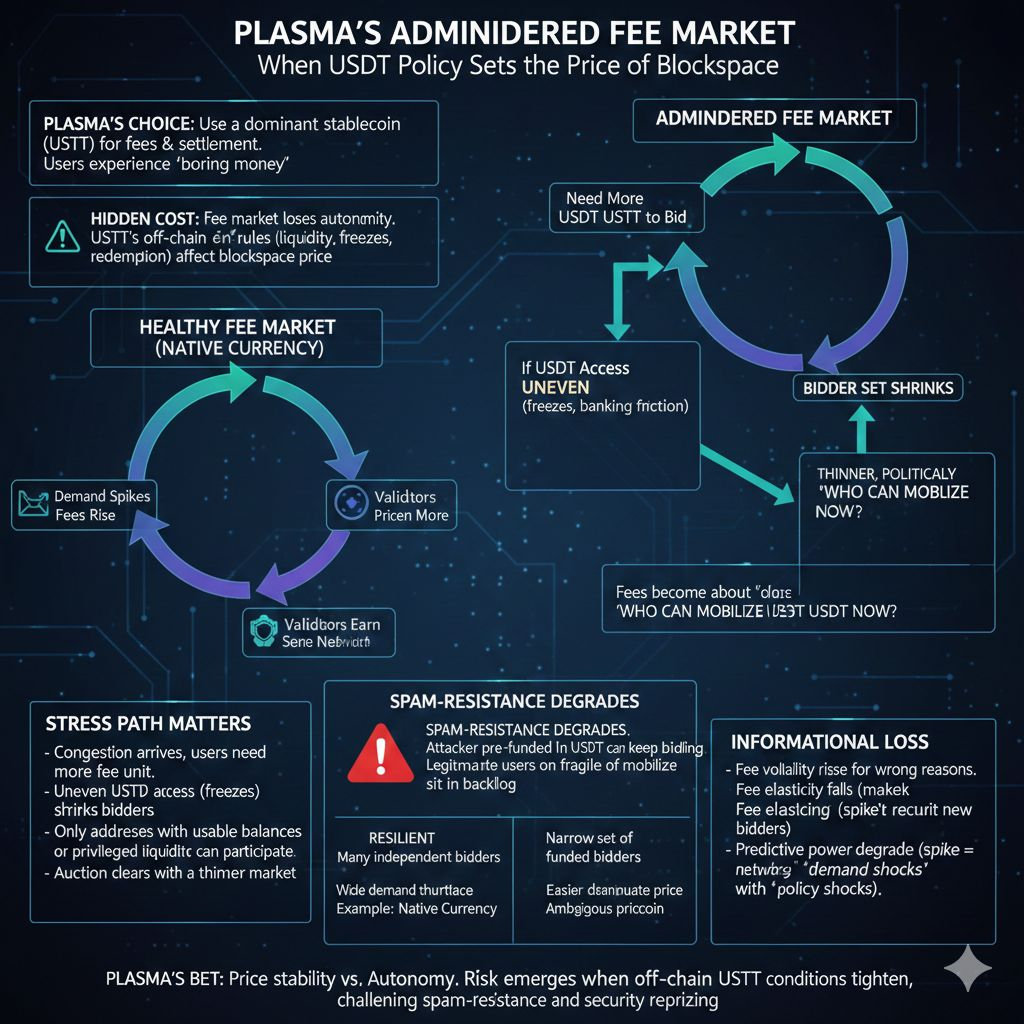

Plasma is making a deliberate choice: let a dominant stablecoin become the unit you pay fees in and the unit you settle in, so users experience “boring money” even when crypto markets aren’t boring. The hidden cost is that the chain’s fee market stops being purely endogenous. Once gas and settlement share the same stablecoin denominator, the issuer’s off-chain rules around liquidity, freezes, and redemption seep into the one signal a chain relies on when things get crowded: what it costs to buy blockspace right now.

