The next wave of crypto adoption won't look like a trading desk in Manhattan. It'll look like a tuk-tuk driver in Phnom Penh, a freelancer in Lagos, and a café owner in Buenos Aires — all using one app to do what their banks never could.

Over 1.4 billion adults worldwide don't have a bank account. Not because they don't want one. Not because they lack ambition or assets. But because the system was never designed for them — too many forms, too few branches, too many fees, and currencies so unstable that saving in them feels like pouring water into sand.

Meanwhile, they have smartphones. They have mobile data. And increasingly, they have Binance.

What began as a crypto trading exchange has, almost quietly, evolved into something far more interesting: a full-stack financial operating system for the parts of the world that traditional finance forgot. P2P markets, stablecoin savings, mobile money on-ramps, cross-border payments, and merchant checkout — all in one app, all accessible without a credit score or a trip to a bank branch.

This isn't just a product story. It's an infrastructure story. And it's playing out right now, in cities like Phnom Penh, Lagos, and Buenos Aires.

The Problem with "Just Get a Bank Account"

If you've ever lived in a country with a stable currency, low inflation, and a functional banking system, it's easy to underestimate how much of your daily financial life depends on infrastructure you've never had to think about.

You swipe a card. Money moves. You send a wire. It arrives in a day or two, maybe three. You open a savings account. The bank doesn't charge you just for existing.

Now imagine none of that works reliably.

In Nigeria, the naira has lost the majority of its purchasing power over the past several years, driven by persistent inflation and restrictive FX controls that make accessing physical US dollars legally difficult. In Argentina, annual inflation exceeded 200% in 2023, and capital controls have long limited how much of their own money citizens can convert into harder currencies. In Cambodia, roughly 70% of the population remains unbanked, even as smartphone penetration races ahead — and remittances from overseas workers account for around 6% of the country's GDP.

These aren't edge cases. These are hundreds of millions of people for whom the gap between "needing financial services" and "having access to financial services" has been measured not in features, but in years of economic exclusion.

Crypto didn't create this problem. But it turns out it's uniquely positioned to solve it.

