I’ve been watching tokens long enough to know when the market is pricing fear versus when it’s pricing reality. A couple of nights ago I pulled up the $SIGN chart around 2 a.m., coffee going cold, and something clicked in a way it hadn’t before. The token had just dropped nearly 39% in seven days while the rest of the market was only mildly red. At first glance it looked like the usual pre-unlock panic. But the more I dug price action, volume, the thin float the more it felt like the panic had already done its job. The April 28 backer unlock, the one everyone is still whispering about, appears to have been sold in advance. What’s left is a cleaner setup than almost anyone is giving it credit for.

Let me walk you through how I got there, because this isn’t some recycled tokenomics pitch. It’s just what the tape is actually showing right now.

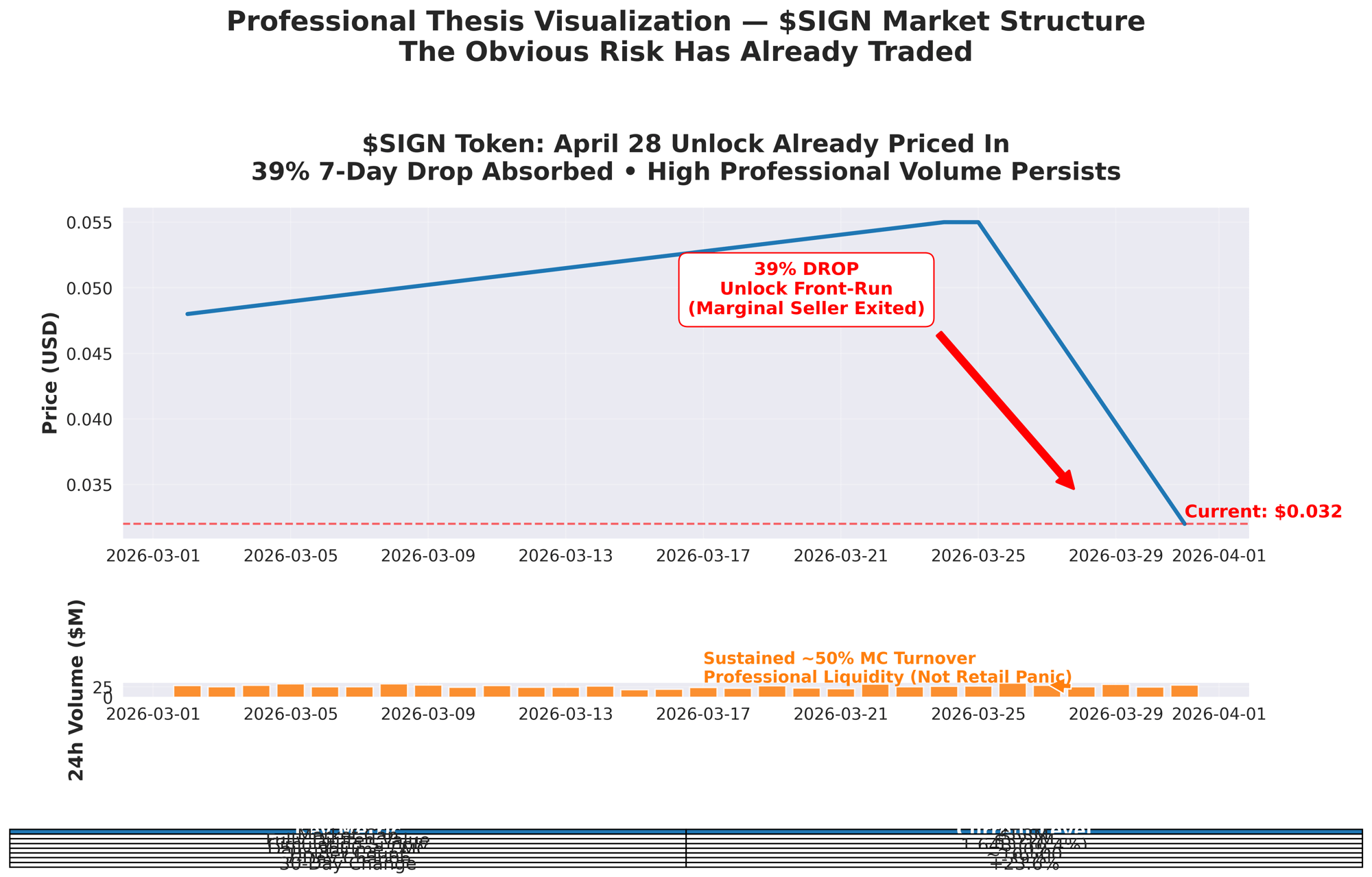

The circulating supply is still sitting at 1.64 billion out of 10 billion total exactly 16.4%. The next meaningful release is the backer tranche on April 28, roughly 296 million tokens. That’s not a slow monthly drip; it’s a single day jump that will lift the float by about 18%. At today’s price around $0.032, that’s real money hitting the market. Yet the chart didn’t wait for the date. It already gave back the better part of two months’ worth of gains in a week. To me that reads like the marginal seller who was going to dump on the unlock has already left the building. The fear trade is exhausted before the actual event.

What makes this feel even more interesting is the relationship between market cap and fully diluted value. We’re looking at roughly $53 million MC against a $322 million FDV still a 6× premium on future supply. Normally that ratio screams overhang and makes me nervous. But when the single biggest near-term supply event has already been frontbrun so aggressively, the multiple starts to look more like compressed risk than a valuation trap. If even modest real-world usage (new attestations, government pilots, credential volume) picks up after April, that FDV gap could close faster than the usual post-unlock despair would suggest.

Then there’s the volume. Twenty-four-hour turnover has been running between $24 million and $29 million lately broughly half the market cap on many days. For a sub-$60 million token that is not normal retail noise. It feels like professional liquidity rotating on the big CEXs, particularly Binance, where depth is actually decent for the size. This isn’t DEX flippers chasing a meme; it’s the kind of persistent churn you see when a handful of well-capitalized players treat the ticker as a proxy for actual infrastructure contracts rather than the next airdrop lottery ticket. High velocity in a low-float name usually scares people, but here it has held up through the drawdown instead of evaporating.

