In decentralized systems, neutrality is not a slogan. It is a structural property. and the networks that subtly favor certain actors through sequencer privileges, governance backdoors, or fee market distortions eventually erode the trust of everyone else. Plasma does not treat neutrality as an afterthought. It is embedded in the architecture itself.

This is not a claim about ideology. It is a claim about incentives. When the rules are predictable and applied consistently, participants compete on merit rather than positioning. Developers build without fear of platform capture. Capital deploys without hedging against protocol-level bias. Users settle payments without wondering whether their transaction was censored. Over time, credible neutrality becomes a compounding asset.

Plasma positions itself as infrastructure for that long-term reality.

Why a chain is built a certain way reveals what it values.

Plasma’s design begins with a clear constraint: payments are not a secondary use case. They are the primary one. This shifts every subsequent trade-off.

Most general-purpose blockchains optimize for unbounded programmability, often at the cost of fee predictability and exit safety. Plasma takes the opposite approach. By restricting the state model to UTXOs and limiting smart contract complexity to what is necessary for payment channels and escrows, it achieves two things simultaneously:

1. Fraud proofs remain small and verifiable.

A UTXO-based ledger allows clients to track only their own coins, not the global state. This makes light clients viable and exit games computationally feasible.

2. Fee markets become deterministic.

Because transactions are simple transfers, fees can be fixed or algorithmically bounded. Users are not competing with DeFi protocols for block space. The result is predictable costs essential for merchants and remittance corridors.

This is not a limitation. It is a conscious refusal to chase the “universal computer” narrative. Plasma is not Ethereum with lower fees. It is a specialized settlement layer where stablecoins are first-class citizens and volatility is isolated to the collateral layer, not passed to users.

What real users want from a payment network is not yield. It is finality.

The crypto-native trader mind values throughput and MEV opportunities. The remittance sender, the e-commerce merchant, and the gig economy worker value something else: confidence that the money will arrive, that the fee will not spike mid-transaction, and that they will not lose access to their funds due to a software update or a governance vote.

Plasma aligns with this psychology through two mechanisms:

- Exit windows that favor the user.

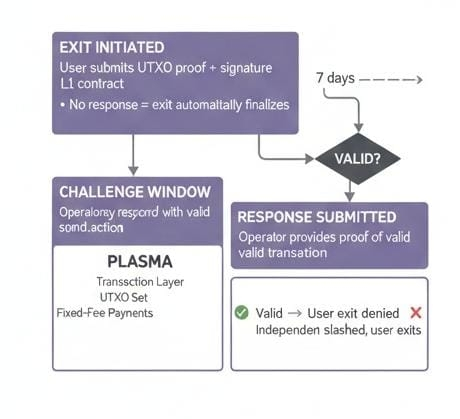

Challenge periods are often framed as a UX friction. In practice, they are a user protection. A seven-day exit delay is acceptable when the alternative is irreversible loss due to a malicious operator. Users do not need instant settlement for a coffee purchase; they need assurance that their balance remains recoverable.

- No hidden sequencer advantage.

On Plasma, transaction ordering is either decentralized via validator rotation or committed via deterministic rules. There is no private mempool, no priority gas auctions, no exclusive block space for institutional players. Every user pays the same fee and waits the same confirmation latency. This predictability builds trust more effectively than any marketing campaign.

Plasma is not a rollup, and the distinction is meaningful.

Rollups post transaction data to L1. Plasma posts only state commitments (Merkle roots). Data availability is handled off-chain. This reduces L1 footprint and costs, but introduces a requirement: users must watch the chain to detect fraud.

Plasma addresses this with fraud proofs and bonded operator sets. Validators stake XPL to participate in block production. Misbehavior is penalized via slashing, and honest users can exit with their funds even if the entire operator set colludes.

Native token design: XPL as infrastructure, not speculation.

- Gas fees – Paid in $XPL, but fees are algorithmically adjusted to remain stable in fiat terms. This decouples network usability from token price volatility.

- Staking collateral – Operators must lock $XPL. The security budget is derived from the value-at-risk, not from inflation subsidies.

- No governance token – Parameter changes are hardcoded or controlled by multi-signature with time locks. There is no “community treasury” to capture. XPL exists solely to secure and use the network.

