When Plasma opened an office in Amsterdam and acquired a Virtual Asset Service Provider license in Italy during October 2025, most observers saw it as a routine regulatory compliance move. They missed the broader strategic insight. The Amsterdam expansion wasn’t about checking boxes or satisfying lawyers. It revealed Plasma’s actual long-term ambition: building a complete regulated financial infrastructure stack that could compete with traditional payment processors on their own terms, not just creating another blockchain for crypto enthusiasts to speculate on.

This licensing strategy matters because it addresses the fundamental problem that’s plagued every previous attempt to bring stablecoins mainstream. You can build the most elegant blockchain architecture in the world, achieve thousands of transactions per second, and offer zero-fee transfers, but if you can’t legally issue cards, hold customer funds under regulatory safeguards, or operate compliant on-and-off ramps without depending on third parties, you’re still just infrastructure waiting for someone else to deliver the last mile to actual users. Plasma’s founders understood this from the beginning, which is why their story is less about revolutionary blockchain technology and more about methodically assembling the boring pieces that actually make global payment systems work.

The Uncomfortable Truths Behind the Vision

Paul Faecks spent years in the stablecoin world before founding Plasma, and what he observed wasn’t particularly glamorous. He watched hundreds of millions of people use USDT and USDC not because they found cryptocurrency philosophically appealing, but because they had no better options for accessing dollars. Turkish merchants converting lira to preserve purchasing power. Venezuelan families receiving remittances from abroad. Dubai traders settling cross-border transactions. Filipino workers sending money home. These users didn’t care about decentralization or blockchain technology. They needed reliable dollar access and existing systems failed them with high fees, slow settlement, and limited availability.

The infrastructure serving these users was cobbled together from incompatible pieces. They’d acquire stablecoins through centralized exchanges that required extensive verification. They’d hold them in generic crypto wallets designed for traders, not everyday users. They’d convert to local currency through informal cash networks with inconsistent rates and availability. They’d pay merchants by manually copying addresses and hoping they didn’t make mistakes. The experience was terrible, yet it still beat traditional banking alternatives sufficiently that adoption continued growing despite the friction.

This created a peculiar market dynamic where the infrastructure had obvious problems that everyone complained about but nobody seemed positioned to fix comprehensively. Blockchains like Ethereum and Tron enabled stablecoin transfers, but they weren’t designed specifically for that purpose, so they carried unnecessary complexity and costs. Wallets provided custody but lacked integrated spending options. Payment processors offered cards but required conversions that added fees and delays. Nobody controlled enough of the stack to optimize the full user experience end-to-end. The fragmentation was economically rational for each individual company but created massive inefficiency systemically.

Faecks recognized that solving this required vertical integration on an unprecedented scale for blockchain projects. Most crypto companies focus on one layer - building a chain, creating a wallet, or offering financial services - and rely on ecosystem partners for everything else. This creates coordination problems where improvements require convincing multiple independent companies to adopt compatible standards and interfaces. Progress happens slowly if at all because everyone has different incentives and priorities. The alternative was building everything yourself, which seemed impossibly ambitious but might be the only way to actually deliver the seamless experience users needed.

The Technical Foundation That Everyone Expected

When Plasma announced it was building a Layer 1 blockchain optimized specifically for stablecoin transfers, the crypto industry responded with predictable enthusiasm followed by predictable skepticism. The enthusiasm came from recognizing that existing general-purpose blockchains did handle stablecoins inefficiently. The skepticism came from having seen dozens of specialized chains promise superior performance and fail to gain traction against established platforms.