The Binance Product Stack, Mapped to Real Barriers

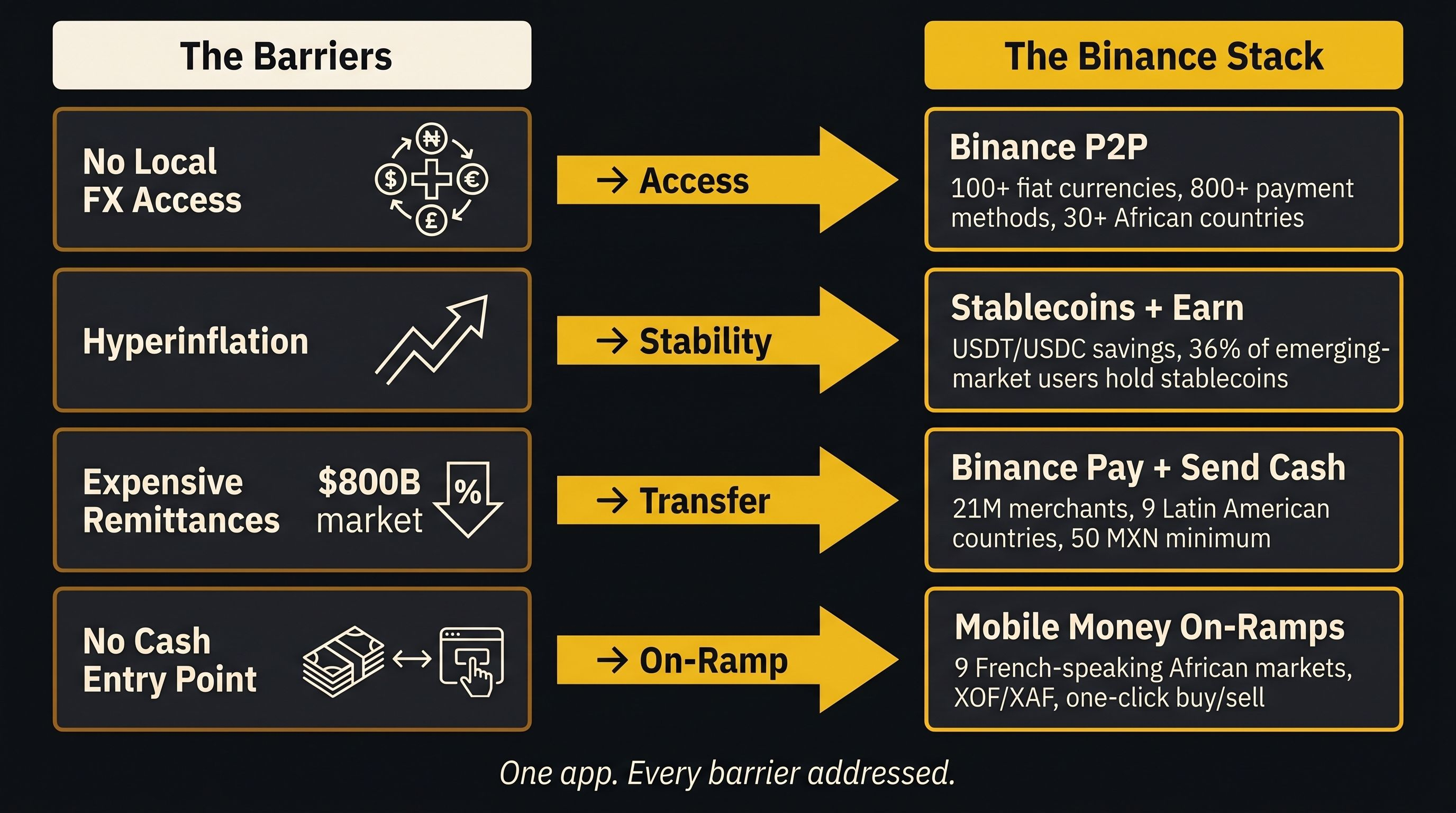

What makes Binance's approach compelling isn't any single product. It's how the whole stack lines up against the actual barriers that keep people locked out of the financial system.

Barrier #1: No Local FX Access → Binance P2P

Binance P2P lets users buy and sell crypto directly from each other using over 100 fiat currencies and more than 800 payment methods — including bank transfers, mobile wallets, and mobile money services. In Africa alone, the platform supports local currency trading across 30+ countries, plugging into mobile money rails like MTN Money, Orange Money, Moov Money, and Tigo Money.

