Today, February 9, 2026, I want to take some time to explain a topic that has been quietly gaining attention across serious crypto and fintech circles. I’m Dr_MD_07, and today I’ll be writing about Vanar Chain and why it matters in the current market landscape. Vanar is not just another blockchain competing on speed or fees. It is being positioned as a fully integrated, AI-native blockchain stack designed specifically for PayFi and tokenized real-world assets, two areas that are increasingly shaping where this industry is heading.

Over the last year, the market conversation has shifted. Traders and builders are paying less attention to empty narratives and more attention to infrastructure that can actually support compliant payments, tokenized assets, and automated decision-making. Vanar enters this conversation with a clear structure. Instead of stitching together external tools, it offers an end-to-end on-chain system that combines transaction execution, AI logic, and data storage in a single coherent stack. This matters in 2026, as regulation, institutional participation, and real economic use cases are no longer optional topics.

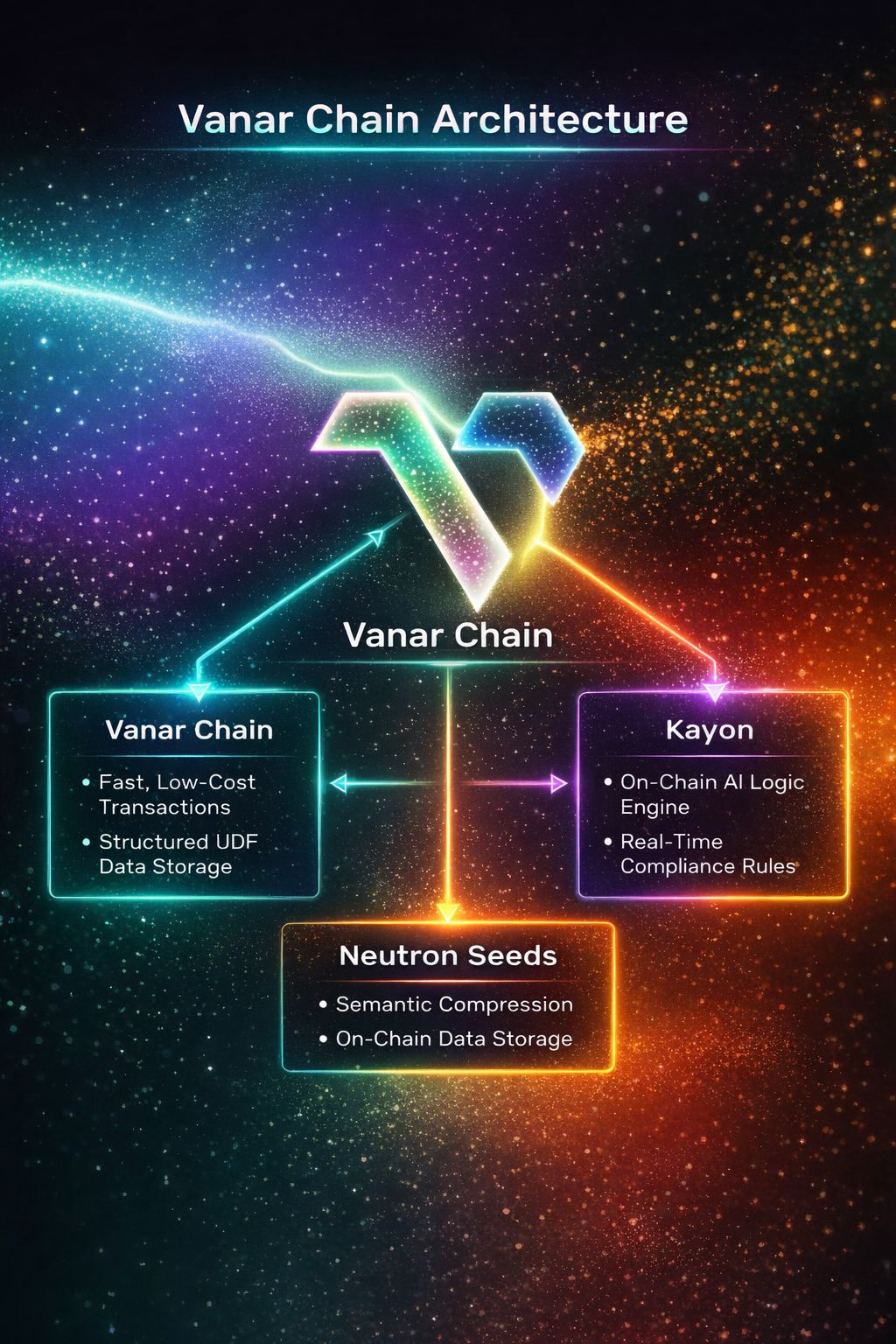

At the base of the system is Vanar Chain itself. This layer focuses on fast, low-cost transactions, which is something every chain claims, but Vanar approaches it with a more specific purpose. It supports structured UDF storage, meaning data is not just stored as raw bytes but in formats that can be queried and interpreted directly on-chain. In practical terms, this allows financial data, asset metadata, and compliance records to live natively on the blockchain without relying on external databases. For PayFi use cases, where speed, cost, and auditability all matter at once, this is a meaningful design choice rather than a marketing line.

On top of this transaction layer sits Kayon, the on-chain AI logic engine. Kayon is where Vanar starts to differentiate itself from most existing chains. Instead of pushing AI logic off-chain and trusting third parties, Kayon allows smart logic to query, validate, and apply real-time compliance rules directly on-chain. For example, payment flows or asset transfers can be automatically checked against predefined conditions, jurisdictional rules, or risk parameters before execution. This approach reflects a broader 2025–2026 trend where automation is no longer about speed alone, but about reducing human error and operational friction in financial systems.

The third core layer is Neutron Seeds, which handles semantic compression and on-chain data storage. This is one of the more technical components, but the idea is relatively simple. Legal documents, financial proofs, and compliance records tend to be large and complex. Neutron Seeds compress this information in a way that preserves meaning rather than just size. As a result, legally relevant data can be stored and verified on-chain without overwhelming the network. In a market where tokenized bonds, real estate, and invoices are becoming more common, this kind of data handling is increasingly necessary.