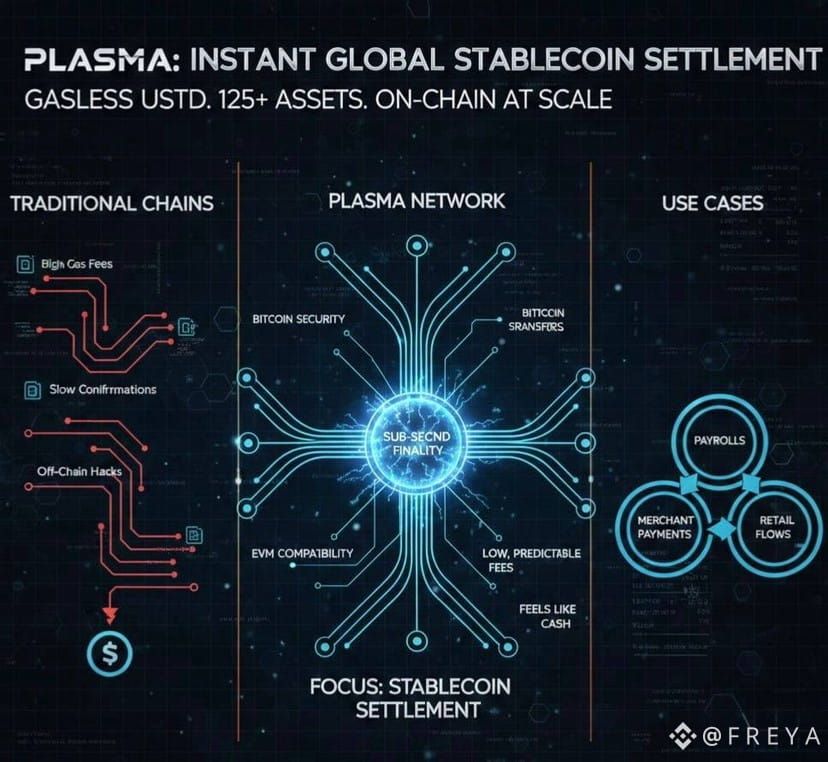

The technical architecture Plasma built incorporated the expected optimizations. PlasmaBFT consensus delivered sub-second finality necessary for payment applications where delays frustrate users. The Reth execution layer provided Ethereum compatibility so developers could deploy existing contracts without rewriting everything. The protocol-level paymaster system enabled gasless USDT transfers so users didn’t need to acquire and manage a separate token just to pay transaction fees. These weren’t revolutionary innovations individually, but together they created infrastructure that worked significantly better for stablecoin payments than general platforms.

The more interesting technical choice was the Bitcoin anchoring mechanism where Plasma periodically commits state to the Bitcoin blockchain. This wasn’t about achieving Bitcoin’s security level directly, which would be technically questionable given the different consensus models. It was about providing an additional verification layer that institutional users could reference and about signaling seriousness through association with the most established blockchain. Whether this actually mattered for security became less important than whether it reassured compliance officers and risk managers at traditional financial institutions who understood Bitcoin better than newer platforms.

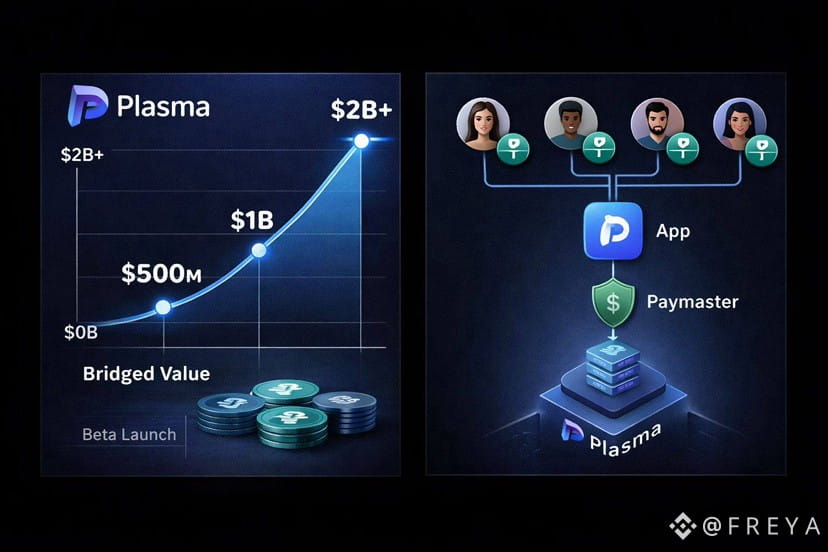

The February deposit campaign provided early validation that demand existed beyond just speculation. When the program raised one billion dollars in ninety seconds, it demonstrated that substantial capital was willing to commit to Plasma before the network even existed. The participants weren’t necessarily believers in the technology specifically. They were people who used stablecoins regularly and recognized that better infrastructure would be valuable. The instant oversubscription suggested the market was ready for someone to build what Plasma promised.

The July public token sale reinforced this demand signal by raising 373 million dollars against a 50 million dollar target. The seven-times oversubscription again showed appetite exceeding expectations. But it also created complications because such extraordinary demand meant disappointment for participants who couldn’t get allocations and created unrealistic expectations about post-launch performance. When something raises seven times its target, people naturally assume it must be exceptional in ways that justify the enthusiasm. The pressure to deliver on those implicit promises would shape everything that followed.