Holder count sits at around 16,500 wallets. That’s not a broad retail army, which is exactly why the price didn’t cascade further on the way down. The circulating float is thinner than the headline 16.4% implies once you account for the big locked foundation and team buckets. Yet the daily volume keeps coming from somewhere likely the same concentrated set of market makers, early ecosystem wallets, and sovereign-aligned capital that understands the long game. Low holder numbers can be a red flag for illiquidity, but right now they look more like a feature: fewer weak hands to shake out, more coordinated conviction if the post-unlock tape stays calm.

And the price structure itself? After that steep weekly leg lower, it has tightened into a narrow band between roughly $0.0315 and $0.0335 with very little drama. The 30-day picture still shows net positive ground despite the recent blood. Buyers stepped in where classic unlock narratives usually trigger freefall. It feels less like a broken chart and more like a market that has already digested the obvious risk and is now waiting to see what actual adoption does next.

Of course I’m not blind to the counter case. That elevated volume to market cap ratio could just be hot money that chased the Binance listing and will evaporate the moment backers treat April 28 as an exit ramp. In a thin holder base, what looks like sticky liquidity can disappear fast if the incentive alignment isn’t there. I’ve seen it before high turnover masking weak hands instead of strong ones.

Still, the setup feels rare enough that I’m paying close attention. What would confirm this thesis for me? After April 28 the circulating supply jumps, yet 24-hour volume stays north of 40% of the new market cap and price either holds or reclaims $0.035 within a couple of weeks. That would tell me the liquidity providers aren’t the backers dumping but the ecosystem players accumulating. Even better if on-chain attestation numbers or fresh government milestones show up around the same time without the price buckling.

What would kill the idea? Price slides another 25% in the week after the unlock while volume collapses below 20% of market cap. That would mean the recent crash was pure speculation front-running, not smart money repositioning, and the dilution narrative wins again.

I’m not here to hype or hand out price targets. I’m just sharing the observation that keeps me up at night in a good way: the most obvious risk on the calendar for $SIGN looks like it has already traded. The token now sits with a thin float, thick professional liquidity, and a market that seems to be betting the real adoption curve starts once the last major cliff is behind us. Whether that bet pays off is going to be visible on the tape by the end of April. For now, it’s one of the more intriguing asymmetries I’ve seen in the small cap infrastructure space in a while.

@SignOfficial #SignDigitalSovereignInfra $SIGN