By the end of 2025, public companies built massive ETH treasury positions most traders barely noticed.

According to Everstake:

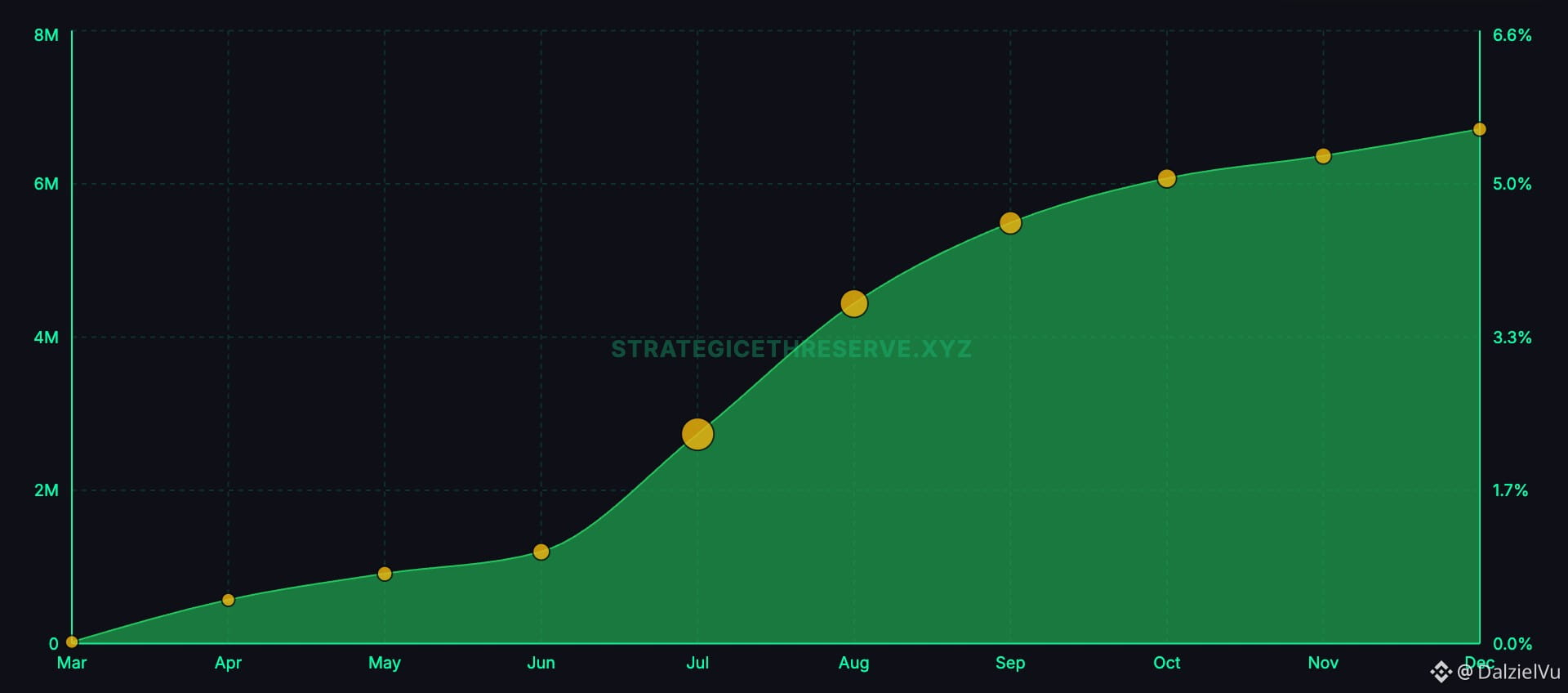

🔹 6.5–7M ETH held by public firms

🔹 ≈ 5.5% of circulating supply

🔹 36M+ ETH staked (29% of supply)

🔹 Staking yield ≈ 3% APY

This is no longer retail institutions are stacking ETH at scale.

Why companies prefer $ETH (not just $BTC)

Bitcoin = scarcity

Ethereum = yield + scarcity

After buying $ETH ,companies can:

✅ Stake

✅ Earn protocol rewards

✅ Grow ETH holdings over time

👉 Basically: ETH that pays yield

So their strategy becomes:

Raise capital

Buy ETH

Stake

Compound rewards

More ETH per share = higher valuation.

Who’s leading?

🏢 BitMine → ~4M ETH

🏢 SharpLink → ~860K ETH

🏢 The Ether Machine → ~496K ETH (100% staked)

These aren’t experiments anymore this is institutional scale accumulation.

Big picture

ETH is turning into:

Staking yield asset

Stablecoin backbone

Tokenized Treasury infrastructure

👉 Institutions aren’t just speculating

👉 They’re treating ETH like productive capital

Risks to watch

⚠️ Validator failures / slashing

⚠️ Stock premium disappears

⚠️ Regulatory pressure

If capital markets slow → the flywheel breaks.

Bottom line:

Companies are quietly buying + staking millions of ETH.

Supply keeps locking. Yield keeps compounding.

Long-term bullish… if the system holds.

Would you treat $ETH as a yield asset or just price speculation? 👇