If you blinked, you probably missed it: while everyone argued about memecoins and ETFs, stablecoins quietly processed more value in 2025 than Visa.

That’s not a typo. Binance Research estimates that stablecoins moved around 33 trillion dollars in 2025, versus roughly 14 trillion on Visa’s network, even after stripping out MEV and internal exchange flows.

The punchline? As the U.S., EU, and key Asian hubs roll out serious stablecoin laws, the market is tilting toward a new breed of fully‑backed, fully‑disclosed, policy‑aligned tokens—and Binance is already rewiring its ecosystem around them.

From “crypto dollars” to regulated settlement rails

For years, stablecoins were treated like a handy hack: offshore crypto dollars you used because bank wires were slow and expensive. Now, regulators are hard‑coding what a “good” stablecoin looks like.

In the U.S., the GENIUS Act finally gives payment stablecoins a federal home: 1:1 dollar‑pegged, backed by cash and short‑term Treasuries, issued by supervised banks or licensed non‑banks, with monthly attestations and full AML/Bank Secrecy Act obligations. This is a big shift from the previous grey zone where no one could say definitively whether a stablecoin was a security, a commodity, or something in between.

Europe’s MiCA regime takes a different route but lands in a similar place: single‑currency payment stablecoins are e‑money tokens (EMTs), multi‑reference coins sit in the asset‑referenced token (ART) bucket, and both categories face authorization, reserve, and disclosure rules if they want EU‑wide distribution.

Meanwhile, Singapore, Hong Kong, and Japan have quietly built some of the strictest—and most forward‑looking—stablecoin laws in the world. MAS’s Single‑Currency Stablecoin framework requires 100% high‑quality liquid reserves, segregated custody, monthly checks, annual audits and five‑day par‑value redemption. Hong Kong’s new licensing regime pulls fiat‑referenced stablecoin issuers under HKMA supervision, while Japan only lets banks, trust companies, and registered funds‑transfer providers issue fiat‑pegged tokens under its electronic payment instrument rules.

The message is consistent: if you want to be the digital dollar (or euro, yen, or SGD) that banks can actually touch, you must be boring in exactly the right ways.

