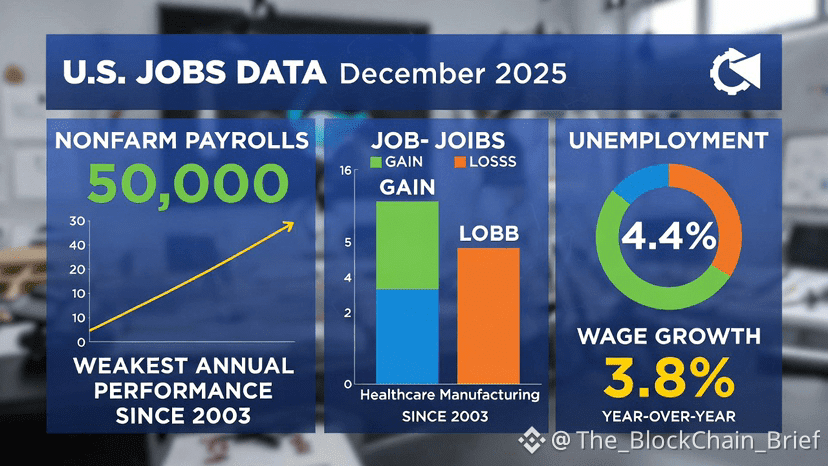

As of January 11, 2026, the latest US jobs report for December 2025, released on January 9, has solidified concerns about a cooling labor market. The Bureau of Labor Statistics (BLS) reported that nonfarm payrolls increased by a modest 50,000 jobs, below economists’ expectations of around 60,000–73,000. This capped off 2025 with total job gains of just 584,000—the weakest annual performance outside of recession years since 2003, and a sharp decline from the 2 million jobs added in 2024. #USJobsData

The unemployment rate provided a sliver of relief, dipping to 4.4% from a revised 4.5% in November, as the broader U-6 measure (including discouraged workers and those in part-time roles for economic reasons) eased to 8.4%. Average hourly earnings rose 0.3% month-over-month, pushing annual wage growth to 3.8%—outpacing inflation and offering some support to consumer spending.

Sector Breakdown and Key Drivers

Gains were heavily concentrated: Healthcare and social assistance drove much of the growth, adding around 713,000 jobs for the year—accounting for nearly all private-sector gains when combined with other resilient areas like food services. In contrast:

• Manufacturing lost 68,000 jobs in 2025, hit by tariffs and automation.

• Professional and business services shed 97,000.

• Retail trade and construction saw declines in December.

• Federal government employment dropped significantly due to staffing cuts and buyouts.

This “no hire, no fire” dynamic—characterized by hiring freezes, AI integration, and policy uncertainty—has left the market in a freeze. Excluding healthcare, private-sector growth was nearly flat, highlighting vulnerabilities in tariff-exposed and tech-adjacent sectors.

Broader Economic Context

2025’s labor slowdown was exacerbated by a prolonged federal government shutdown that disrupted data collection (notably skipping October household survey estimates) and contributed to revisions downward in prior months. Tariffs, immigration reforms, and AI adoption further restrained hiring, while demographic shifts boosted healthcare demand.

Despite the weakness, no recession signals are flashing: Layoffs remain contained (though announced cuts hit 1.2 million for the year), and consumer spending holds up amid solid wage gains.

Market and Policy Implications

The report reinforced expectations that the Federal Reserve will hold rates steady at 3.5%–3.75% in late January, with potential cuts delayed. Stocks showed mixed reactions initially but ended the week higher, buoyed by hopes for stability in 2026. Economists forecast modest improvement later in the year, potentially aided by tax provisions and rate easing, with GDP growth above 2%.

Looking ahead, the January 2026 report (due February 6) will incorporate benchmarks and cleaner data, offering a clearer picture. For now, the US jobs trend underscores resilience amid fragility—reminding investors that in a post-pandemic economy, even slow growth can avert deeper downturns.