 4.5; utility 1.8).

2. Research Question and Investment Relevance

Primary Question: Does Naoris Protocol establish a durable moat as decentralized post-quantum security infrastructure (Sub-Zero Layer trust mesh), or is NAORIS primarily a high-beta proxy for cyber-defense/post-quantum narratives?

Investment Relevance: Institutions face quantum migration mandates (EU 2030 deadline, US NIST FIPS 204) and rising DePIN/Web3 attack surfaces ($3.7B 2025 hacks). Naoris offers preemptive exposure to a $7T+ digital asset + $200B cyber market, but success hinges on transitioning from testnet hype to monetized validation demand. Relevant for VCs/funds seeking 10x infrastructure (e.g., early Chainlink), hedge funds trading narrative volatility, and family offices hedging systemic cyber/quantum risks. Differentiator: Unlike PoS L1s, Naoris monetizes security proofs via dPoSec; risks mirror early oracles (utility lag).

Why Now? Mainnet (Apr 2026) + SEC citation catalyze repricing, but data gaps demand scrutiny.

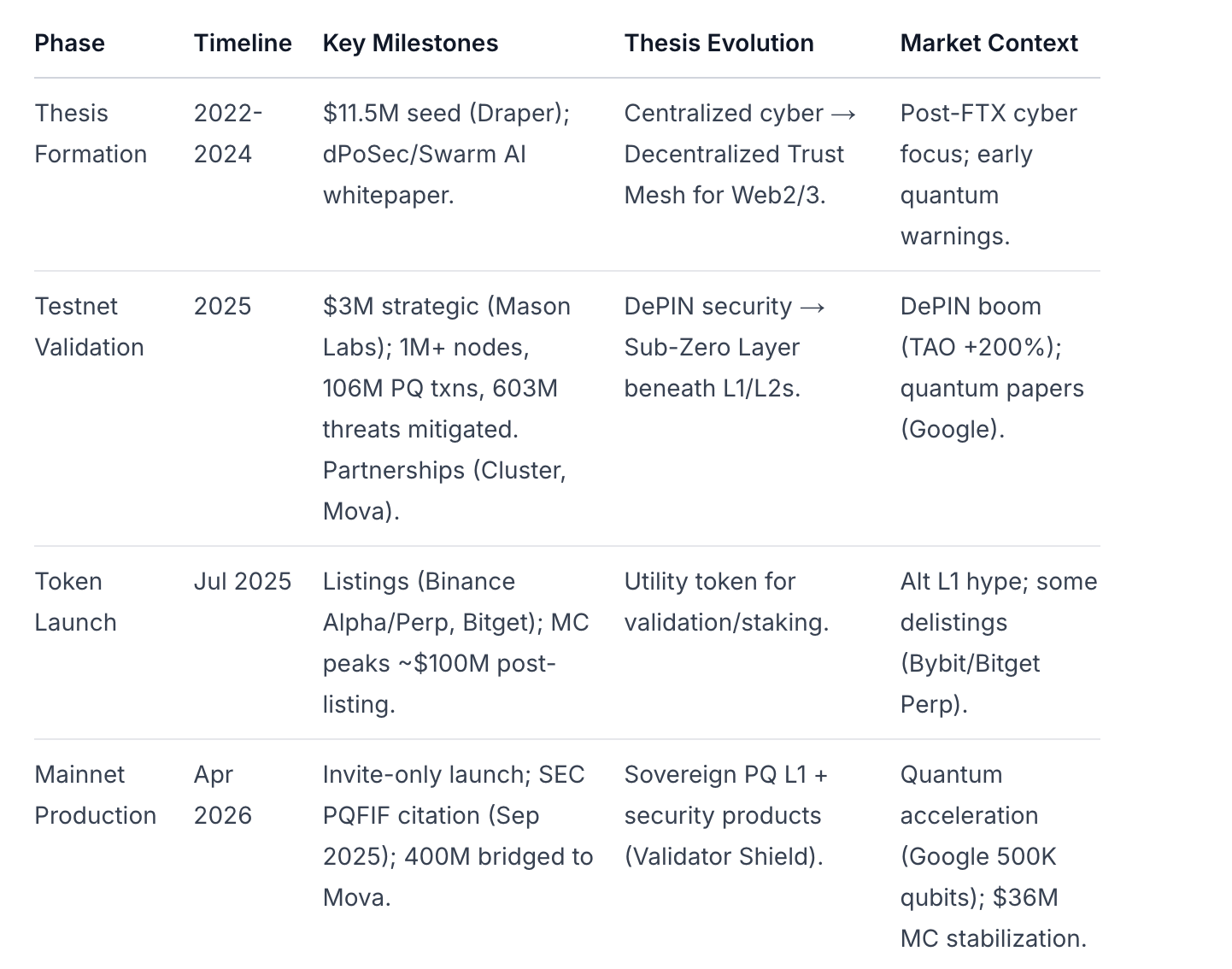

3. Historical Evolution

Naoris evolved through four phases, shifting from cyber-DePIN concept to post-quantum L1 infrastructure:

