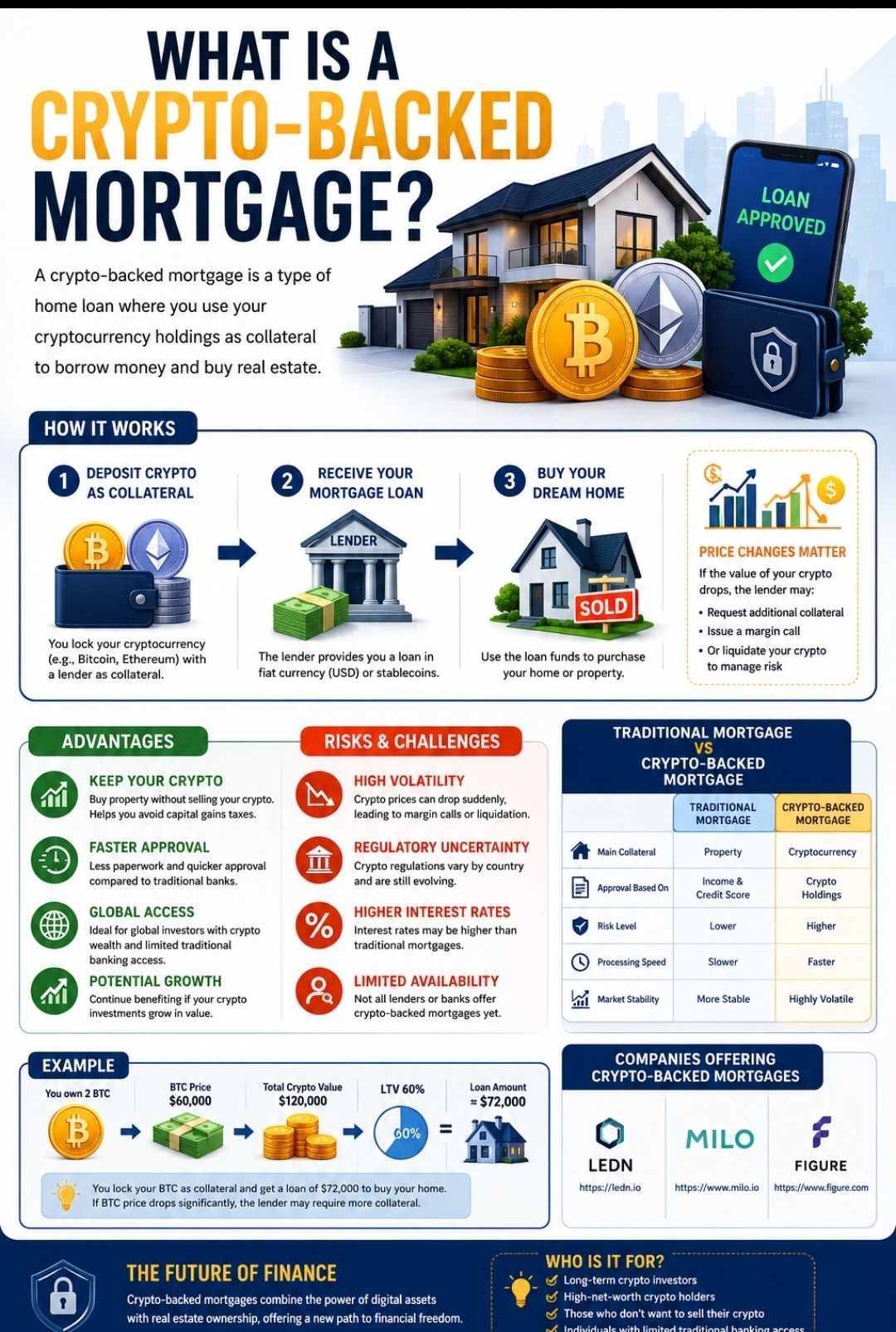

A crypto-backed mortgage is a type of home loan where a borrower uses cryptocurrency holdings—such as Bitcoin or Ethereum—as collateral to secure a mortgage for purchasing real estate.

Instead of relying mainly on income records, bank statements, or credit scores like traditional mortgages, crypto-backed mortgages focus heavily on the value of the borrower’s crypto assets.

---

How a Crypto-Backed Mortgage Works

1. The Borrower Pledges Crypto as Collateral

The borrower deposits cryptocurrency with a lender.

For example:

A borrower owns $100,000 worth of Bitcoin.

The lender may offer a loan based on a Loan-to-Value (LTV) ratio of 50%–70%.

This means the borrower could receive a mortgage loan between $50,000 and $70,000.

---

2. The Lender Provides the Mortgage

The lender gives the borrower money in fiat currency (such as USD) or sometimes in stablecoins.

The borrower then uses those funds to purchase a home or property.

---

3. Crypto Prices Affect the Loan

Cryptocurrency prices are highly volatile.

If the value of the pledged crypto drops significantly:

the lender may request additional collateral,

issue a margin call,

or liquidate some of the crypto assets to reduce risk.

This makes crypto-backed mortgages riskier than traditional home loans.

---

Advantages of Crypto-Backed Mortgages

✅ Keep Your Crypto Investments

Borrowers do not need to sell their cryptocurrency to buy property.

This may help avoid triggering capital gains taxes in some countries.

✅ Faster Loan Approval

Crypto lenders may offer quicker approval processes compared to traditional banks because there is less paperwork.

✅ Access for Global Investors

People who have significant crypto wealth but limited traditional banking access may still qualify for financing.

✅ Portfolio Growth Potential

Borrowers can continue benefiting if their crypto assets increase in value while still owning real estate.

---

Risks and Challenges

⚠️ High Volatility

Crypto markets can change rapidly.

A major price drop could force borrowers to provide more collateral or risk liquidation.

⚠️ Regulatory Uncertainty

Crypto regulations differ across countries and are still evolving.

⚠️ Higher Interest Rates

Some crypto-backed mortgages may charge higher interest rates than traditional mortgages.

⚠️ Limited Availability

Not all banks or lenders offer crypto-backed mortgage services.

---

Traditional Mortgage vs Crypto-Backed Mortgage

Feature Traditional Mortgage Crypto-Backed Mortgage

Main Collateral Property Cryptocurrency

Approval Based On Income & Credit Score Crypto Holdings

Risk Level Lower Higher

Processing Speed Slower Faster

Market Stability More Stable Highly Volatile

---

Example

Suppose:

You own 2 BTC.

Each BTC is worth $60,000.

Total crypto value = $120,000.

If a lender offers a 60% LTV ratio:

You may qualify for a loan of around $72,000.

You keep ownership exposure to your Bitcoin while using it as security for the mortgage.

However, if Bitcoin’s value drops sharply, the lender may require more collateral.

---

Companies Offering Crypto-Backed Mortgages

Some companies involved in this sector include:

Ledn

Milo

Figure Technology Solutions

---

Conclusion

A crypto-backed mortgage is an innovative financing method that allows people to use cryptocurrency assets as collateral for home loans. It combines digital assets with traditional real estate financing, offering flexibility for crypto investors.

However, because cryptocurrency prices can fluctuate dramatically, borrowers must carefully understand the risks before choosing this type of mortgage.