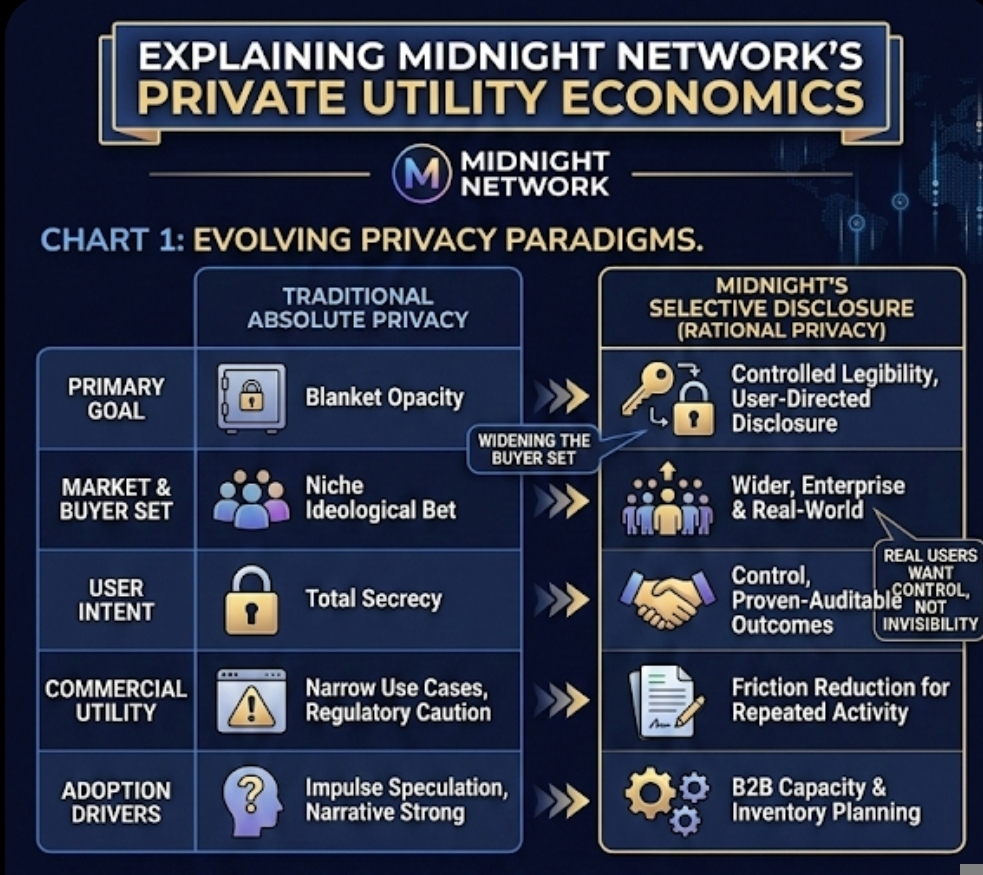

I remember watching privacy narratives trade a few cycles ago and noticing how often the market treated them like a simple ideological bet. Either a chain was “fully private” and therefore interesting, or it was not. Over time that started to look too clean to me. Real users do not usually want total secrecy. They want control. They want to prove one thing, hide five others, and keep moving. That is why Midnight caught my attention. The more I looked at it, the less it felt like a pure privacy trade and the more it looked like a market on selective disclosure, where the product is not invisibility but controlled legibility. Midnight’s own docs lean hard into that framing through “rational privacy,” zero-knowledge proofs, and user-directed disclosure rather than blanket opacity.

That distinction matters more than people think. Absolute privacy is emotionally strong as a narrative, but it narrows the buyer set. Selective disclosure widens it. A user can prove age without revealing a birth date. A firm can prove compliance without exposing all counterparties or internal records. Midnight is explicitly pitching that middle ground: private data handling with auditable outcomes when needed. From a trader’s perspective, that changes the question. I stop asking whether privacy is philosophically attractive and start asking whether this model can support recurring commercial behavior. That is a better question. Markets do not pay sustained premiums for ideals alone. They pay for systems that reduce friction for repeated activity.

