I've been skeptical about crypto banking apps for years because most are just glorified wallet interfaces pretending to be banks. When Plasma announced Plasma One back in September promising 10%+ yields, 4% cashback, and physical cards working in 150 countries, my first thought was "sure, another vaporware announcement that never ships." But XPL sits at $0.0844 today up 0.60% with RSI at 32.28, and Plasma One is still in waitlist phase five months later, which tells you something about execution timelines versus marketing hype.

What makes Plasma One different from the dozen other crypto banking apps that launched and died isn't the technology. It's that Plasma has Tether CEO Paolo Ardoino as both angel investor and strategic partner, meaning USDT integration is native rather than afterthought. Plasma was literally designed from ground up with Tether involvement for stablecoin operations, not a general blockchain that added stablecoins later.

The Plasma One value proposition targets emerging markets specifically. Istanbul, Dubai, Buenos Aires get mentioned constantly in Plasma documentation because these are places where accessing dollars is valuable but traditional banking makes it expensive or impossible. Someone in Turkey dealing with lira volatility or Argentina fighting peso collapse wants dollar exposure without dealing with local banking restrictions.

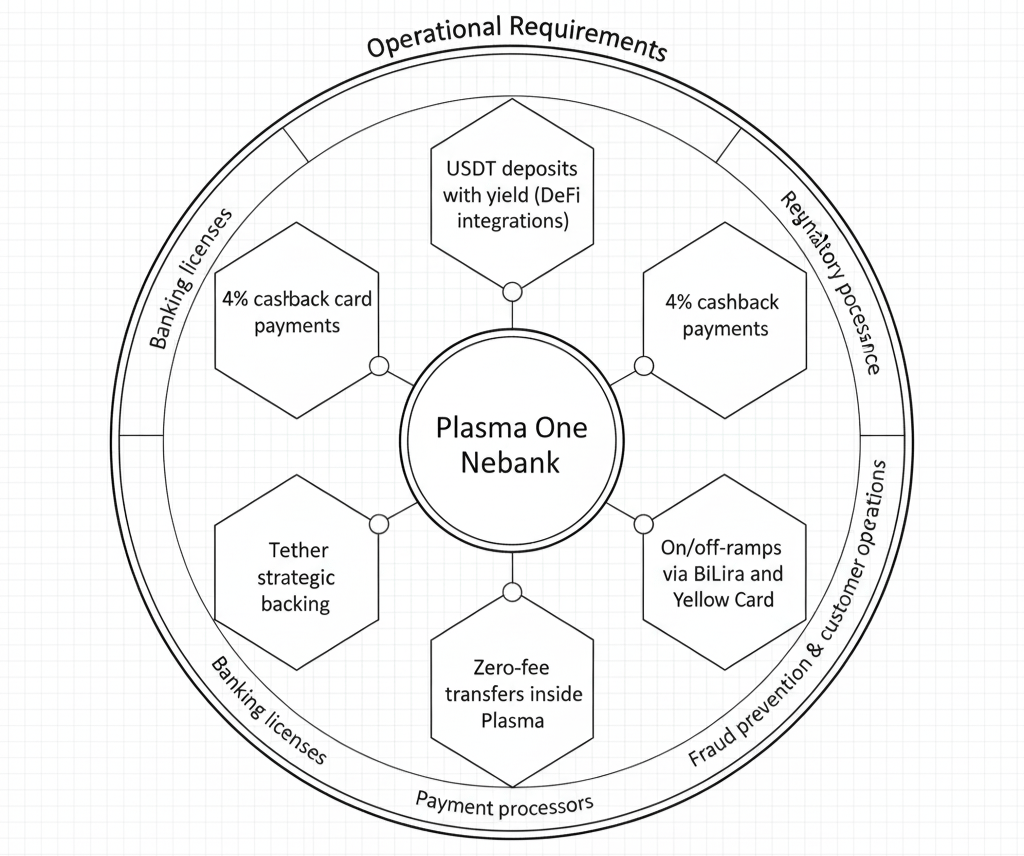

Plasma One promises to solve that by letting users hold USDT earning 10%+ yields directly in app, spend using physical cards getting 4% cashback, and transfer money fee-free inside the Plasma ecosystem. That's compelling if it actually works as described and regulatory approvals don't kill it before launch.