Reserve transparency: the new trust primitive

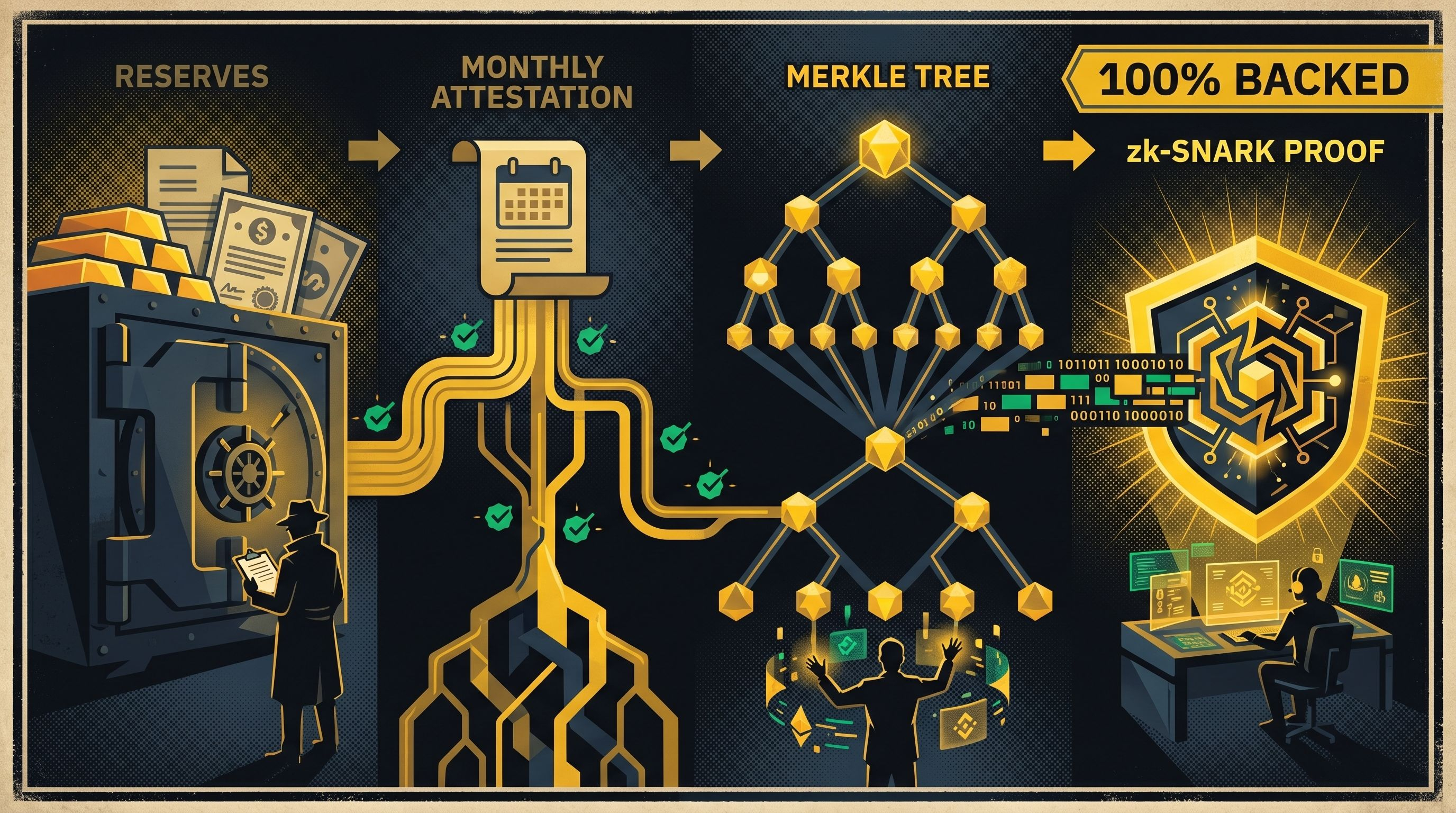

All of these laws converge on one core idea: reserve transparency.

At a minimum, that means an issuer has to spell out what backs each token—cash, T‑bills, repos, bank deposits—and how those assets are split across custodians and maturities. It also means independent assurance that reserves always meet or exceed tokens in circulation, usually via monthly attestations plus annual audits.