The September Launch and Reality Check

Mainnet launch on September twenty-fifth started with the impressive metrics crypto projects dream about. Two billion dollars in committed liquidity. Over one hundred DeFi partners deploying simultaneously. Integrations with major protocols like Aave, Ethena, Fluid, and Euler. The XPL token generating immediate trading volume and attention. Within days, stablecoin supply on Plasma approached levels that took other chains years to achieve. The launch appeared to validate everything Plasma had promised about market demand for dedicated stablecoin infrastructure.

The token price behavior told a more complicated story. XPL debuted with significant enthusiasm, reaching prices that valued the network at multiple billions in fully diluted market capitalization. Some early participants who received allocations saw substantial paper gains. But the price couldn’t sustain those levels once trading opened broadly and reality set in about actual network usage versus speculative expectations. Within weeks, XPL had declined significantly from its peak as traders realized that infrastructure adoption happens gradually while token speculation operates on much faster cycles.

The network statistics showed the gap between launch metrics and sustainable usage. While two billion dollars in total value locked sounded impressive, much of it represented liquidity mining programs and incentivized deposits rather than organic user activity. The actual transaction volume remained modest compared to what the network could theoretically handle. Daily active addresses stayed in the thousands rather than millions. The DeFi protocols had deployed but showed limited actual usage beyond initial testing. Plasma had successfully launched infrastructure. Converting that infrastructure into genuine adoption would be different challenge entirely.

The market’s harsh judgment of the token price obscured some legitimate progress. The network operated reliably without major technical incidents. The gasless USDT transfers worked as designed. The partnerships remained committed even as speculative enthusiasm faded. The foundation existed for building something substantial. But the crypto market rewards immediate traction and punishes projects that need time to develop, creating misalignment between what Plasma needed to do and what markets wanted to see.

The Amsterdam Strategy and What It Signals

The October regulatory expansion into Europe represented a strategic pivot that many observers missed because they were focused on token prices and immediate network metrics. Opening an office in Amsterdam wasn’t about establishing a sales presence or following crypto industry trends toward Europe. It was about positioning Plasma to own the complete regulated infrastructure stack required to offer banking-like services at global scale.

The Virtual Asset Service Provider license acquired through the Italian entity provided immediate legal authority to custody digital assets and handle cryptocurrency transactions under European regulation. This mattered because it meant Plasma could offer services directly rather than depending on third-party custodians with their own requirements, fees, and limitations. The company could design the user experience without being constrained by whatever custody partners were willing to support.

The planned applications for Crypto Asset Service Provider authorization under MiCA and Electronic Money Institution licensing revealed the full scope of ambition. CASP status would allow asset exchange services - enabling users to move between stablecoins, cryptocurrencies, and fiat currencies within Plasma’s own systems. EMI licensing would permit issuing electronic money and cards, operating payment accounts, and providing money transmission services across European corridors. Together, these licenses would give Plasma the legal authority to operate like a regulated financial institution rather than just a blockchain infrastructure provider.

The Netherlands office location was equally strategic. Amsterdam serves as one of Europe’s primary payment hubs with concentration of financial technology companies, payment processors, and banking infrastructure. Being physically present there provided access to partnerships with established payment networks, banks, and financial services providers that wouldn’t take meetings with companies operating remotely from crypto-friendly jurisdictions. The compliance team appointments - chief compliance officer and money laundering reporting officer - signaled commitment to operating with institutional standards rather than crypto industry norms.

This regulatory-first approach distinguished Plasma from most blockchain projects that treat licensing as a necessary evil to tolerate rather than a strategic asset to pursue aggressively. The team understood that controlling regulated infrastructure created competitive advantages that pure technology couldn’t match. A competitor might copy Plasma’s blockchain architecture within months. They couldn’t replicate years of regulatory work, established banking relationships, and licensed entities that took time and capital to build.

Plasma One and the Distribution Problem

The Plasma One neobank announcement just before mainnet launch revealed why the regulatory infrastructure mattered so much. Building a blockchain that could process stablecoin transfers efficiently was necessary but insufficient. The actual problem was distribution - getting that infrastructure into the hands of people who needed it in a form they could actually use without needing to understand anything about blockchain technology.

Plasma One aimed to solve distribution by creating an application that looked and felt like any other banking app while running entirely on stablecoin infrastructure. Users would download the app, complete rapid onboarding, receive a virtual card within minutes, and start spending immediately. They’d earn yield on their balances automatically through DeFi opportunities on the Plasma network. They’d send money to friends instantly with zero fees. They’d spend at merchants anywhere cards were accepted. The blockchain would be completely invisible. Users would just know they had an app that worked better than their alternatives.

