The concept of stablecoins is very effective, but that generates a reputation issue: transactions are immediate and irreversible. Merchants are fond of it since it removes chargebacks, yet common consumers also ask themselves: what happens in case something goes wrong?

In the case of card payments, individuals are interested in protection, and not settlement. They are aware that they can challenge an account and that a bank can undo the charge, and that there is customer service services, even though it is usually slow or annoying.

Stablecoins eliminate that intermediary, and therefore, nobody to compel the turnaround. What comes out is the low cost clean transactions and also the disappearance of the familiar undo button many users have become used to.

Thus, it is not speed or fees but trust that is the key obstacle to the adoption of stablecoins. The typical factor of trust in payment systems is simply the issue of refunds.

The hypothesis: the stablecoins will become mainstream when final payments do not feel unfair.

In case the everyday money is to be substituted with stablecoins, users must get the daily safeguards that they are used to. This does not imply the duplication of chargebacks. Chargebacks are clunky, contribute to fraud, harm merchants, foster abuse, and accrue billions of fees and operation inconvenience.

However, not paying attention to the problem of refund is no longer an option either. When the payment of the stablecoins cannot be refunded regardless, many consumers will never be comfortable to use the coins to make real purchases.

The chance is to create a system in which deals are done but reasonably, without returning to the nightmare of chargebacks.

Plasma is applicable since it is constructed on the foundations of stablecoins, thus it inherently pays attention to consumer-grade payment behaviour - not simply the movements of money but also what comes after it.

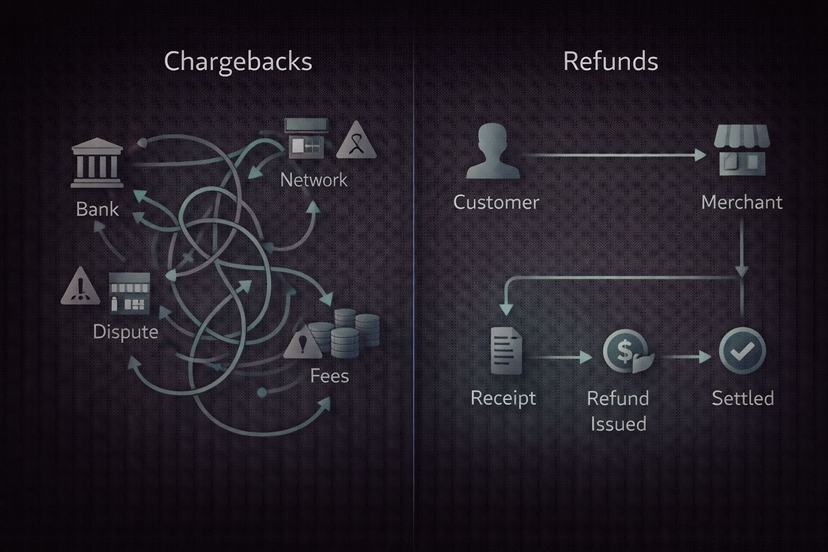

The reason why chargebacks are the nightmare of the merchant and the safety net of a consumer.

It is important to consider both substances in order to comprehend the effect.

To consumers, the chargebacks give them a feeling of safety. On a situation where an item is not delivered they are able to argue with it and the bank may take back the payment. It is not perfect, but it makes one feel safe again.

In the case of merchants however, chargebacks are usually a source of chaos. They generate unforeseen losses, may be misused, tie up money, make merchants demonstrate their innocence, introduce additional charges, and even result in the extension of a ban on the account in case of too many disagreements.

This will appeal to merchants to use stablecoins. A reversal cannot be forced by any outside body with regard to stablecoin payments. That eliminates a substantial source of fraud, minimizes the uncertainty, and allows merchants to operate in a less corrupt manner upon settlement.

But finality is in itself not enough. In case the consumers do not have a sense of protection, they will be reluctant to pay.

The most effective value proposition that plasma can make to merchants and consumers is that stablecoins are not final, but they can be final without being unfair.

The difference between refunds and chargebacks lies in the difference between the two.

A chargeback is an involuntary reversal that is initiated by a bank and a refund is an involuntary correction that is initiated by the merchant. That distinction matters.

Refunds when properly organized, keep merchants under control. To the consumer, refunds will be optimum where they are transparent, quick, and legal.

The Stablecoin payments are inherently compatible with the refund model. The missing element is a refund logic that can be easily provided by merchants and easily consumed by the consumer.