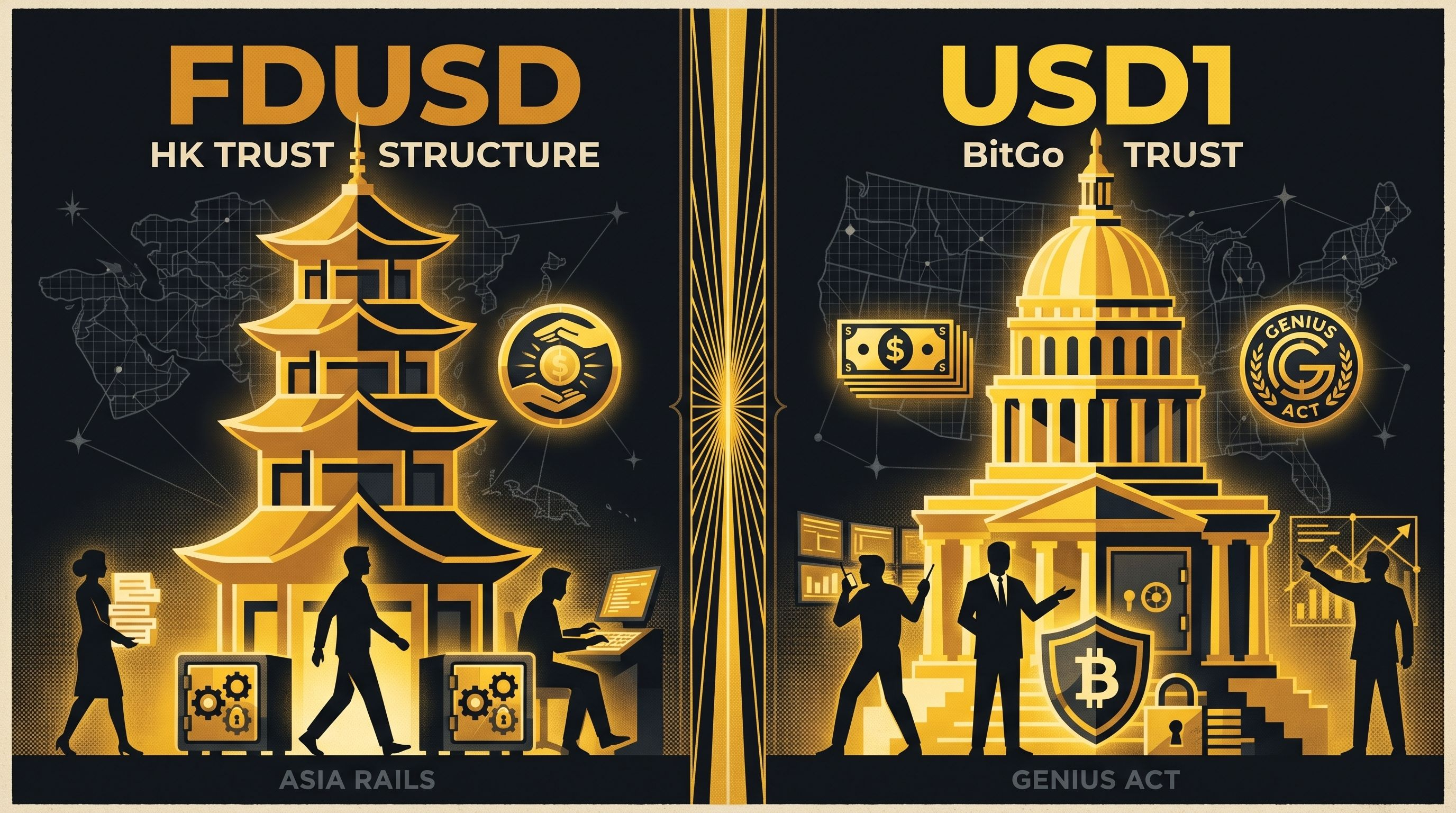

In Hong Kong and Japan, regulators go further, pushing issuers toward segregated trust accounts where token holders have priority claims if something goes wrong. That structure is exactly what you see with First Digital’s FDUSD, which uses a Hong Kong‑regulated trust company and segregated accounts for its USD reserves.

Binance adds a crypto‑native twist on top of this with proof‑of‑reserves (PoR). Its system aggregates user balances into a Merkle tree, then lets each user verify that their account is included in the total liabilities represented by the Merkle root. Building on that, Binance integrated zk‑SNARKs so it can prove—without revealing individual balances—that all included accounts have non‑negative balances and that aggregate user assets do not exceed on‑chain reserves.

That combination of regulated‑style audits plus open‑source, zero‑knowledge proofs is exactly the kind of transparency stack regulators say they want but traditional finance can’t yet deliver at scale.

FDUSD vs USD1: case studies in “next‑gen” stablecoins

So what does a “policy‑aligned” stablecoin actually look like in practice? Two of the clearest examples on Binance right now are FDUSD and USD1.

FDUSD, issued by First Digital Labs in partnership with First Digital Trust in Hong Kong, is a 1:1 USD‑pegged stablecoin backed by cash and equivalent assets like U.S. Treasury bills and bank deposits, held in segregated trust accounts. It lives on multiple chains—Ethereum, BNB Chain, Solana, Sui and others—and has become a default quote asset and collateral token across many Binance spot and derivatives markets.

Structurally, FDUSD is tailored to sit comfortably inside Hong Kong’s fiat‑referenced stablecoin regime and, by extension, plays nicely with Singapore’s Single‑Currency Stablecoin standards thanks to its G10 USD peg and fully reserved design. For Asia‑centric funds, OTC desks, and exchanges, that makes FDUSD an obvious “house dollar” for cross‑exchange settlement and on‑chain collateral.

USD1 takes aim at a different target: the post‑GENIUS U.S. landscape. The coin is issued by BitGo Trust Company on behalf of World Liberty Financial and is fully backed by short‑term U.S. Treasuries and cash equivalents, with public reserve reports and third‑party audits. It’s explicitly marketed as an institutional‑grade, regulation‑friendly payment stablecoin—exactly the profile U.S. lawmakers had in mind when drafting the GENIUS Act.

Binance hasn’t treated USD1 as “just another listing.” It rolled out zero‑fee USD1 trading pairs against BTC, ETH, BNB and SOL for mid‑ to high‑tier VIPs, set up zero‑fee conversion between USD1 and majors like USDT and USDC, and started migrating all internal BUSD‑pegged collateral to USD1 at 1:1. This effectively retires BUSD within Binance’s systems and slots USD1 in as a core collateral and liquidity asset.

You can read this as a giant neon sign: Binance wants its “house stablecoins” to be the ones regulators are most likely to bless.