What makes Vanar interesting is not any single layer, but how these layers interact. Transactions are executed on Vanar Chain, validated and guided by Kayon’s AI logic, while Neutron Seeds ensures that the underlying data remains accessible, verifiable, and compliant. This creates a programmable financial foundation that can support payments, assets, and even autonomous agents without constant reliance on off-chain systems. From a trader’s perspective, this reduces unknown variables. From a builder’s perspective, it simplifies architecture.

Vanar is trending right now largely because PayFi and real-world asset tokenization are no longer theoretical. In late 2025 and early 2026, several jurisdictions finalized clearer frameworks for tokenized financial instruments, and large payment providers began experimenting with on-chain settlement layers. Infrastructure that can handle compliance, data integrity, and automation in one place naturally attracts attention. Vanar’s recent testnet expansions and developer activity reflect this shift, even if it’s not yet dominating headlines.

From my personal perspective, having watched multiple cycles, Vanar feels more like a response to market maturity than an attempt to chase hype. It doesn’t promise unrealistic throughput or dramatic narratives. Instead, it focuses on making financial logic programmable and verifiable. That may not excite short-term speculation, but it aligns well with where serious capital tends to move once markets stabilize.

Technically, none of the components are magic. Fast chains exist. AI logic engines exist. Data compression exists. What’s different is the decision to integrate them fully on-chain rather than treat them as modular add-ons. This reduces trust assumptions and operational complexity, which are two issues that have repeatedly caused failures in past blockchain systems.

Looking ahead into 2026, the success of Vanar will depend on adoption rather than design alone. Payment providers, asset issuers, and developers will ultimately decide whether this integrated approach delivers real efficiency gains. Still, as infrastructure conversations mature, Vanar’s architecture fits well with the current demand for compliant, automated, and transparent financial systems.

In a market crowded with chains solving yesterday’s problems, Vanar is clearly trying to address tomorrow’s. Whether it succeeds or not, it represents a thoughtful direction for blockchain infrastructure at a time when the industry needs fewer promises and more working systems.