The yields come from DeFi integrations with Aave on Plasma where USDT deposits earn interest from borrowers. The 4% cashback presumably gets subsidized by Plasma treasury burning capital to acquire users, standard growth playbook. Physical cards working in 150 countries require payment processor partnerships and banking rails that take years to establish. That's why Plasma One is still waitlist only five months after announcement.

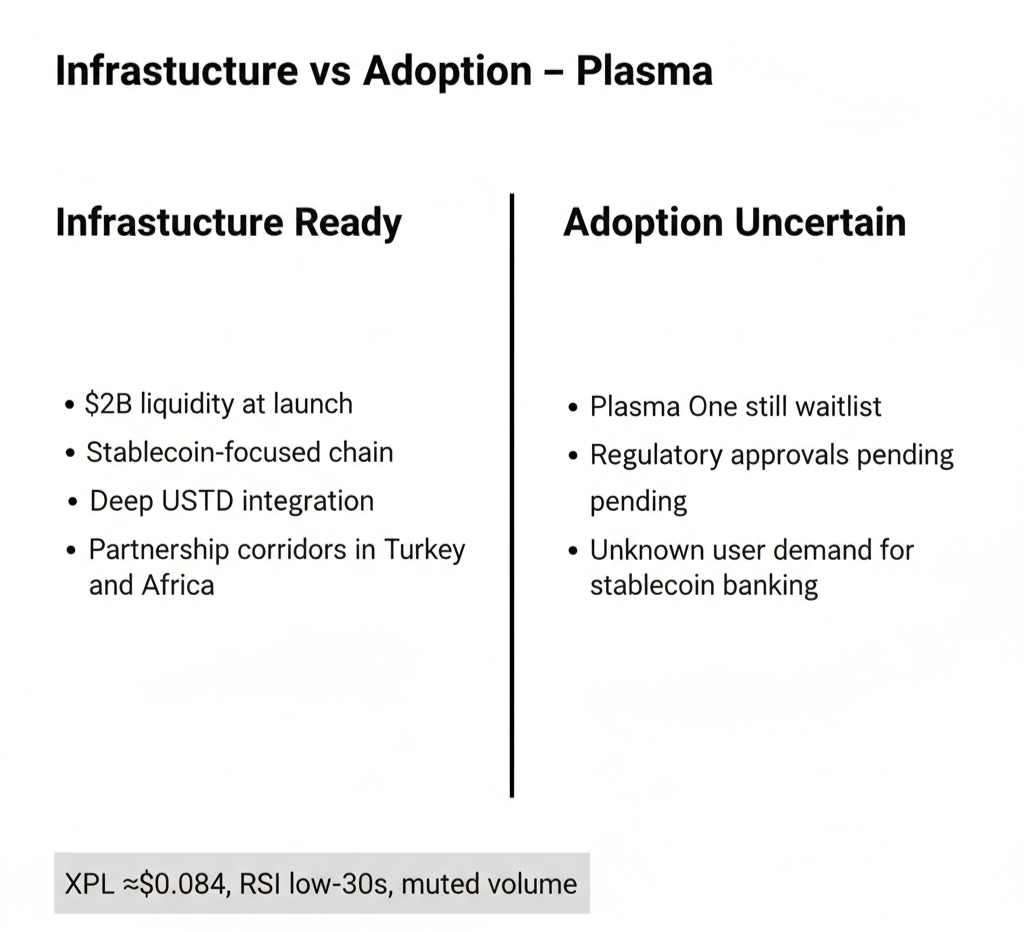

Building banking infrastructure is infinitely harder than building blockchain infrastructure. Plasma shipped mainnet beta in September with $2 billion deposits in 48 hours proving the blockchain works. But Plasma One neobank requires banking licenses, payment processor agreements, regulatory compliance in every jurisdiction, fraud prevention systems, customer service operations. None of that is engineering work, it's grinding operational execution dealing with regulators and banks who hate crypto.

