Executive Summary

The recent market reaction to speculative reports about AI-driven payment disruption—triggering a 4–12% drop in card network stocks—was not an overreaction. It was an early signal of a structural shift that incumbents themselves are now racing to address. This article provides a systematic analysis of why traditional interchange fees are vulnerable to agent-led commerce, the infrastructure being built to replace them, and what the next three to five years will actually look like.

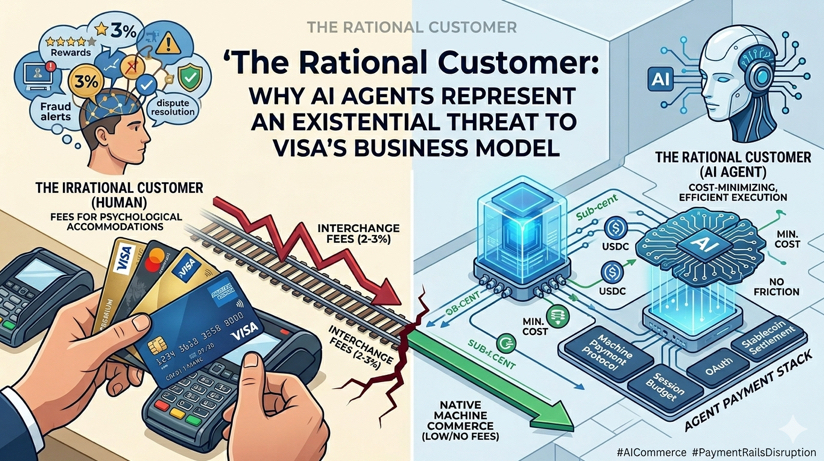

1. The Cognitive Asymmetry That Built a $500 Billion Empire

What Visa Actually Sells

Visa does not move money. It moves trust. The 2–3% interchange fee merchants pay covers a bundle of services that only irrational humans need:

Fraud protection – Humans lose cards and fall for phishing.

Dispute resolution – Humans regret purchases or receive damaged goods.

Reward points – Humans respond to gamification and status signals.

Zero-liability guarantees – Humans feel anxious using cards abroad.

These are not technical requirements. They are psychological accommodations. Visa’s moat has never been technological superiority—it has been behavioral economics embedded into a two-sided network.

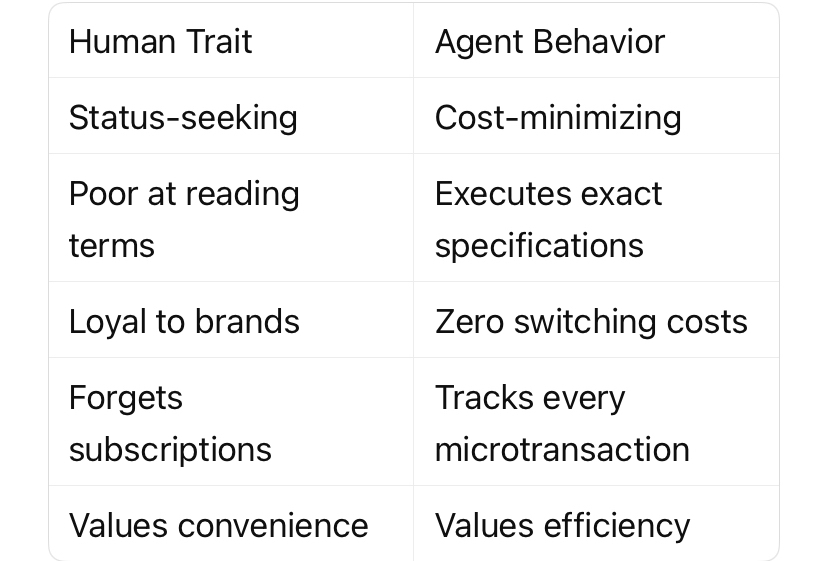

The Rationality Gap

AI agents exhibit none of the traits that justify interchange fees:

Key insight: The 2–3% fee is not a transaction cost. It is a tax on human irrationality. Agents refuse to pay it by design.

2. The Infrastructure Avalanche: What Launched in Three Weeks

March 2026 will be remembered as the week the agent payment stack became real. Four parallel developments signal coordinated recognition of the shift:

Tempo Mainnet + Machine Payment Protocol (MPP)

Backers: Stripe, Paradigm

Mechanism: Session-based authorization – agents receive a spending limit once, then execute continuous micropayments for data, compute, or API calls

Authentication: OAuth-style, not per-transaction card authorization

Design partners: Anthropic, DoorDash, Mastercard, Nubank, OpenAI, Ramp, Revolut, Shopify, Standard Chartered, and Visa itself

The inclusion of both Visa and Mastercard as design partners is telling. Incumbents are not ignoring the shift—they are attempting to co-opt it.

