I used to believe the main problem with money was just how slow it moved. If a transfer took three days, I figured the system was simply old-fashioned. All we needed were faster pipes, slicker apps, and smarter automation to bring it into the modern world. After all, we send messages across the globe in a blink, hop on video calls like it’s nothing, and watch information zip around faster than we can keep up. So money dragging its feet felt like a glitch that technology would eventually iron out.

That idea wasn’t totally off base. It was just a bit innocent.

Because money isn’t the same as data. Money is coordination — it’s about getting people, businesses, and institutions to move in sync.

The change in my thinking didn’t hit me while reading some technical paper. It came from real conversations with friends who were quietly struggling.

A couple of weeks ago, I was grabbing coffee with a buddy who runs a small import business. He glanced at his phone, let out a tired sigh, and said, “I sent the payment three days ago. It still hasn’t shown up.” He wasn’t mad — just worn down. Then he added the part that really stuck with me: “I don’t even know where it is.”

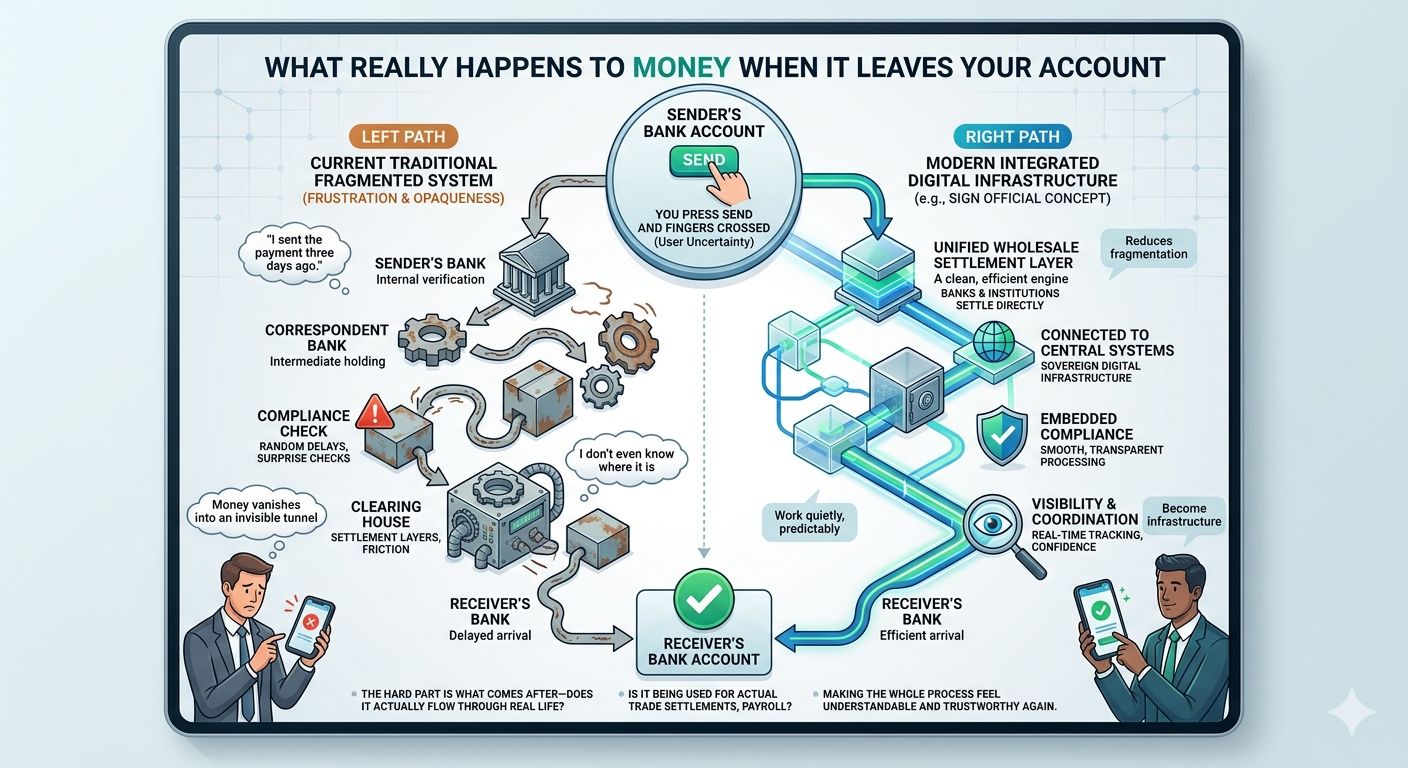

That simple sentence hit different. We can track a package from one country to another, see exactly where our food delivery is on a map, and know the second someone reads our text. But when it comes to money — the lifeblood of everything — it just vanishes into some invisible tunnel. You press send and cross your fingers.

A few days later, another friend who owns an online shop told me almost the exact same story: random delays popping up, surprise compliance checks, and cash flow getting jammed right when she needed it most. It stopped feeling like bad luck and started feeling like the normal, frustrating way things are set up.

That’s when my question shifted. Instead of asking why money is so slow, I found myself wondering: what actually happens to it once it leaves my hands?

Building something new is the exciting part. Anyone can launch a flashy system and talk about revolutionizing finance. The hard part is what comes after — does it actually flow through real life? Does it quietly support payroll, supplier payments, cross-border deals, and everyday spending? Or does it stay stuck on the sidelines, another clever idea that never quite becomes part of how the world works?

So many systems fall short not because the dream was bad, but because they never become infrastructure — the kind of thing you rely on every day without even noticing it. Like a beautifully built road that leads nowhere useful.

That’s how a lot of today’s financial world feels. Money doesn’t simply jump from my account to yours. It has to weave through banks, compliance teams, settlement layers, and scattered networks. Every handoff adds friction, confusion, and that uneasy feeling of not knowing what’s happening.