Has Plasma made progress on any of that? Can't tell from outside because they're not publishing metrics. No user counts for Plasma One waitlist. No launch timeline beyond vague "coming soon." No details on which countries got regulatory approval or which payment processors signed deals. Just silence that usually means things are harder than expected.

The strategic rationale makes sense though. Plasma has zero-fee USDT transfers and deep Tether integration creating infrastructure for stablecoin banking. What it doesn't have is distribution to regular people who've never used crypto. Plasma One could solve distribution by packaging Plasma's infrastructure into consumer banking experience normal people recognize.

If Plasma One actually launches with promised features and gains traction in emerging markets, it validates the entire Plasma thesis about specialized stablecoin infrastructure. Suddenly you have real payment volume from real people using Plasma for actual banking not just DeFi speculation. That drives transaction fees that get burned offsetting XPL inflation and creates sustainable economics.

If Plasma One launches but nobody uses it because yields drop or cashback gets cut or regulatory problems emerge, then it proves building infrastructure doesn't solve distribution problems. You can have perfect technology and still fail commercially because getting users is harder than building products.

Current XPL price at $0.0844 with RSI at 32.28 doesn't price in any optimism about Plasma One succeeding. Markets assume either it never launches properly or launches without gaining meaningful adoption. Volume at 8.03M USDT is low suggesting traders aren't positioning for any catalysts.

The Tether relationship running deeper than standard blockchain integration matters enormously for Plasma One success chances. Paolo Ardoino backing Plasma as angel investor and Bitfinex co-leading funding rounds creates alignment you don't see with typical blockchain-stablecoin partnerships. Tether wants Plasma to succeed because it drives USDT usage and creates vertically integrated distribution for their stablecoin.

That strategic alignment could unlock doors for Plasma One that other crypto banking apps couldn't access. Banking relationships, regulatory approvals, payment processor deals all get easier when you have Tether's institutional credibility backing you. Whether that translates to actual launches in actual markets remains completely unproven.

Plasma also announced partnerships with Yellow Card for Africa remittances and BiLira for Turkish lira on/off-ramps. Those are exactly the emerging market corridors where Plasma One could get traction if executed well. Turkey especially makes sense given massive stablecoin adoption and currency volatility driving genuine demand for dollar access.

But partnerships announced don't equal products shipped. Plasma needs to actually launch Plasma One with real users in real markets to prove any of this matters. Five months of waitlist without launch suggests the operational challenges are bigger than anticipated or regulatory approvals are taking longer than planned.

The bull case is Plasma One launches in Q1 2026 gets hundreds of thousands of users in Turkey, Latin America, Africa within first year and drives meaningful transaction volume onto Plasma network. That would validate specialized stablecoin infrastructure thesis and create organic XPL demand from actual usage.

The bear case is Plasma One launches late, gets minimal adoption because yields drop and cashback gets cut to reduce burn, or doesn't launch at all because regulatory approvals fall through. Then Plasma remains DeFi chain processing minimal payment volume while XPL continues bleeding.

Plasma sits at an interesting inflection point. The infrastructure is built. The partnerships are announced. The strategic relationships with Tether exist. What's missing is shipping Plasma One and proving people want stablecoin banking enough to actually use it. Next few months probably determine whether this becomes real or just another ambitious crypto project that couldn't execute on distribution.

For now XPL at $0.0844, RSI 32.28, volume 8.03M shows markets waiting for proof. Plasma technology works but that was never the question. Question is whether Plasma One ships and whether anyone cares when it does. That's what determines if this infrastructure gets used or sits idle while capital moves elsewhere.