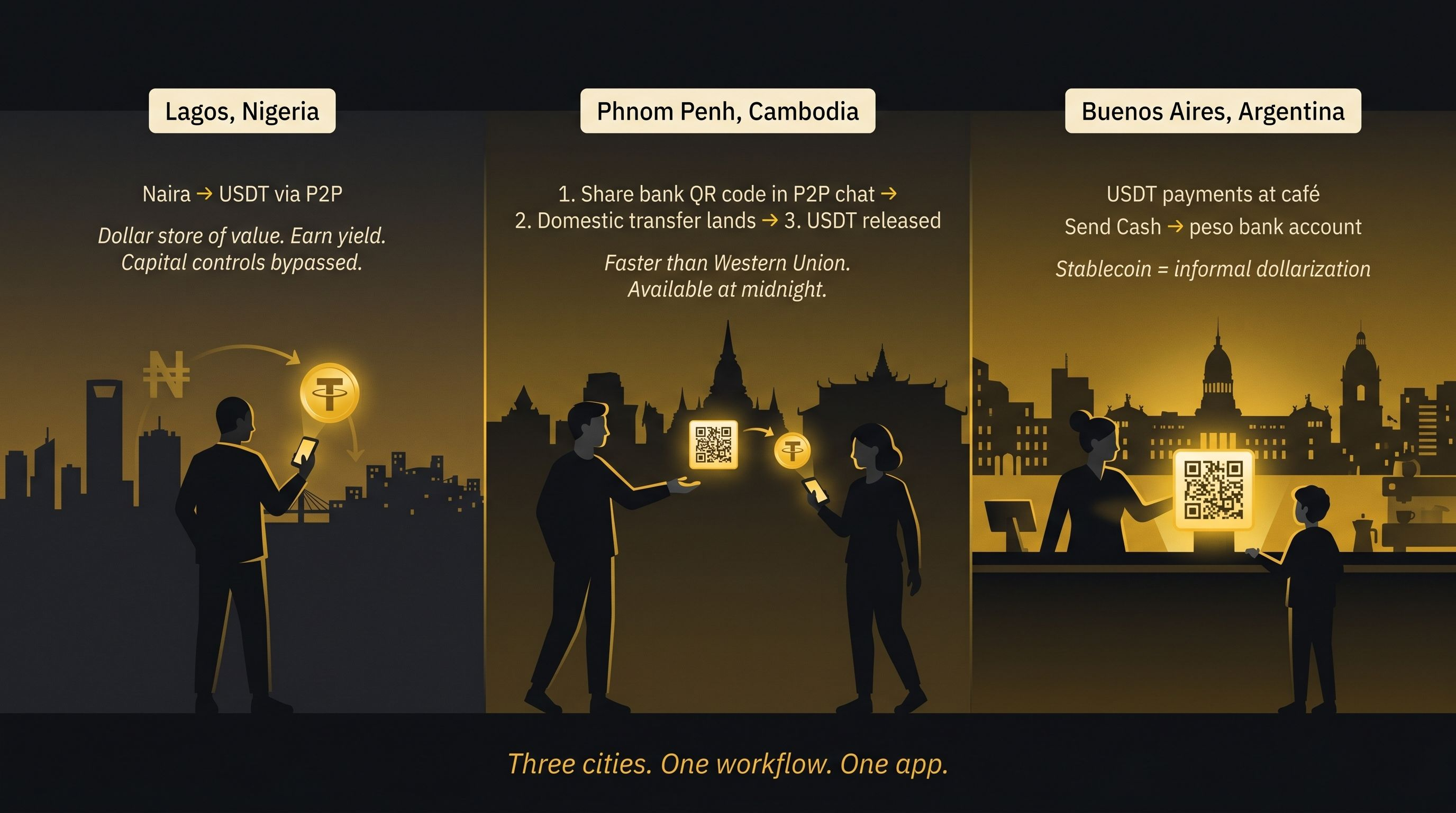

In Cambodia, there's a dedicated "Bank Transfer (Cambodia)" corridor on Binance P2P. The mechanics are elegantly simple: a buyer shares their local bank QR code in the P2P chat, a domestic transfer lands in their account, and only then does the USDT get released. For a worker in Phnom Penh receiving money from a relative abroad, that workflow — crypto sent overseas, sold via P2P into a local bank account in minutes — is a direct replacement for a remittance counter charging 5–8% for the privilege of a three-day wait.