I started paying closer attention to projects that seemed to tackle the deeper, hidden parts of the system instead of just making the surface prettier. That’s how I came across Sign Official and their focus on building sovereign digital infrastructure.

What drew me in wasn’t the usual hype about being faster or cheaper. It was the way they were thinking about the structure: creating a clean wholesale layer where banks and institutions can settle with each other directly and transparently, connected properly to central systems, while keeping the everyday retail side familiar and easy for regular people and businesses.

The idea isn’t to tear everything down. It’s to reduce all the fragmentation that makes money get lost between disconnected pieces. When issuance, settlement, compliance, and visibility work more as one coherent system, coordination starts to feel natural instead of mysterious. The apps and interfaces we use every day stay recognizable, but underneath, things actually move more smoothly and predictably.

Of course, the real proof isn’t in the diagrams or promises. It’s in whether it becomes part of daily economic life. Will businesses start using it for real payments because it actually cuts the uncertainty and stress? Can it turn into the kind of reliable background layer we barely think about, like electricity or roads?

When I look at something like this, I watch for the human signals: Is it being used because it genuinely solves problems, or mostly because of temporary rewards and buzz? Are more institutions and businesses weaving it into their regular routines — actual trade settlements, supplier invoices, payroll — or does the activity spike only during announcements? Does every new participant make the whole thing stronger and more useful for everyone?

The frustrations are very real. Sending money across borders is still messy and unpredictable. Compliance rules keep adding friction. Businesses are working globally, yet the money moving behind the scenes often feels stuck in old, opaque systems. If something can bring real clarity and steady flow without needing constant hype or incentives to keep going, that feels like it could actually last.

At the end of the day, my friend wasn’t just annoyed about a late payment. He was pointing to something deeper — a quiet erosion of trust when you send money and have no idea where it’s gone or when it’ll arrive.

Maybe the future of money isn’t only about making everything lightning quick and flashy. Maybe it’s about making the whole process feel understandable and trustworthy again. So reliable that we stop wondering “where did it go?” Not because we’ve stopped caring, but because the system finally does what good coordination is supposed to do: work quietly, predictably, and in support of real human economic life.

That’s the kind of change I’m keeping an eye on.

@SignOfficial #SignDigitalSovereignInfra $SIGN