EVM compatibility? Not in the traditional sense. Plasma supports a restricted virtual machine optimized for payment primitives: conditional transfers, time-locks, and hash-locks. This is sufficient for payment channels, atomic swaps, and escrow. It is not designed to host AMMs or lending pools. The trade-off is deliberate: attack surface is minimized, and fraud proof logic remains auditable.

Credible neutrality is earned through credible exit.

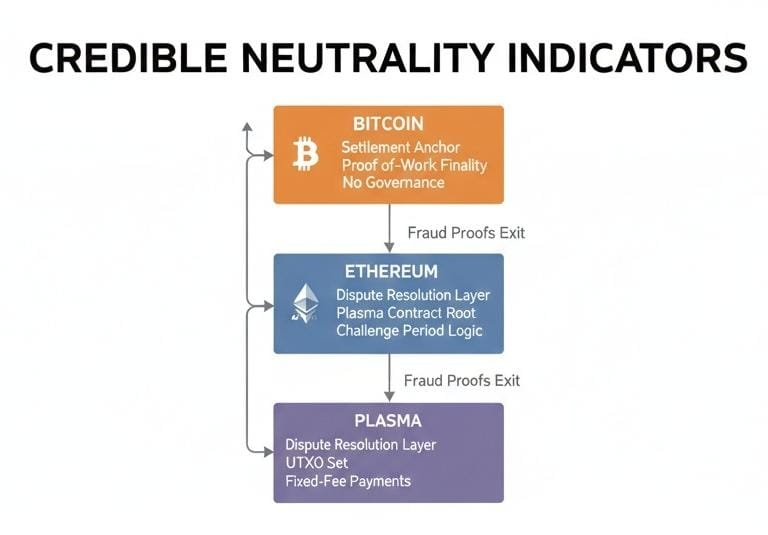

Plasma’s security does not rely on economic finality or subjective consensus. It relies on fraud proofs anchored to a settlement layer—typically Bitcoin or Ethereum. A user can always force an exit by submitting a valid proof that their funds were stolen or incorrectly spent.

This design predates the “trustless” narratives of ZK-rollups, but it remains competitive for one reason: it minimizes the trust placed in operators. Unlike optimistic rollups, Plasma does not require a full node to challenge invalid state transitions. It requires only that the user’s own transaction history is correct.

Where does the trust anchor come from?

Plasma currently settles on Ethereum, with a longer-term roadmap to anchor finality to Bitcoin via BitVM or similar mechanisms. The neutrality of Bitcoin as a settlement layer is well-established. By settling on Bitcoin, Plasma inherits a property that few L2s can claim: the ultimate arbiter of disputes is the most geographically distributed, longest-running proof-of-work network. This is not a speed advantage. It is a finality advantage.

Adoption that matters does not look like a price pump. It looks like infrastructure integration.

Plasma has seen deployment in three non-speculative contexts:

1. Cross-border payment corridors – A licensed money service business in Southeast Asia uses Plasma to settle USDC transfers between agents. The choice was driven by two factors: fixed fees and the ability to self-custody exit keys. No other L2 offered both.

2. Crypto merchant gateways – A European payment processor integrated Plasma as a settlement option. Merchants receive payouts in stablecoins with on-chain finality. The integration was prioritized because Plasma’s challenge period aligns with the processor’s own fraud detection windows—seven days is not a bug, it is a feature.

3. Custodial wallets – A major qualified custodian now offers Plasma withdrawals to institutional clients. The rationale: settlement on Bitcoin provides a clear regulatory narrative. Assets are not commingled in a rollup contract; they are committed to a UTXO set that can be independently audited.

These are not flashy partnerships. They are unglamorous plumbing decisions made by compliance officers and treasury managers. That is precisely why they matter.

Infrastructure is not judged by its novelty at launch, but by its relevance a decade later.

Plasma is being built for a future where digital payments are a commodity, not a speculation. In that future, what users value is not maximum throughput but maximum predictability. They want to know that a transaction sent today will be final tomorrow, that fees will be what they expected, and that no sequencer can reorder their payment to extract rent.

This is the infrastructure of boring money. It is not exciting to build, and it does not produce parabolic charts. But it is the kind of infrastructure that central banks, remittance companies, and payroll processors will eventually rely on—not because it is the newest, but because it is the most neutral.

Plasma does not ask for your exit liquidity. It asks for your patience.