The product specification showed sophistication about what mainstream users actually need versus what crypto enthusiasts think they want. No seed phrases to manage, just biometric authentication that people already understand from banking apps. No manual token swaps or gas management, just balances that automatically deployed into highest available yields. No crypto addresses to copy and paste, just normal payment flows identical to existing fintech applications. The design philosophy was making blockchain irrelevant to the user experience rather than celebrating it.

The go-to-market strategy targeted emerging markets where dollar access creates genuine value rather than developed markets where stablecoins compete against already excellent banking infrastructure. Turkish users facing currency instability. Middle Eastern traders conducting cross-border commerce. Southeast Asian workers sending remittances. These segments already used stablecoins despite terrible interfaces because the value proposition was strong enough. Giving them proper infrastructure would accelerate adoption rather than having to convince people why they should care.

The four percent cash back on spending and ten percent yield on balances created economic incentives that could drive initial adoption even without perfect product-market fit. These rates would almost certainly decrease over time as promotional programs ended and yield farming opportunities normalized, but they served their purpose of attracting early users and generating word-of-mouth promotion. The challenge would be retaining those users after the exceptional economics transitioned to sustainable levels.

The Market Disconnect and Communication Challenges

The gap between Plasma’s long-term infrastructure building strategy and the crypto market’s demand for immediate results created communication challenges that the team struggled to navigate effectively. When XPL declined ninety percent from its peak through November, the natural question from token holders was what the team was doing to reverse the price decline. The honest answer - building regulatory infrastructure, refining products, and pursuing sustainable adoption - didn’t satisfy people who wanted catalysts that would move prices quickly.

The November development update highlighting technical improvements, infrastructure maturation, and operational progress landed poorly with an audience expecting announcements about major partnerships, explosive user growth, or revolutionary features that would justify higher valuations. Refactoring the codebase mattered for long-term reliability. Expanding testing infrastructure improved quality. Rebuilding peer discovery layers enhanced user experience. None of these created immediate traction that markets would reward.

The communication challenge was that building real financial infrastructure happens slowly and involves mostly unglamorous work that doesn’t generate exciting headlines. Securing regulatory licenses takes months of applications, audits, and negotiations. Developing compliant payment products requires extensive testing and iteration. Establishing banking relationships proceeds at traditional finance’s pace, not crypto’s. The team was making genuine progress on things that would matter enormously in two or three years. They struggled to articulate why that progress should matter to people focused on token prices over the next two or three weeks.

The sparse network activity became the most visible metric that critics could point to as evidence of failure. When blockchain explorers showed just a few transactions per second on a network theoretically capable of thousands, it was difficult to argue that adoption was proceeding successfully. The reality was that most infrastructure operates well below capacity initially as usage builds gradually. But crypto markets don’t reward building capacity ahead of demand. They punish projects that launch with more infrastructure than current usage requires.

The Plasma One Hypothesis Being Tested

Whether Plasma succeeds ultimately depends on whether the Plasma One application can actually drive meaningful stablecoin adoption among people who don’t currently use cryptocurrency. The team’s hypothesis is that previous attempts failed not because people don’t want stablecoin-based banking but because the infrastructure was too complicated, unreliable, and fragmented to deliver acceptable experiences. If true, then providing proper infrastructure should unlock latent demand.

The competing hypothesis is that stablecoin adoption faces fundamental barriers beyond just user experience - regulatory uncertainty, lack of merchant acceptance, volatility concerns, limited awareness, superior alternatives - that good infrastructure alone cannot overcome. Under this view, the hundreds of millions supposedly desperate for dollar access either don’t exist, already have adequate solutions, or face obstacles that technology cannot address.

The initial rollout targeting regions with existing stablecoin penetration was designed to test these hypotheses in environments favorable to the optimistic case. If Plasma One can’t gain traction in markets where people already use stablecoins despite terrible infrastructure, that would suggest the problem is more complex than infrastructure quality. If it does succeed in these markets, that validates moving into more challenging environments where stablecoin awareness is lower and alternative solutions are more competitive.

The staged rollout approach gave Plasma flexibility to iterate based on what they learned from early markets before committing to global scale. They could adjust the product based on actual user behavior rather than assumptions. They could refine the economics as they understood what yields were sustainable and what rewards were necessary. They could identify which features mattered most versus which turned out to be unnecessary complexity. The downside was that staged rollouts generated less immediate impact than big bang launches and required patience from stakeholders expecting faster results.