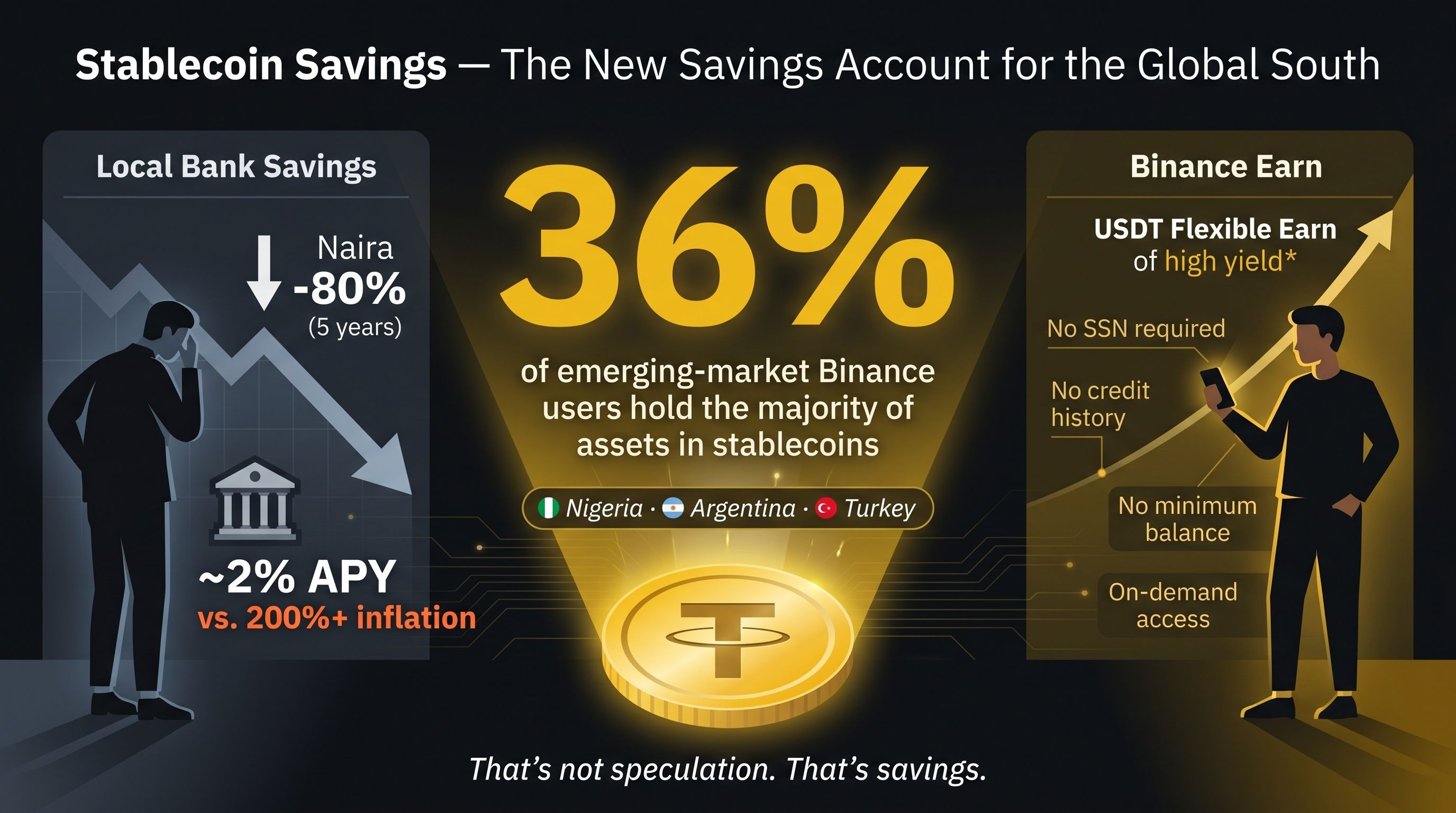

Barrier #2: Hyperinflation and Currency Collapse → Stablecoins + Earn

When your local currency is losing value faster than your savings account can earn interest, the most logical financial move is to get out of that currency as quickly as possible. That used to mean standing in line at a bureau de change. Now it means buying USDT on Binance.

Stablecoin data shows that users in Nigeria, Argentina, and Turkey — three of the world's most inflation-battered economies — are disproportionately represented among those holding large stablecoin balances. On Binance, over 36% of emerging-market users keep at least half their total portfolio in stablecoins. That's not speculation. That's savings.

And those savings can work harder on Binance than they ever could at a local bank: Binance's flexible and fixed-term Earn products let users put idle USDT or USDC to work with transparent, on-demand yields — the equivalent of a high-yield savings account, accessible without a SSN, a credit history, or a minimum balance requirement.

Barrier #3: Expensive Cross-Border Remittances → Binance Pay + Send Cash

The global remittance market processes over $800 billion a year, and traditional operators like Western Union or SWIFT still capture enormous margins on the transfer. Binance is building around them.