Key Insight: Identity stabilized as PQ-native security infra post-SEC nod, but mainnet opacity echoes early L1 risks (e.g., no public validators). Fact: Testnet scale proven; Inference: Production utility unverified.

4. Naoris Protocol’s Role in Crypto and Cybersecurity Market Structure

Naoris occupies a nascent "trust coordination" niche at the Web3/DePIN/cybersecurity intersection:

Crypto Structure: Sub-Zero Layer beneath L1/L2s/bridges, providing external PQ trust proofs (no forks needed). Complements oracles (Chainlink data) with infrastructure validation. DePIN-adjacent (devices as nodes) but security-focused vs compute/storage.

Cybersecurity Structure: Decentralized alternative to Chainalysis/PeckShield (analytics) or enterprise stacks (CrowdStrike), using dPoSec for real-time device attestation. Targets $200B cyber market + $7T crypto assets vulnerable to quantum ("4.5M BTC exposed").https://crypto.news/bitcoin-quantum-computing-risk-2026/

Positioning: Not a general L1 (EVM-compatible but validation-first); middleware for machine-trust in high-stakes envs (validators, CEXs, DeFi). Mindshare #7 Security (behind Chainalysis); DePIN top-20 fringe. Relevance: High for quantum tailwinds; durable if proofs become standard (e.g., via SEC PQFIF).

Fact: Invite-only mainnet limits density; Inference: Structural fit for DePIN growth (Bittensor-like) if execution holds.

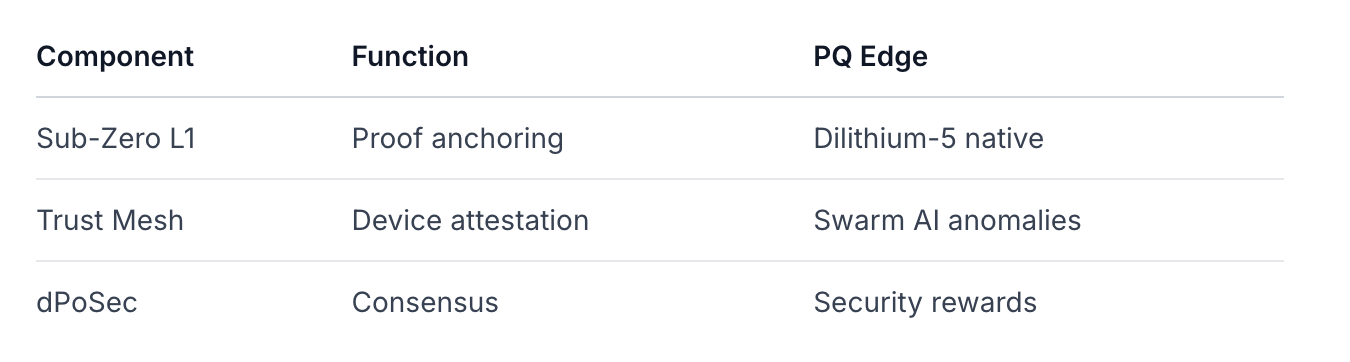

5. Architecture, Sub-Zero Layer, and Trust Mesh Design

Naoris' architecture centers on Sub-Zero Layer L1 (beneath execution layers) enforcing continuous integrity via Decentralized Trust Mesh:

Sub-Zero Layer: PQ blockchain (Dilithium-5/ML-DSA FIPS 204) anchoring trust proofs from validators/sequencers/provers. Chains consume proofs externally—no consensus changes.https://knowledgebase.naorisprotocol.com/naoris-protocol/technical-guide/how-does-naoris-protocol-work

Trust Mesh: Devices/nodes attest hardware/software state; Swarm AI detects anomalies (federated learning, no central model).

Core Flow: Node → Attest (PQ sig) → dPoSec consensus → Proof anchored → External verification.

Scalability: Testnet 1M TPS claim; EVM-compatible for dApps. Differentiation: Proactive (real-time) vs reactive cyber tools.

