Right now, almost nobody is watching what's quietly taking shape on the economic horizon. But by the time the average person realizes what's happening, markets will already be in freefall.

Right now, almost nobody is watching what's quietly taking shape on the economic horizon. But by the time the average person realizes what's happening, markets will already be in freefall.

Here's the reality check we all need to sit with

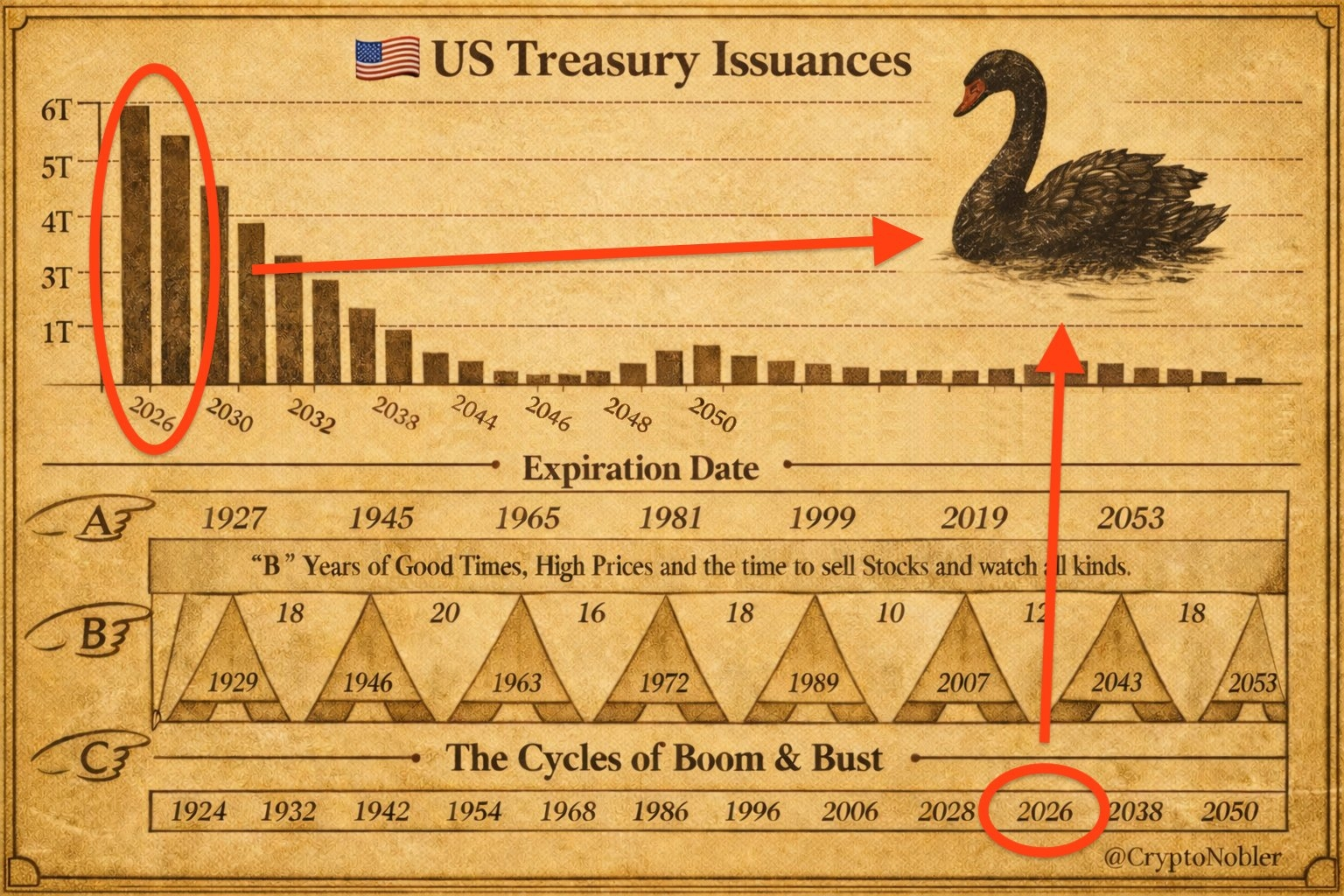

In 2026, $9.6 trillion of U.S. government debt matures in a single year.

That's more than one-quarter of America's entire national debt—coming due for refinancing all at once.

Let me break down why this actually matters, because it's not what most people assume.

Where did this mountain of debt come from?

During 2020 and 2021, when the pandemic upended everything, the government funded emergency relief through short-term borrowing. Interest rates sat near zero, so this made perfect sense at the time—why lock in higher rates when you can borrow cheap and figure it out later?

Well, later is now arriving.

Today, rates hover between 3.5% and 4%. And here's the uncomfortable math nobody in Washington wants to tackle: the U.S. doesn't have to repay all that debt outright. It has to refinance it.

Refinancing trillions at today's rates creates a vicious cycle. By 2026, annual interest payments are on track to exceed $1 trillion for the first time ever. That's not a line item—that's a fundamental shift in how the federal budget operates.

What this actually means for everyday people

→ The deficit expands automatically, regardless of new spending

→ Budget negotiations become increasingly brutal

→ The government loses its ability to respond to unexpected crises

→ Every dollar spent on interest is a dollar not spent on infrastructure, healthcare, or education

History shows us exactly how governments handle this situation. They don't slash spending—that's politically impossible. They don't default—that would unravel the global financial system. They do what they've always done: they cut rates.

Here's how this likely plays out

The U.S. hits a refinancing wall that makes the current interest math unsustainable. As debt service consumes more of the budget, political pressure reaches a breaking point. Meanwhile, inflation continues cooling and the labor market shows enough softness to justify action. The Federal Reserve gains the cover it needs.

Rate cuts stop being a policy choice and start being a necessity.

And here's the twist: a new Fed chair steps in during May 2026. The political signals are already flashing—we've heard direct calls from leadership that rates should be significantly lower.

What happens when rates finally fall?

Liquidity floods back into the system. Borrowing costs drop. Risk appetite returns with a vengeance.

And the assets that thrive in that environment? They don't just recover—they go parabolic.

We're talking about cryptocurrencies, high-beta stocks, speculative growth plays—everything that gets dismissed as "risky" during tight money periods becomes the exact place investors flock when liquidity returns.

The next eighteen months will test whether anyone's paying attention to what's refinancing beneath the surface. Most won't. But understanding the mechanics now means you're not reacting in panic later—you're simply watching the剧本 unfold as it always does.

Please don't forget to like, follow, and share! 🩸 Thank you so much ❤️