Here programmable money ceases to be a buzz word and becomes a tool. Each payment in a stablecoin may include so-called rules in the funds, specifying the refund timeframes, partial refunds, cancelation processes, and dispute routes.

This is not a science fiction concept, but a real-world method to use stablecoin payments as something normal in common business.

The actual design problem: How to put protections on without a new bank middle man?

When you introduce refund guarantees through payment reversals to a centralized company, you are more or less re-creating the old system. The user can be safe, but you have forfeited the benefit of stablecoins in the first place, which is neutral settlement.

The design dilemma would therefore be to introduce protective measures without becoming custodial and transparent.

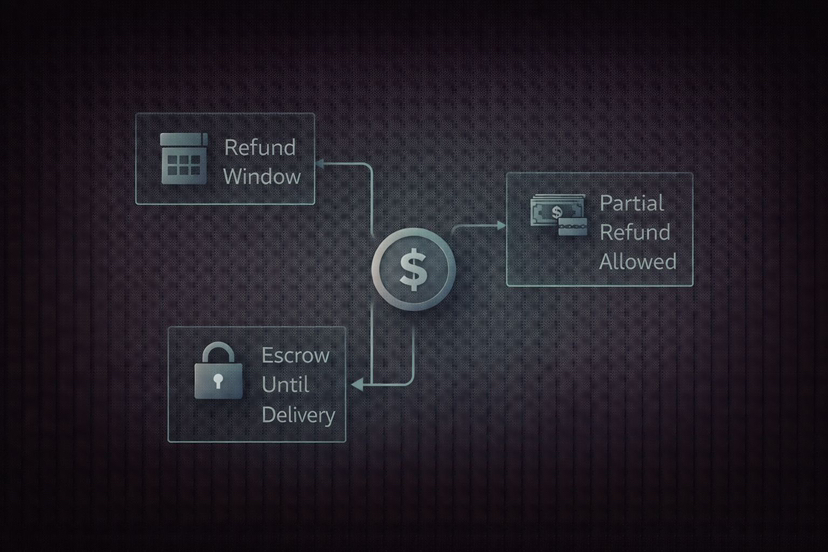

A sound stablecoin payment system can provide such things as:

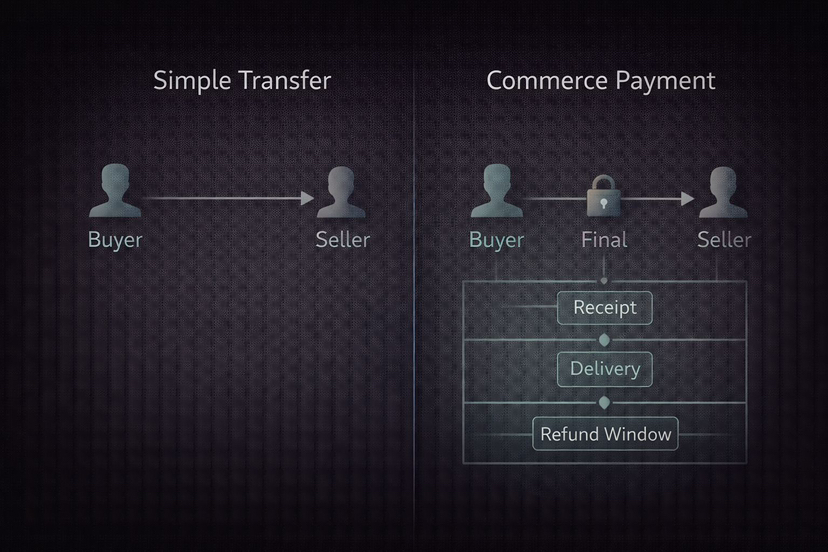

- A limited escrow period, during which the money is kept in lock and only when the goods have been delivered it is released automatically.

- A refund facility that is merchant controlled and is simple to activate and produces a clear records.

- Refund policies based on time were incorporated into payment system hence the buyer is fully aware of the rules prior to paying.

- Conflict resolution based on express agreement and not reversals of contests in the last minute.

These trends allow the buyer to feel safe without allowing one side to have unlimited authority.

This is the major point: stablecoins do not have to have chargebacks. They are in need of contemporary refund design.

The angle of plasma: a stablecoin business made to feel like an adult.

The public education of plasma on stablecoin chargebacks is important than it appears. When a network makes it clear that stablecoin payments lack the traditional chargebacks, it makes the right expectations. Misplaced expectations destroy trust. When individuals think that they have chargebacks and later find out that they do not, they get deceived.