Strengths: Forkless PQ upgrade path; DePIN economics for global mesh. Weaknesses: Complexity risks bugs; unproven at scale (no public mainnet metrics).

Assessment: Architecturally superior to retrofits (e.g., ETH PQ hub); creates network effects if proofs standardize. Speculation: Swarm AI efficacy depends on data quality.

6. dPoSec, Validator Economics, and Security Incentives

dPoSec: Rewards anomaly detection over tx ordering; nodes stake NAORIS, attest integrity, slash on compromise. Swarm AI aggregates detections for consensus.

Validator Econ (Inferred; No Public Formulas):

Requirements: TrustNode (devices stake/run light client); hardware TBD (testnet 1M nodes).

Rewards: Emissions + fees for proofs; anti-farming via PQ attestations.

Slashing: Anomalous behavior → stake burn.

Inference: Aligns security (good detections rewarded) vs PoS (uptime). Limitation: Invite-only → no live data; risk of farming if proofs low-value.

Economics: Bootstraps via incentives; durable if enterprises demand proofs (e.g., Mova RWA). Risk: Subsidy dependency without external utility.

7. Post-Quantum Positioning and Technical Differentiation

PQ Core: NIST ML-DSA (Dilithium) for signatures; "irreversible transition" blocks classical keys post-upgrade.https://crypto.news/naoris-launches-first-nist-approved-quantum-resistant/

Differentiation:

vs Classical L1s: Native PQ (no migration pain).

vs Enterprise Cyber: Decentralized (no honeypots).

Real Today?: Mitigates classical threats (603M testnet); quantum "optionality" (Google: 500K qubits by 2029).

Thesis Strength: SEC PQFIF citation validates; EU/US mandates tailwind. Weakness: Quantum not imminent (10% ETH risk by 2032); classical utility unproven.

Fact: First NIST-approved PQ L1; Inference: Moat if proofs commoditize.

8. Token Economics and Value Capture

Supply: Circ ~600M (stable Mar-Apr); Total 4B (inferred); FDV ~$244M. Utility: Staking, governance, fees, bonding for validation.

Capture: Indirect (demand for proofs/fees); no TVL/revenue data. Concentration: Top 2 ~76% (treasuries/bridges).

Value Accrual: Weak direct (early); reflexive via node growth. Risk: Emissions dilution; unlocks unknown.

Assessment: Speculative utility; needs mainnet density for sustainability.

9. Developer Ecosystem, Integrations, and Real Utility

Ecosystem: Partnerships (Mova 400M bridge, Cluster AI, Level One Robotics); no public dApps (invite-only).

Utility: Testnet validates proofs; mainnet proofs consumable by chains. Density: Zero public metrics → theoretical.

Dev Readiness: EVM; docs sparse. Inference: Partnerships signal enterprise pivot; lacks Web3 density (e.g., no DEX TVL).

Limitation: No GitHub/activity data; pre-production.

10. Competitive Landscape

Moat: PQ + dPoSec niche; Threat: Centralized incumbents cheaper short-term.

11. Valuation and Importance Framework

Framework:

Structural (20%): PQ arch (high premium).

Narrative (50%): Quantum/cyber beta ($36M MC undervalues optionality?).

Utility (15%): Proof demand discount (low).

Risk Adj (15%): Concentration/execution (-30%).

Fair Value: $50-80M MC base (2-3x); narrative stretch to $150M bull.

Systemic: Medium (niche infra).

12. Catalysts

Public validator data (Q2 2026).

Major integration (e.g., L2 proofs).

Quantum event (Google qubit milestone).

Unlock clarity/partners revenue.

13. Risks

Execution: Invite-only opacity → rug fears.

Concentration: 76% top holders → dump risk.

Utility Lag: No fees → incentive farming.

Competition: Centralized cyber cheaper.

Quantum Hype: Narrative fade if delayed.

Regulatory: MiCA whitepaper compliant, but SEC scrutiny.