Binance Pay has now exceeded 21 million global merchants. Beyond peer-to-peer crypto transfers, the "Send Cash" product lets users in nine Latin American countries — Argentina, Colombia, Honduras, Guatemala, Costa Rica, Panama, Mexico, the Dominican Republic, and Paraguay — send funds via Binance Pay directly to local bank accounts, using licensed transfer processors to bridge the last mile into traditional rails. A separate Money Transfer product targets remittance corridors like Mexico, with minimum transfers as low as 50 MXN.

For a Honduran freelancer paid in USDT for online work, "Send Cash" means converting and landing pesos directly into their local bank without visiting a third-party service. For a Buenos Aires café owner, it means settling a cross-border payment without navigating the Argentine blue-dollar system.

Barrier #4: No Entry Point for Local Cash → Mobile Money On-Ramps

Even the best crypto product fails if users can't fund it. Binance's Africa push addresses this head-on: a one-click buy/sell feature lets users in nine French-speaking African markets fund their accounts directly from mobile-money balances in XOF or XAF — no bank card, no wire, just a few taps connected to the same mobile wallet they already use for everything else.

This is the kind of seemingly small design decision that determines whether a product actually gets used. It meets users not where Western financial infrastructure is, but where West African infrastructure actually is.

Country Close-Ups: Three Stories, One Pattern

Nigeria: The Parallel FX Window

In Nigeria, Binance P2P has become so central to how people access dollar liquidity that the government took notice. In early 2024, Nigerian regulators pressured Binance to implement a naira/USDT price cap on its P2P platform — a direct acknowledgment that P2P crypto markets had become a meaningful price-discovery mechanism for the naira itself.

Think about what that says: a crypto platform's peer-to-peer trading pairs had become significant enough to the local FX market that a central bank had to issue guidance about them. That is not the behavior of a gambling app. That is the behavior of financial infrastructure.

For Nigerian users, the appeal is straightforward: buy USDT as a dollar-equivalent store of value when naira pressure is high, earn yield in Binance's Earn products, transact across borders without hitting capital controls, and convert back when needed. The entire workflow — formerly requiring either a black market FX dealer or privileged access to a Nigerian bank's FX allocation — now runs from a phone.

Cambodia: The Remittance Bypass

Cambodia's economy runs on dollar-adjacent flows. Overseas workers send billions home; garment factories pay in mixed currencies; tourism creates FX demand across the country. The formal banking system serves only a minority of residents, but mobile phones are everywhere.

Binance signed an MOU with Cambodia's securities regulator (SERC) to help build a digital-asset legal framework — signaling a long-term institutional presence, not just a product listing. On the user side, Cambodian traders on local forums describe using P2P methodically: wait for the bank transfer confirmation, check the sender ID, then release the crypto. What sounds like caution is actually a refined workflow developed by a community that has figured out how to use a global financial tool in a local context.

The result is a de facto remittance network, running on Binance P2P, denominated in USDT, and settled through Cambodian bank accounts — faster than Western Union, cheaper than bank wires, and available at midnight when no money-transfer shop is open.

Argentina: Dollar Demand, Digitally Filled

Argentina doesn't need much introduction as a monetary cautionary tale. After years of triple-digit inflation and serial currency crises, Argentinians have become arguably the world's most financially sophisticated retail investors by necessity — because not hedging is financial suicide.

Today, Buenos Aires has a growing ecosystem of merchants accepting USDT directly — cafés, shops, and service providers who would rather settle in digital dollars than watch peso revenues evaporate overnight. Binance's stablecoin holdings are natural instruments here: hold USDT in Earn, spend it via Binance Pay at compliant merchants, or convert via Send Cash into peso-denominated bank accounts for expenses that still require local currency.

Where formal dollar accounts are restricted by capital controls, stablecoins on Binance have quietly become Argentina's de facto informal dollarization layer — accessible, liquid, and increasingly mainstream.