Why institutions suddenly care about stablecoins

It’s easy to forget how bad cross‑border payments are until you try sending money to a supplier over the weekend and realize your transfer is essentially stuck in airport security. Stablecoins attack exactly that problem—and the numbers show the idea is working.

Binance Research estimates that stablecoins processed about 33 trillion dollars in transfer volume in 2025, compared to roughly 14 trillion on Visa’s network, and still beat Visa after filtering out MEV and internal flows. Fireblocks data shows that around 60% of surveyed banks now prioritize cross‑border payments and FX for their blockchain initiatives, with roughly half targeting real‑time settlement and about a third focusing on treasury optimization and collateral use cases.

On the front end, Binance Pay is a live demonstration of how this plays out in the wild. By late 2025, Binance reported that its merchant network had grown from about 12,000 merchants at the start of the year to over 20 million worldwide—a roughly 1,700× jump—covering Latin America, Africa, Europe, the Middle East, and Asia. More than 98% of B2C payments on Binance Pay in 2025 were settled in stablecoins like USDT, USDC, EURI, FDUSD and others, underscoring how quickly they’ve become the default medium of exchange in crypto‑native commerce.

From a user perspective, it feels simple: scan a QR, funds arrive instantly, and you don’t think about correspondent banks, cut‑off times, or FX spreads. Under the hood, what’s really happening is that stablecoins and platforms like Binance Pay are replacing a spaghetti bowl of legacy rails with a programmable, global settlement layer.

Binance’s stablecoin pivot as a policy read‑through

If you zoom out, Binance’s behavior is a useful tell for where the puck is headed. The exchange isn’t just listing the latest algo‑experiment; it’s re‑architecting its core infrastructure around fully reserved, policy‑aligned stablecoins.

It has embedded FDUSD as a key quote and collateral asset, leaning into its Hong Kong trust structure and Asia‑friendly regulatory profile.

It has aggressively promoted USD1 with zero‑fee trading pairs, 1:1 migration of BUSD‑pegged collateral, and prominent spot and margin integrations, signaling confidence in a U.S. Treasury‑backed, GENIUS‑compatible dollar token.

It continues to iterate on transparent PoR with Merkle trees and zk‑SNARKs, open‑sourcing tooling so users and even other exchanges can verify reserves without sacrificing privacy.

Through Binance Pay and related payment products, it is normalizing stablecoins as a day‑to‑day payment method across millions of merchants, not just as trading collateral.

Put differently: Binance is quietly aligning its incentives with the emerging rulebook. The stablecoins it’s pushing to the center—FDUSD, USD1 and other fully backed, audited tokens—are the ones most likely to be white‑listed for banks, fintechs, and corporates once the dust settles on regulation.

2030: stablecoins as the invisible settlement layer

What does this look like by 2030 if current trends hold?

Start from where we are:

The U.S. now has a dedicated payment‑stablecoin statute in the GENIUS Act.

The EU has MiCA’s ART/EMT framework.

Singapore, Hong Kong, and Japan all run detailed licensing, reserve, and redemption rules that assume stablecoins will be used in real‑world payments, not just trading.

Visa has launched multi‑chain stablecoin settlement on Ethereum, Solana, Avalanche and Stellar, processing billions in annual transactions using on‑chain tokens under the hood.

Stablecoins already move more raw value than Visa and are a core focus area for banks looking at cross‑border FX and real‑time settlement.

Project that forward and a plausible 2030 picture emerges:

Regulated dollar, euro, yen, SGD, and CNH stablecoins—issued by banks or in partnership with regulated trusts—become the default settlement asset for cross‑border invoices, trade finance, and B2B payments, even when the end user never sees a wallet address.

Payment giants, banks, and fintechs treat public and permissioned blockchains as shared settlement backbones, while user experiences stay abstracted behind familiar apps and cards.

Exchanges like Binance function as ultra‑liquid FX and collateral hubs for these tokens, with PoR‑verified reserves and tight integration into both DeFi and institutional platforms.

In that world, arguing about whether stablecoins are “real money” will feel as dated as arguing about whether email is “real communication.” The more interesting question will be: which stablecoins sit at the core of global trade, and which platforms became the liquidity engines behind them?

Judging by how aggressively Binance is leaning into fully backed, regulation‑ready stablecoins like FDUSD and USD1—and how seriously it takes transparency and payments infrastructure—it intends to be one of those engines.

And if regulators get this right, most people won’t even notice the shift. They’ll just notice that paying a supplier in another country feels as quick and cheap as sending a DM.