Visa’s CLI Commerce Tool

Visa’s crypto division released a command-line interface enabling AI agents to make terminal payments without:

API keys

Accounts

Human authorization

This is Visa admitting that its traditional merchant onboarding and authentication model is too heavy for machine-to-machine commerce.

Mastercard Acquires BVNK ($1.8B)

A stablecoin infrastructure startup at nearly $2 billion valuation. Mastercard is buying its way into programmable, agent-ready money movement.

Circle’s Nanopayments

Sub-cent, gas-free USDC transactions on a beta network. Designed for pay-as-you-go APIs where transaction values fall below credit card minimums.

Worldcoin’s AgentKit

Cryptographic proof-of-personhood for agents, allowing platforms to verify that an agent legitimately represents a real human without blocking automated commerce.

Takeaway: The infrastructure for agent-led payments is no longer theoretical. It is live, funded, and backed by every major player in payments and AI.

3. The Paradox: Incumbents Are Not Standing Still

The Defense Argument

Visa and Mastercard can argue that their distribution advantages will persist:

Merchant acceptance networks built over decades

Consumer trust and existing wallet relationships

Regulatory relationships and compliance infrastructure

Balance sheets to acquire or replicate new technology

Stripe processed $1.9 trillion in 2025, up 34% year-over-year. These networks are not shrinking.

The Flaw in the Argument

The two-sided network flywheel relies on human behavior:

Merchants accept Visa because consumers hold Visa. Consumers hold Visa because merchants accept Visa.

Agents break this loop. They have no wallets, no brand loyalty, no preference for Centurion lounges. When an agent is the buyer:

It queries all available rails simultaneously

It selects the lowest-cost, fastest-settlement option

It switches rails for every transaction with zero friction

The network effect collapses when the customer has perfect information and zero emotional attachment.

4. Where We Actually Are: Data vs. Narrative

The current narrative is moving faster than the transaction volumes. Precision matters.

Metric Value Interpretation

Agent-driven commerce has not yet scaled. The merchants building native agent services, the enterprises deploying agents as primary buyers, and the transaction volumes needed to stress-test new economics are still in development.

Where Disruption Hits First: Micropayments for AI Infrastructure

Not consumer retail. Not travel booking. AI infrastructure itself.

An agent completing a research task may call hundreds of specialized data APIs per session. Each call costs fractions of a cent. Over a week, that developer might generate $40 in revenue from one user.

Credit card networks cannot process this:

Minimum transaction amounts (often $0.50+) break the economics

Merchant onboarding takes days, not milliseconds

Per-transaction fees (e.g., $0.30 + 2.9%) exceed the transaction value

This commerce is structurally incompatible with Visa’s rails. Protocols like x402, Nanopayments, and Tempo are built specifically for this use case.

5. The Consumer Commerce Scenario (Citrini’s Model)

McKinsey estimates $3–5 trillion in AI-agent-facilitated consumer transactions by 2030. The Citrini report that spooked markets modeled a plausible sequence:

1. 2026-2027: Agents handle routine, low-stakes purchases (groceries, subscriptions, travel rebooking)

2. 2027: Stablecoin settlement between agents bypasses card networks for a meaningful percentage of e-commerce

3. 2028: Interchange fee revenue at affected issuers declines 15–20%

4. 2029: Consumer behavior shifts—users delegate more discretionary spending to agents

Caveat: This requires consumers to trust agents with purchasing decisions they currently make themselves. That trust is not guaranteed and will not arrive uniformly.