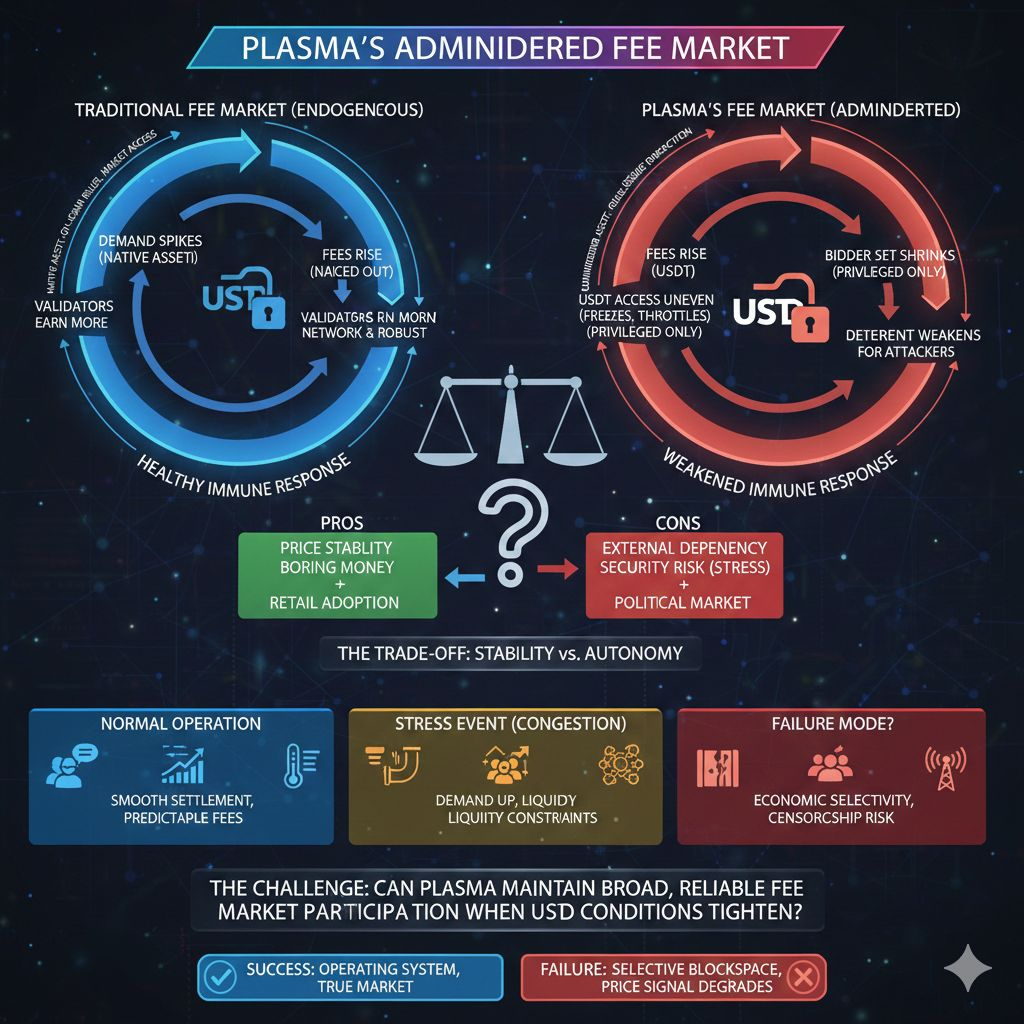

A healthy fee market is an immune response. Demand spikes, fees rise, spam gets priced out, and validators earn more to secure a busier network. That loop degrades when the bidding currency is externally administered, meaning its usability can be constrained without any vote of consensus. By “native” here I mean an asset whose availability and transferability are governed primarily by on-chain rules and market access, not by an issuer’s discretionary freeze policy or by the operational state of redemption rails. Plasma’s stablecoin-first design trades away some of that autonomy in exchange for pricing stability, and that trade becomes visible only when the network is stressed.