But Plasma also foreshadows the next stop stablecoin payments can enable flexible refund functionality which can be used in a clean way by merchants. How mainstream retail applications can be unlocked without bringing the worst of card disputes in-house.

Here the wider design options of Plasma also come into play. A network centered around stablecoin-first flows simplifies developing wallet and merchant workflows centered on norms of stablecoins: immediate settlement, transparent history and basic post-payment operations such as refunds.

The next secure currency transaction application is not send USDT and hope. It is pay, keep track, refund, as any payment system presently.

Why refund design is also a compliance win also.

Customer experience is not the only thing about refunds. They also help compliance.

Transaction audit is easier where there are clear refund trails. When one of the customers is refunded, a clean record is made. In case a payment is challenged and adjudicated, it will be a clean record. That reduces ambiguity.

Uncertainties are what regulators despise. It is also the hate of finance teams. Properly designed refund procedures generate formal records, which simplify presentations by merchants, platforms, and payment providers of what transpired.

In stablecoin business, structured records can be the distinction between a rail that is adopted and a rail that is a niche.

So they are not a nice feature, refunds. They belong to the construction of a payment rail that the businesses can rely on.

The reason this is important most to e-commerce and services, and not crypto-native users.

You may not be preoccupied with refunds when you simply consider the crypto users. Several users of crypto have treated transfers as cash. However, stablecoin payments are not only used by crypto users, but they are used in everyday business.

E‑commerce needs refunds. Services need refunds. Travel needs refunds. Businesses that are subscription-centered require refunds. Marketplaces need refunds. Restaurants need refunds. The simplest retail system must be able to undo a transaction at will in a clean manner.

Should one of the stablecoins wish to go that world, they must have fast, transparent, and simple to implement refund logic.

This is why I consider the refund layer to be one of the largest silent unlocks to adopt stablecoins. It is not a social media trend, but it alters the behavior of buyers.

How successful Plasma can be in this refund-first story

When Plasma inclines towards this rightly, victory will be in readable payments of coin like cash in real life.

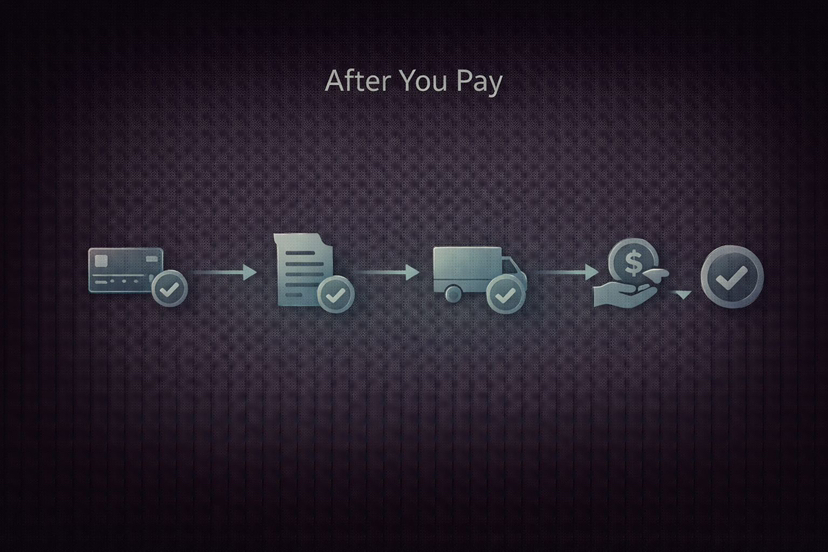

A customer will make a payment using stablecoins and receive a transparent receipt.

One gesture can enable a merchant to issue a refund and the customer can see it immediately.

The policy of refunds is not concealed somewhere in a help center at the time of purchase.

Disputes don’t become chaos. They get organized streams of which both parties are aware.

Merchants are no longer afraid of chargeback fraud, and consumers are no longer afraid of having no protection.

That is the happy medium: amicable final settlement.

The great point: when stablecoin payments cease to act like transfers and begin to act like commerce, they gain.

The last transition is an attitude change.

A transfer consists of nothing more than money moving.

Commerce is money in transit with anticipations: delivery, service, guarantees and reversals in case of failures.

The most promising opportunity of plasma is to ensure that stablecoin payments move past the category of fast transfer, to actually becoming commerce rails. Refunds are not a side topic. Refunds are the bridge.

And in case Plasma is able to clean and decipher that bridge, it will not be another stablecoin chain. It will be a part of the moment when stablecoins will be finally indeed usable money that can be used in the daily life.