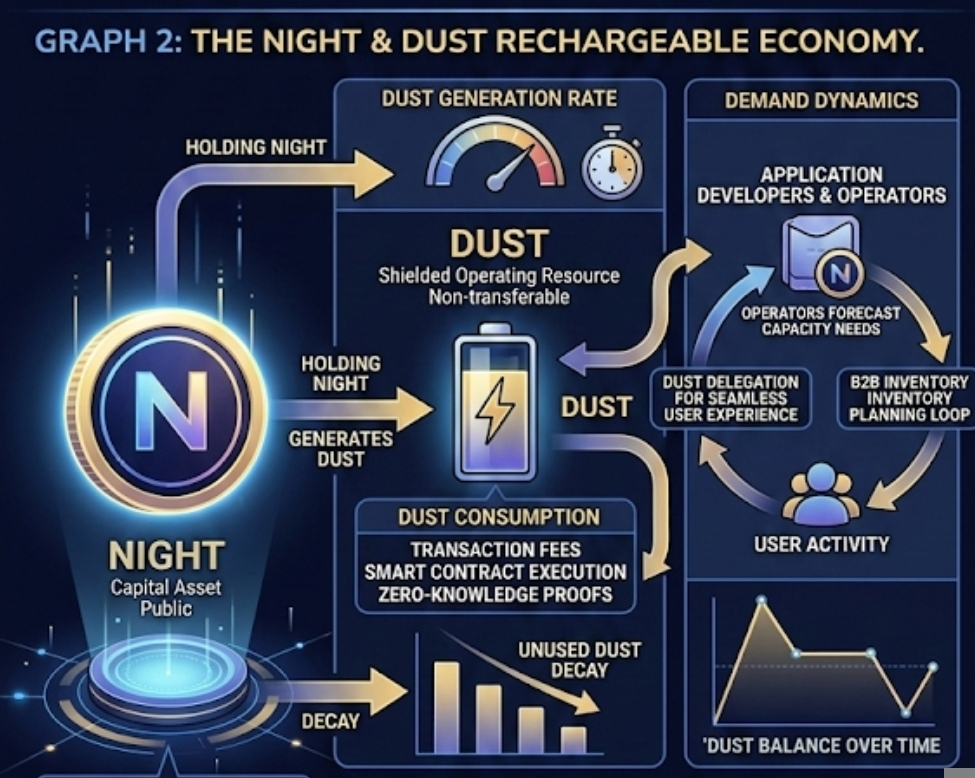

What caught my attention next was the economic design. Midnight separates the capital asset from the operating resource. NIGHT is the public token. DUST is the shielded, non-transferable resource used to power transactions and smart contract execution. Holding NIGHT generates DUST over time, and DUST decays if unused. Midnight describes it almost like a rechargeable battery rather than a spend-down gas token. That is an unusual structure, and I think the market still underestimates what it implies. If the model works, frequent users do not need to constantly market-buy the same way they would on a standard gas chain. They need access to capacity. That can be their own NIGHT balance, or delegated DUST from an application provider.

That sounds elegant, but this is where I slow down a bit. Elegant token models often look strongest in diagrams. The real test is operational behavior. If a developer holds NIGHT and uses the generated DUST to make the app feel free for end users, that can help onboarding. Midnight openly markets that as a benefit. But the tradeoff is obvious: user activity does not automatically become open-market fee demand in the way traders are used to modeling. Demand can get pulled one layer earlier, into application operators deciding how much NIGHT they need to warehouse in order to serve usage. So the core question is not “will transactions go up?” It is “will enough serious operators decide they need persistent capacity?” That is a different retention loop. It is more B2B than retail, more inventory planning than impulse speculation.

This is also where selective disclosure becomes more than a branding line. If Midnight were only a privacy chain, I would worry about the usual ceiling: strong narrative, weak institutional comfort. But the network is clearly trying to be usable in situations where proof and privacy need to coexist. The official material keeps returning to compliance, auditable reporting, private identity, and privacy-preserving financial workflows. Even the ecosystem examples now being highlighted, like shieldUSD, fit that pattern. The commercial logic is straightforward: if data exposure is the thing stopping a user, an enterprise, or even an AI-driven workflow from moving on-chain, then selective disclosure is not a feature. It is the transaction enabler.

Still, mechanism risk is real. Midnight’s current design ties consensus to a partner-chain structure linked to Cardano infrastructure, with validator selection accounting for Cardano SPO participation, while the mainnet rollout is beginning through a federated validator phase before broader expansion. That can help early stability, but it also means the market should not confuse “mainnet exists” with “economic decentralization is fully solved.” Early-stage chains often get priced on symbolic milestones long before their demand loops settle. If the validator set is stable but usage is thin, the story can outrun the evidence. If the privacy guarantees are strong but tooling is hard, developers stall. If DUST delegation works in theory but operators do not see repeatable end-user value, the retention problem shows up fast. People visit once and never build this as a habit.

Then there is supply. Midnight’s official tokenomics material sets total NIGHT supply at 24 billion, and the January network update says 4.5 billion NIGHT was allocated through Glacier Drop and Scavenger Mine. That does not tell me everything I would want to know as a trader. I still care about effective float, custodial concentration, exchange inventory, unlock timing, and whether delegated capacity ends up sitting inert in large balances. But it does tell me one important thing: this is not a tiny-float reflexive asset where scarcity alone will carry the chart forever. The network will eventually need absorption through real usage, governance relevance, block production incentives, and operators choosing to hold NIGHT because DUST generation matters to their business. Without that, FDV-style thinking comes back hard.

At first I assumed the bullish case would mostly be about privacy demand. Now I think that is incomplete. The stronger case is that Midnight could become infrastructure for situations where public chains reveal too much and private systems prove too little. That is a narrower story, but a more durable one. I would get more constructive if I saw repeated signs of capacity demand: developers actually warehousing NIGHT, production apps consuming DUST regularly, growth in node participation, and ecosystem tools making private apps measurable enough that outside capital can evaluate traction. Midnight is already pushing developer readiness, indexer infrastructure, wallet tooling, and a March 2026 mainnet launch sequence, which is the right direction, but direction is not the same as proof.

So this is where I land. Midnight’s real bet does look like selective disclosure, not absolute privacy, and I think that is the smarter market bet. But traders should resist turning that into a clean narrative too early. Watch whether selective disclosure creates recurring economic behavior, not just good conference language. Watch who keeps holding NIGHT when attention fades. Watch whether DUST becomes a real operating resource rather than a clever tokenomic diagram. In markets like this, behavior usually tells the truth before the story does.

Articolo

Midnight’s real bet may be selective disclosure, not absolute privacy

Disclaimer: Include opinioni di terze parti. Non è una consulenza finanziaria. Può includere contenuti sponsorizzati. Consulta i T&C.