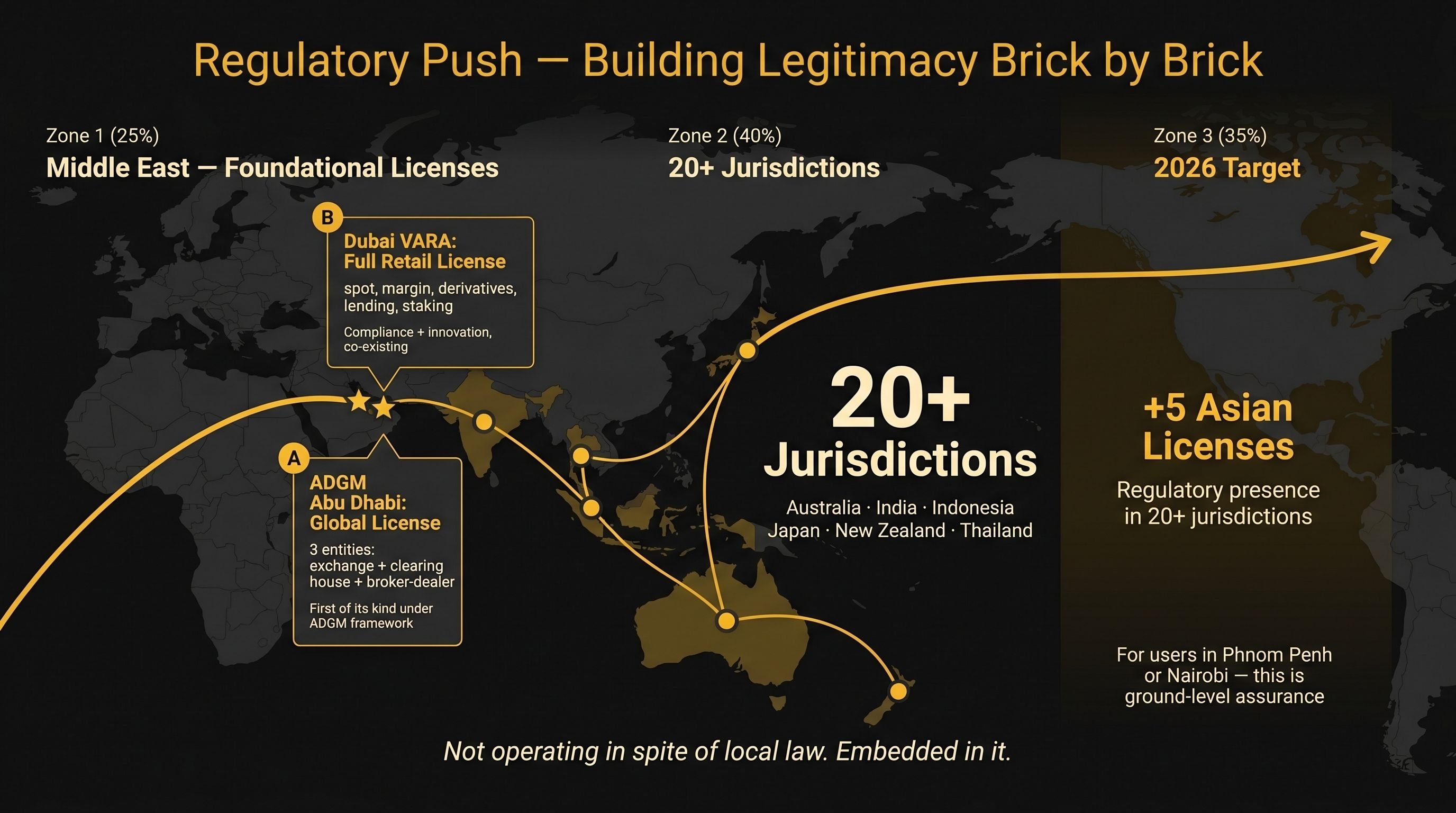

Building Legitimacy Brick by Brick: The Regulatory Push

There's a version of this story where Binance remains a grey-area app, tolerated but never trusted by local regulators. That's the version Binance is actively working to avoid.

