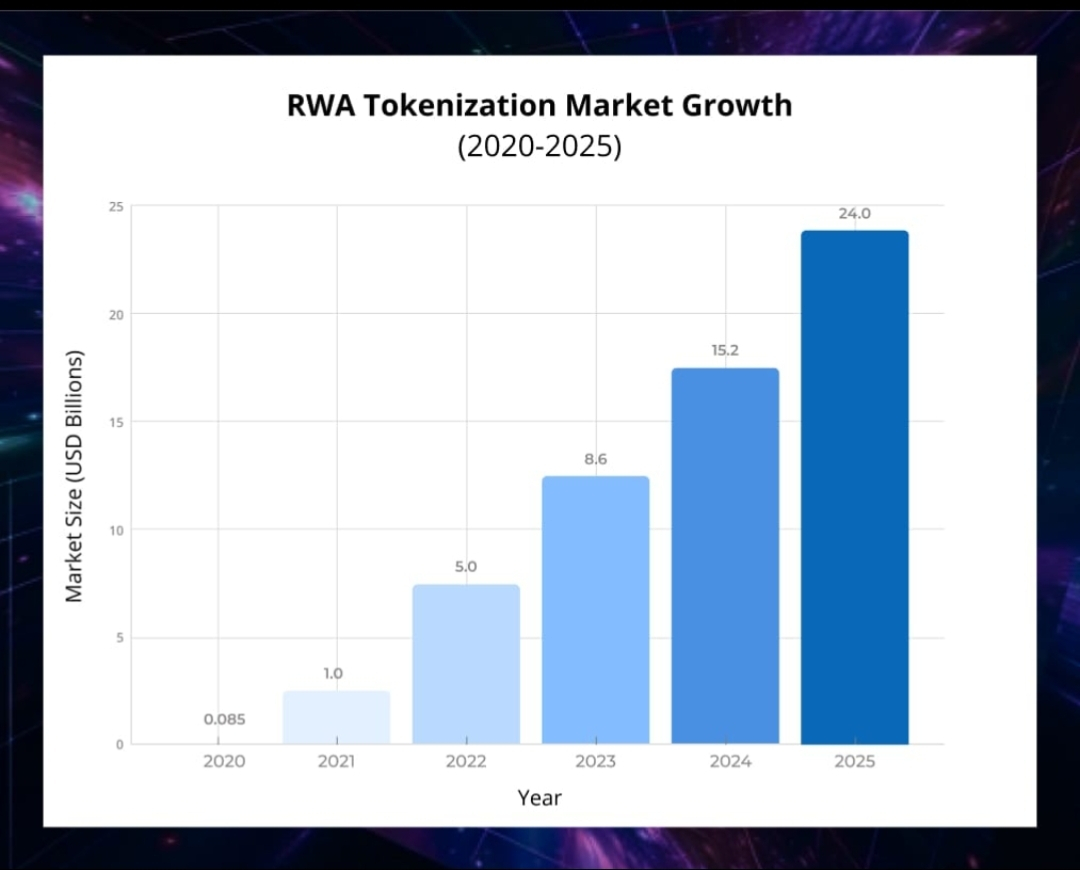

I've been tracking the RWA narrative for a while, and the latest numbers are the kind of inflection point that's hard to ignore. The tokenized real-world asset market expanded from around $5.8B in January 2025 to over $30.2B by late April 2026, per RWA.xyz. That's a 420%+ jump in roughly 16 months, and it's not driven by speculation. It's institutional plumbing being built in real time.

Tokenized US Treasuries are leading the charge, growing from $3.9B to over $15B and now anchoring the entire sector. CoinGecko's RWA Report 2026 puts Treasuries at 67.2% of on-chain RWA market cap by end of Q1, which is actually down from 73.7% at the start of 2025. That dilution is bullish, not bearish. It means other asset classes are finally getting traction instead of Treasuries carrying all the weight.

The gold story is where it gets interesting for me. Tokenized gold spot trading volume hit $90.7B in Q1 2026 alone, already past the $84.6B traded across all of 2025. Within the commodities segment specifically, PAXG and XAUT together drove 89.1% of the expansion, with PAXG growing its share from 36.8% to 41.8% during the period. That's a quarter where gold-backed tokens basically got a year's worth of activity compressed into three months, fueled by the gold rally and broader CEX accessibility.

Here's what I think actually matters for trading logic. The Treasury concentration breaking is a real signal. When the dominant asset class share drops while absolute numbers keep growing, you're watching genuine diversification of demand rather than a single-product story. Tokenized commodities went from $1.43B to $5.55B in fifteen months. ETFs and equities have emerged from near-zero. That's a maturing market structure.

MiCA in Europe is doing what regulatory clarity always does, which is unlock institutional capital that was previously sidelined. Compliant on-chain yield is now a real product category, not just a thesis. BlackRock's BUIDL, Ondo's USYC, Franklin Templeton's BENJI, and WisdomTree's WTGXX all crossed major thresholds this quarter. These aren't crypto-native projects pivoting to RWAs. They're TradFi giants moving infrastructure on-chain, which is a different kind of liquidity than past cycles.

The RWA perpetuals story is one I think is underappreciated. The segment quietly did $524.8B in volume in Q1 2026. Full year 2025 was $313B. Daily open interest went from $0.14B at the start of 2025 to $6.68B by end of Q1 2026. That's derivatives growth following real spot demand, which is usually a healthier setup than the other way around.

What I'm watching from here. If Treasury share keeps slipping below 65% while absolute growth holds, that confirms the sector is past its Treasury-dominant phase. If gold-backed token volume sustains above $25-30B monthly, the commodity rotation thesis has legs. And if MiCA-compliant products keep landing on more centralized European exchanges, retail flow through regulated channels could accelerate the next leg up.

The setup that gets me genuinely interested is this. RWA tokenization at ~$30B is still only 6.4% of the stablecoin market by CoinGecko's measure, up from 2.7% at the start of 2025. The relative gap is closing fast. If McKinsey's $2T forecast for 2030 is even directionally right, we're early in the structural growth phase that defines the cycle.#LearnWithFatima