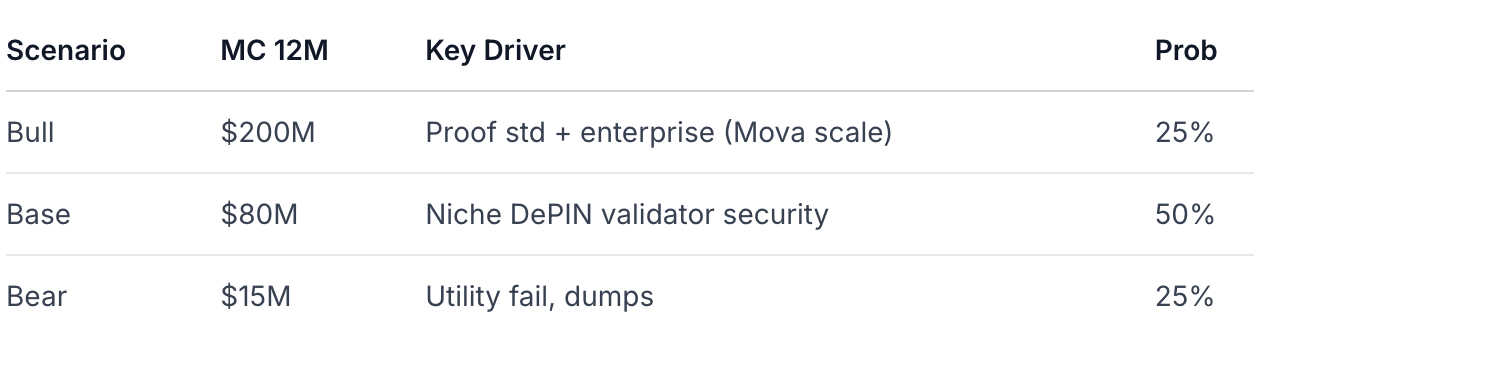

14. Bull / Base / Bear

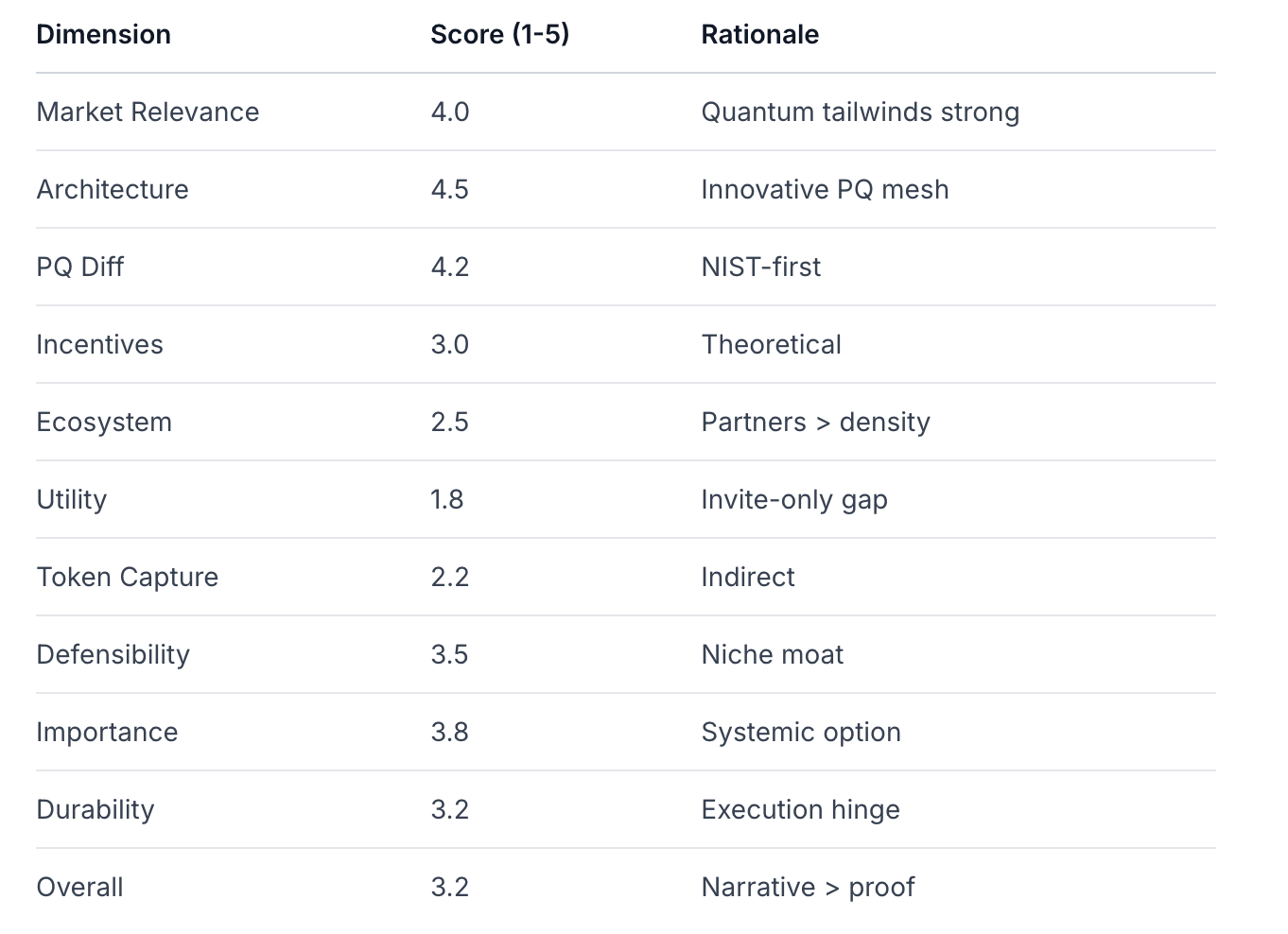

15. Scoring Matrix

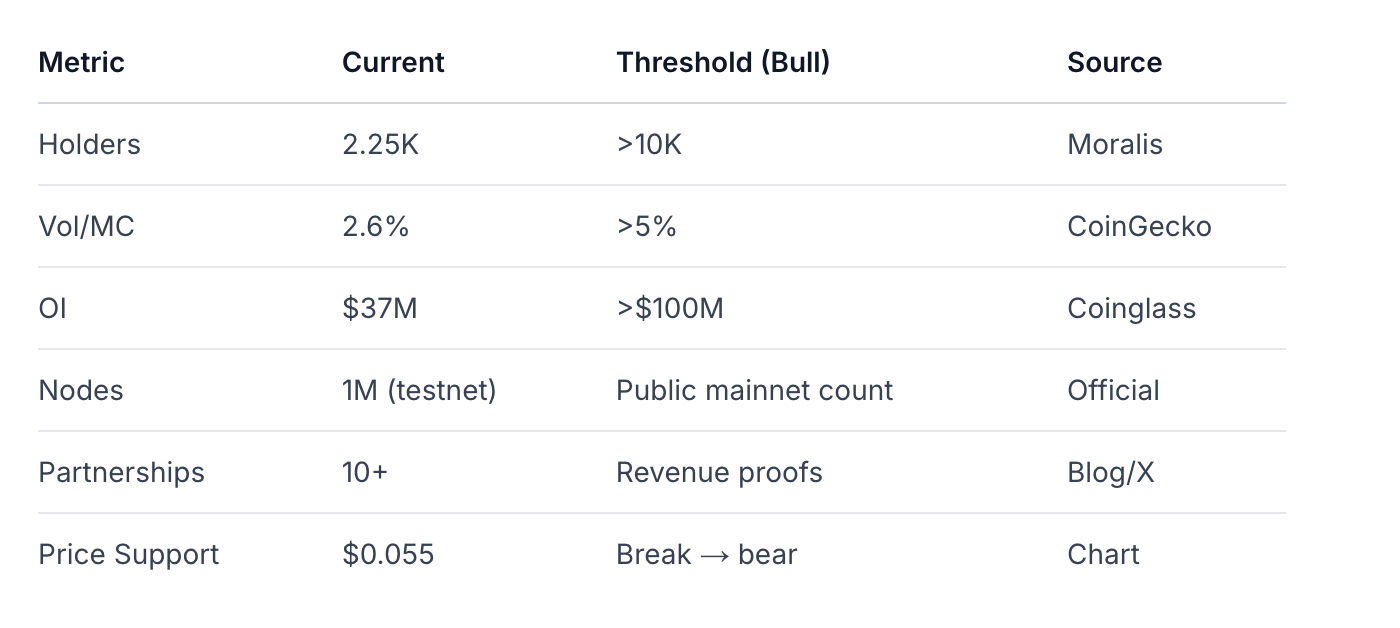

16. Monitoring Dashboard

17. Final Investment View

Why Important? Naoris pioneers PQ DePIN security, solving immutable chain vulnerabilities via external trust proofs—critical as quantum nears.

Durable? Medium: Arch strong, but needs utility transition.

Stronger/Weaker? Beats retrofits (forkless); weaker vs scaled cyber (no density).

Thesis Strengtheners: Mainnet metrics, integrations.

Breakers: Opacity, dumps, narrative fade.

Best View: Reflexive cyber/PQ narrative asset (80% narrative, 20% infra). Overweight 2-5% for thematic; monitor unlocks/nodes. Rating: Spec Buy.

Reasoning: Data shows ambition validated by testnet/SEC/partners, but gaps (utility, econ) cap conviction. Narrative drives 3x potential; structure supports 10x if proofs standardize.

read more: https://kkdemian.com/blog/naoris-protocol-naoris-post-quantum-sub-zero-layer-security-infrastructure