Here is the stress path that matters. Congestion arrives and users need more of the fee unit to outbid others. If the stablecoin’s access becomes uneven, whether due to freezes, redemption throttles, banking-rail friction, or regional compliance constraints, the bidder set shrinks in a specific way: only addresses already holding usable balances, or actors with privileged liquidity and routing, can keep participating at the margin. The auction can still clear blocks, but it clears with a thinner, more politically shaped market. Fees become less about “how much does the world want this blockspace” and more about “which subset of the world can still mobilize the fee currency right now.”

That distinction is not cosmetic. Spam-resistance depends on the network being able to raise the price of abuse broadly, not just raise it for the people who are already locked out. When the fee unit is hard to source for a large slice of users, you can get a perverse outcome where gas prices spike while the effective deterrent weakens for the attacker class you care about. An attacker who is pre-funded in the fee stablecoin, or who has stablecoin liquidity through compliant routes, can keep bidding. Meanwhile legitimate users who rely on topping up through fragile rails sit in a backlog. The chain is “pricing congestion,” but the pricing is not universally actionable, so it doesn’t function as a clean throttle.

This is where the security budget angle stops being abstract. Validators get paid in the same stablecoin unit, but the robustness of that revenue under stress depends on participation breadth. A fee market with many independent bidders is resilient because the network can discover price through a wide demand surface. A fee market that collapses into a narrow set of funded or privileged bidders is brittle because it becomes easier to manipulate and harder to interpret. In a thin auction, the same nominal fee level can reflect very different realities: genuine global demand, or a liquidity choke where only a few entities can transact at any price. Plasma’s design makes that ambiguity more likely during the exact moments when fee clarity is most valuable.

The informational loss shows up in the properties of the signal, not just the number on the screen. Under issuer-layer friction, fee volatility can rise for the wrong reason, and fee elasticity can fall because the market can’t recruit new bidders by offering higher prices. Predictive power degrades too: a spike might normally imply “the network is popular,” but here it can also mean “the fee unit became temporarily harder to mobilize.” When the unit-of-account is administered, the chain’s telemetry starts mixing demand shocks with policy shocks, and the chain has fewer levers to separate them.

Gasless transfers don’t escape this dependency; they concentrate it. Sponsorship means someone warehouses the fee unit and decides when to spend it on behalf of users. During congestion, sponsors face constraints that force rationing behavior: inventory limits, cost uncertainty, compliance exposure, and the practical need to avoid being the universal liquidity provider for a queue that won’t clear cleanly. That pushes sponsors toward tighter eligibility rules, higher internal thresholds, or selective service, not because they want to gatekeep, but because they are absorbing the fee volatility and the issuer-policy risk in one balance sheet. The result is that access to blockspace can collapse into sponsor policy precisely when organic access is already impaired by stablecoin mobility constraints.

It is tempting to wave this away by pointing to strong consensus and external security design. Bitcoin-anchored security can meaningfully raise the cost of certain history-rewrite games and strengthen assurances about state ordering, but it does not neutralize the fee unit. Anchoring can protect what happened; it can’t guarantee who gets to make something happen during a liquidity or freeze event. Plasma can be robust against chain-level adversaries while still being economically fragile at the issuer boundary, because the fee-market boundary and the consensus boundary are different surfaces.

The honest framing, then, is that Plasma is not just optimizing stablecoin settlement; it is accepting an administered unit-of-account for blockspace. That can be a rational bet for payments and high-adoption retail markets where users care more about predictable denominations than about maximal endogenous fee discovery. But it changes the risk model. The question becomes whether Plasma can preserve broad, reliable participation in the fee market when the stablecoin’s off-chain conditions tighten, because that is when spam-resistance and the security budget must reprice quickly and cleanly.

If Plasma gets it right, it will feel like a chain where stablecoin settlement is not a wrapper but the operating system, and the fee market still behaves like a market under stress. If it gets it wrong, the failure mode won’t look like an outage; it will look like a live network whose blockspace becomes economically selective at the worst time, because the price of blockspace is being discovered in a currency that can be partially switched off.