Plasma is not trying to be just another blockchain. It is being built as financial infrastructure with a very specific mission: make digital dollars move as naturally and efficiently as cash, but at a truly global scale. At its core, Plasma focuses on stablecoins as money itself, not as a side feature of DeFi or speculation. This design choice shapes everything about the chain, from its consensus model to how users interact with it on day one.

Plasma’s Vision: Stablecoins as Everyday Money

For most of the world, moving money is still slow, expensive, and full of friction. Plasma approaches this problem from a distribution-first mindset. Money only works when it reaches people, merchants, and markets they already trust. Plasma is designed to connect onchain dollars directly to real-world payment flows, including peer-to-peer cash-style networks, so digital dollars don’t stay trapped inside crypto-native apps.

Instead of forcing users to adapt to complex blockchain mechanics, Plasma hides that complexity behind a system optimized for speed, security, and composability. The goal is simple: sending stablecoins should feel instant, cheap, and reliable, whether it’s for saving, paying, or settling transactions across borders.

Mainnet Beta: Utility from Day One

Plasma’s mainnet beta represents a major milestone. From the very first day, billions of dollars in stablecoins are expected to be active on the network. Rather than launching empty and hoping liquidity arrives later, Plasma begins with deep capital already deployed across a wide range of DeFi integrations. This ensures immediate utility: users can save, borrow, and move digital dollars without waiting for an ecosystem to form.

A defining feature of this phase is zero-fee stablecoin transfers through Plasma’s own products. By removing fees at the base layer for authorized transfers, Plasma makes a strong statement: stablecoins should function like digital cash, not like a premium service.

PlasmaBFT: Built for High-Volume Dollar Flows

Traditional blockchains often struggle when transaction volume spikes, especially during periods of heavy usage. Plasma introduces a high-throughput consensus layer specifically designed for stablecoin flows. This allows the network to handle large volumes of dollar-denominated transactions without congestion or unpredictable costs.

The architecture prioritizes reliability and efficiency over unnecessary complexity. For builders, this means an environment where financial applications can scale without worrying about sudden fee spikes or settlement delays. For users, it means trust: money moves when it’s supposed to move.

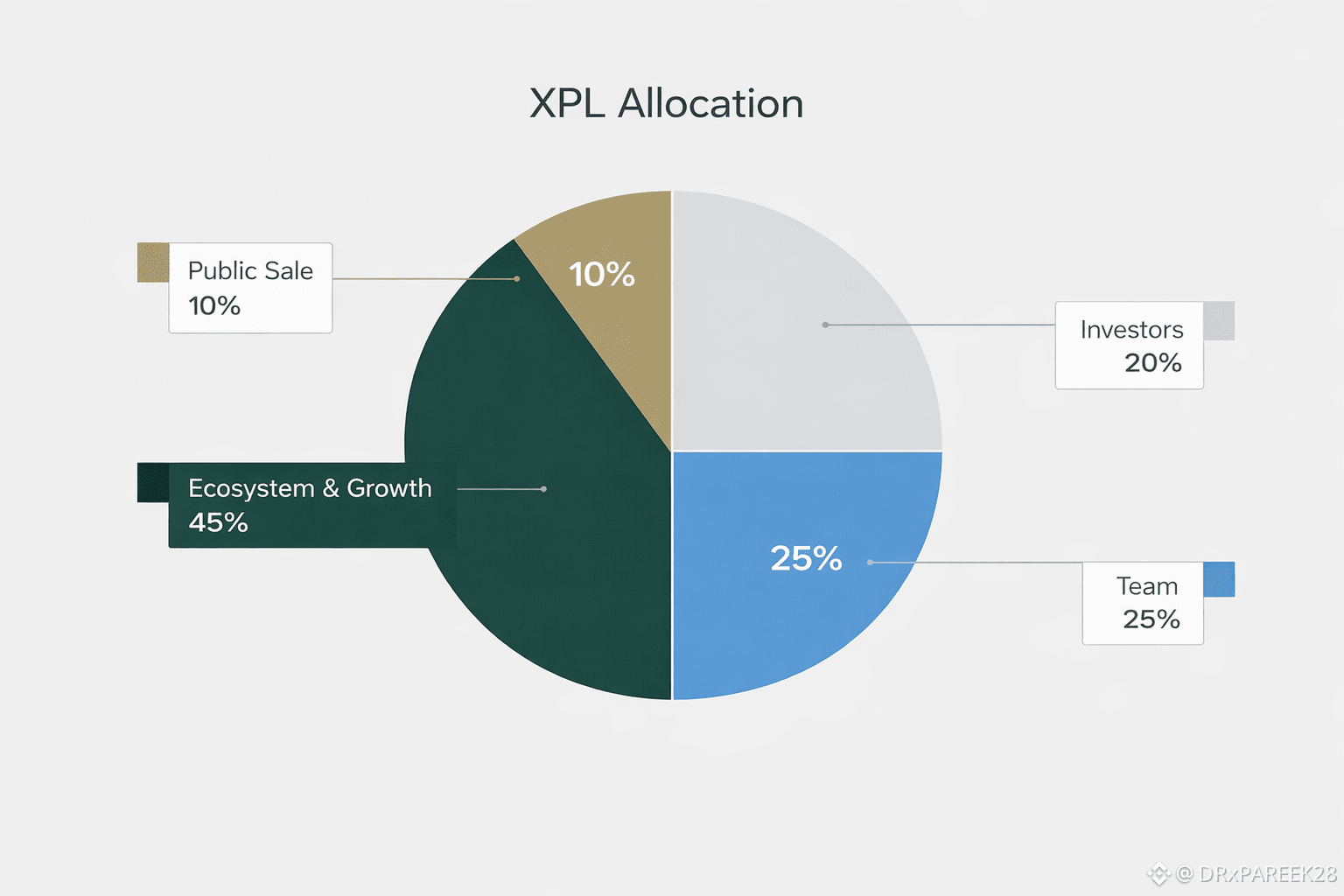

Ownership and Alignment Through XPL

Plasma’s native token, XPL, plays a critical role in securing the network and aligning incentives. Rather than concentrating ownership, Plasma emphasizes broad distribution. Community members, early participants, and contributors are recognized through structured allocations, ensuring that the people who use and build the system also have a stake in its future.

XPL secures the network, incentivizes validators, and represents ownership in the underlying financial rails Plasma is creating. This approach reinforces the idea that global money infrastructure should not be controlled by a narrow group, but shared among those who rely on it.

A Trillion-Dollar Opportunity

Stablecoins are already changing how people preserve value, send remittances, and run businesses, especially in emerging markets. Plasma is positioning itself as the foundation that turns stablecoins into true everyday money. By combining deep liquidity, zero-fee transfers, regulatory alignment, and real-world distribution, Plasma aims to bridge the gap between onchain dollars and daily life.

This is not about short-term hype. It’s about building durable financial rails that can support payments, foreign exchange, savings, and commerce for millions, and eventually billions, of people. Stablecoins are Money 2.0, and Plasma is the system designed to carry them everywhere.