The Longer Timeline That Markets Don’t Want to Hear

If Plasma succeeds in becoming significant financial infrastructure, that success will measure in years, not months. Regulatory licenses take time to secure and activate fully. Banking relationships develop gradually as trust builds. User adoption compounds slowly as word spreads and experiences improve. Revenue grows incrementally as transaction volume increases. None of this happens in quarters. It happens across multiple years of sustained execution.

This timeline fundamentally conflicts with crypto market expectations where projects are expected to demonstrate traction within months or be declared failures. The industry moves so quickly that investors struggle to maintain conviction through the quiet periods where real infrastructure development happens. They’re constantly tempted to chase newer projects promising faster returns rather than supporting projects building sustainable foundations.

Plasma’s challenge is maintaining team morale, community engagement, and investor confidence through the unglamorous building phase when progress is real but not immediately visible in obvious metrics. The regulatory licenses won’t generate revenue for quarters after they’re secured. The Plasma One application will require extensive iteration before achieving product-market fit. The network effects that make payment infrastructure valuable take time to compound as more users and merchants join.

The team’s decision to focus on building properly rather than optimizing for short-term metrics was strategically correct but emotionally difficult. It meant accepting that the token price would likely remain depressed until actual adoption materialized. It meant enduring criticism from people expecting faster progress. It meant working through periods where markets questioned whether the project made sense at all. The alternative would be pursuing initiatives that generated quick attention but didn’t contribute to long-term viability.

What Success Actually Looks Like Years From Now

Success for Plasma in 2028 or 2030 looks completely different than what crypto markets typically celebrate. It’s millions of people in emerging markets using Plasma One as their primary banking app without knowing or caring that it runs on blockchain. It’s merchants accepting stablecoin payments through Plasma’s infrastructure because settlement is faster and cheaper than credit cards. It’s institutional treasurers moving corporate funds through Plasma rails because the compliance infrastructure is robust and the efficiency is superior to traditional banking.

It’s developers building payment applications on Plasma infrastructure because the regulated stack is already established and battle-tested rather than something they need to assemble themselves from fragmented pieces. It’s traditional financial institutions partnering with Plasma because the licensing and compliance framework makes integration possible under their risk requirements. It’s regulatory clarity around stablecoin operations with Plasma positioned as a model for how to operate in compliance with emerging frameworks.

The XPL token in this scenario derives value from actual network usage rather than speculation about future potential. Transaction fees from real commerce. Staking requirements for validators securing billions in transaction volume. Governance influence over infrastructure that genuinely matters to millions of users. The token becomes a functional component of financial infrastructure rather than just a speculative asset.

This vision requires everything working correctly - regulatory strategy executing as planned, products achieving product-market fit, users adopting at sufficient scale, institutional partnerships materializing, market conditions remaining favorable. Any number of things could prevent it from happening. Regulatory barriers could prove insurmountable. Competitors could execute better. User adoption could remain limited. Market dynamics could change in ways that undermine the thesis.

Reflecting on Infrastructure Versus Hype

We’re watching an experiment in whether building boring infrastructure with proper regulatory foundations can compete in an industry that typically rewards bold promises and rapid speculation cycles. Plasma chose the harder path of pursuing licenses, establishing banking relationships, and building compliant products rather than the easier path of maximizing token price through hype and hoping adoption would follow.

This choice made sense if their goal was building something that could actually serve hundreds of millions of users at global scale under regulatory frameworks that will inevitably govern digital finance. It made less sense if their goal was maximizing returns for early investors on timeframes crypto markets expect. The tension between these objectives defines most of Plasma’s challenges.

Whether this approach succeeds or fails will reveal important things about how blockchain infrastructure can actually integrate with traditional finance and whether the industry can support projects that prioritize sustainable building over speculative attention. It becomes a test case for whether crypto can mature beyond just creating new tokens and toward providing real infrastructure that competes with established systems on reliability, compliance, and user experience rather than just novelty and speculation.

The answer won’t be clear for years. Plasma has built the foundation and articulated the vision. Now they have to actually deliver the adoption, execute on the regulatory strategy, achieve the product-market fit, and sustain the operation through the difficult building phase. They’re trying to create financial infrastructure from the ground up in an industry that typically loses interest before infrastructure becomes valuable. Whether that’s possible will determine not just Plasma’s fate but also whether blockchain can actually deliver on its promise of improving how money moves globally.