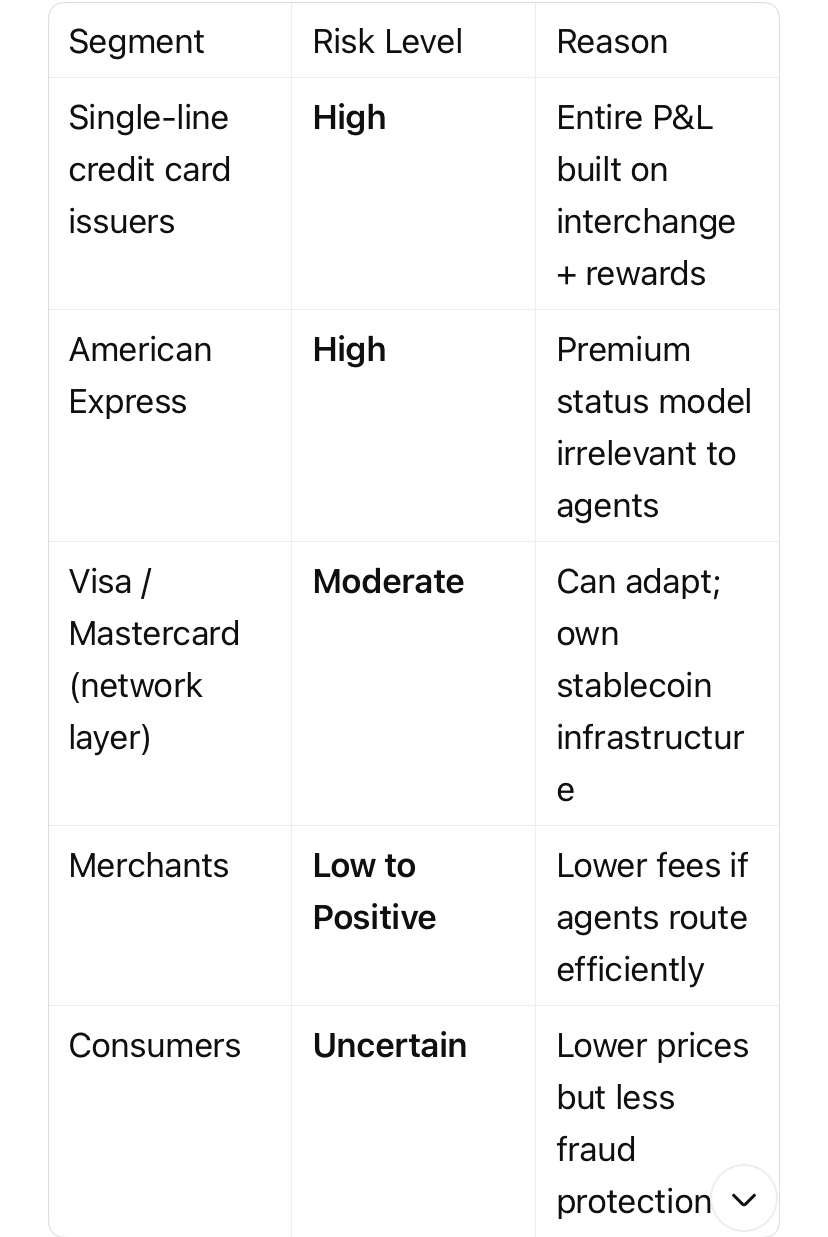

Who Is Most Exposed?

6. What It Means for Financial Professionals

For Payment Network Analysts

Monitor not transaction volumes but authorization methods. When OAuth-style session budgets replace per-transaction card authorizations in API logs, the shift has begun.

For Credit Issuers

The rewards points arms race is a zero-sum game among humans. Agents do not collect points. If 20% of your transaction volume moves to agent-led stablecoin settlement, your rewards liability drops—but so does your interchange revenue. The net effect depends on your cost structure.

For Merchants

Lower payment processing fees are coming, but not immediately. Early agent commerce will be in digital goods and API access. Physical goods still require fraud protection, dispute resolution, and consumer trust—services agents do not need but humans do.

For Regulators

Stablecoin settlement between agents raises questions about:

Anti-money laundering (who is the counterparty?)

Consumer protection (when an agent makes an erroneous purchase)

Tax reporting (microtransaction aggregation)

7. Conclusion: Disrupted by a Better Customer

Visa is not being disrupted by a better technology. It is being disrupted by a better customer—one that does not require fraud protection, reward points, or status validation.

The 2–3% interchange fee is not a technical necessity. It is a behavioral tax on human irrationality. And irrationality is not a feature agents possess.

The signal to watch: Not whether Visa survives—it likely will, in some form. But whether the next $500 billion payment company is built on rails designed for machines, not for humans anxious about swiping their card abroad.

Visa spent $1.8 billion last week to ensure it wouldn’t be left out of the answer. That is the clearest possible confirmation that the question matters.

#AICommerce #PaymentRailsDisruption #StablecoinSettlement #Web3Education #ArifAlpha