In Abu Dhabi's Global Market (ADGM), Binance secured full authorization from the Financial Services Regulatory Authority to operate three licensed entities — an exchange, a clearing house, and a broker-dealer — effectively mirroring the architecture of traditional regulated market infrastructure. It marked the first time a crypto exchange received a "global license" of that structure under ADGM's framework.

In Dubai, Binance FZE received a full VASP license from the Virtual Assets Regulatory Authority (VARA), upgrading from a provisional license and gaining the right to serve retail clients with spot, margin, derivatives, lending, and staking products. Executives framed this as a signal to the world that full regulatory compliance and product innovation could co-exist.

Across the Asia-Pacific, Binance already holds approvals in Australia, India, Indonesia, Japan, New Zealand, and Thailand, and has publicly committed to targeting five additional Asian licenses in 2026 — aiming for a regulated presence in over 20 jurisdictions.

For users in Phnom Penh or Nairobi, these licenses matter not as legal abstractions but as ground-level assurance: the rail they're depending on is increasingly embedded in local financial law, not operating in spite of it.

The Together Initiative: $400M as Ecosystem Anchor

In October 2025, following a period of extreme market volatility that triggered record liquidations across futures and margin platforms globally, Binance launched the "Together Initiative" — a 400 million dollar recovery program designed to rebuild market confidence and protect affected users.

The plan had two components: 300 million in token vouchers and USDC distributed to eligible users who suffered forced liquidation losses above a defined threshold during a specific volatility window, and 100 million in low-interest loans extended to institutional partners and liquidity providers to help stabilize ecosystem infrastructure.

The significance for emerging markets is indirect but real. When 77% of your user base comes from developing economies, and many of those users rely on the platform as a primary financial tool rather than a supplementary trading account, protecting the ecosystem from liquidity crises isn't just good investor relations — it's a form of financial consumer protection for people who have no fallback.

The Bigger Picture: 77% and Counting

By 2026, Binance's own data says 77% of its users come from emerging markets. That number carries enormous weight.

It means the platform's center of gravity has shifted. The marginal Binance user is not a DeFi native in San Francisco or a derivatives trader in Seoul. They're a first-generation crypto user in a city like Kampala, Ho Chi Minh City, or Medellín — someone for whom "financial inclusion" isn't an ESG talking point but a lived gap in their daily economic life.

Among that base, 83% use more than one Binance product. More than a third hold the majority of their assets in stablecoins. They're not chasing 10x returns — they're building the digital equivalent of a wallet, a savings account, and a remittance service all in one.

That is the market Binance is quietly, methodically serving. And it's a market with hundreds of millions of people who have never had a financial product designed for them before.

The Next 200 Million Won't Come from Wall Street

There's a seductive narrative about crypto's future that revolves around institutional adoption: BlackRock ETFs, tokenized treasuries, sovereign wealth funds dipping their toes into digital assets. And that story is real — it's happening, and it matters.

But the next 200 million crypto users won't come from any of that.

They'll come from Phnom Penh, where a garment worker uses Binance P2P to receive a transfer from her brother in South Korea — faster and cheaper than any bank. They'll come from Lagos, where a twenty-three-year-old developer holds USDT in Binance Earn because the naira has taught him not to trust paper savings. They'll come from Buenos Aires, where a café owner has a QR code on the counter for USDT payments because her peso register feels like it's denominated in a currency that's making up the rules as it goes.

These users are already here. They're already building their financial lives around the infrastructure Binance has spent the last several years quietly assembling — local currency on-ramps, P2P corridors, stablecoin yields, merchant payment rails, and regulatory approvals that make all of it legitimate.

Binance isn't just a trading platform with a big user count. In the Global South, it's becoming something closer to the financial operating system that traditional banks never got around to building — and for hundreds of millions of people, it might be the only one they ever need.