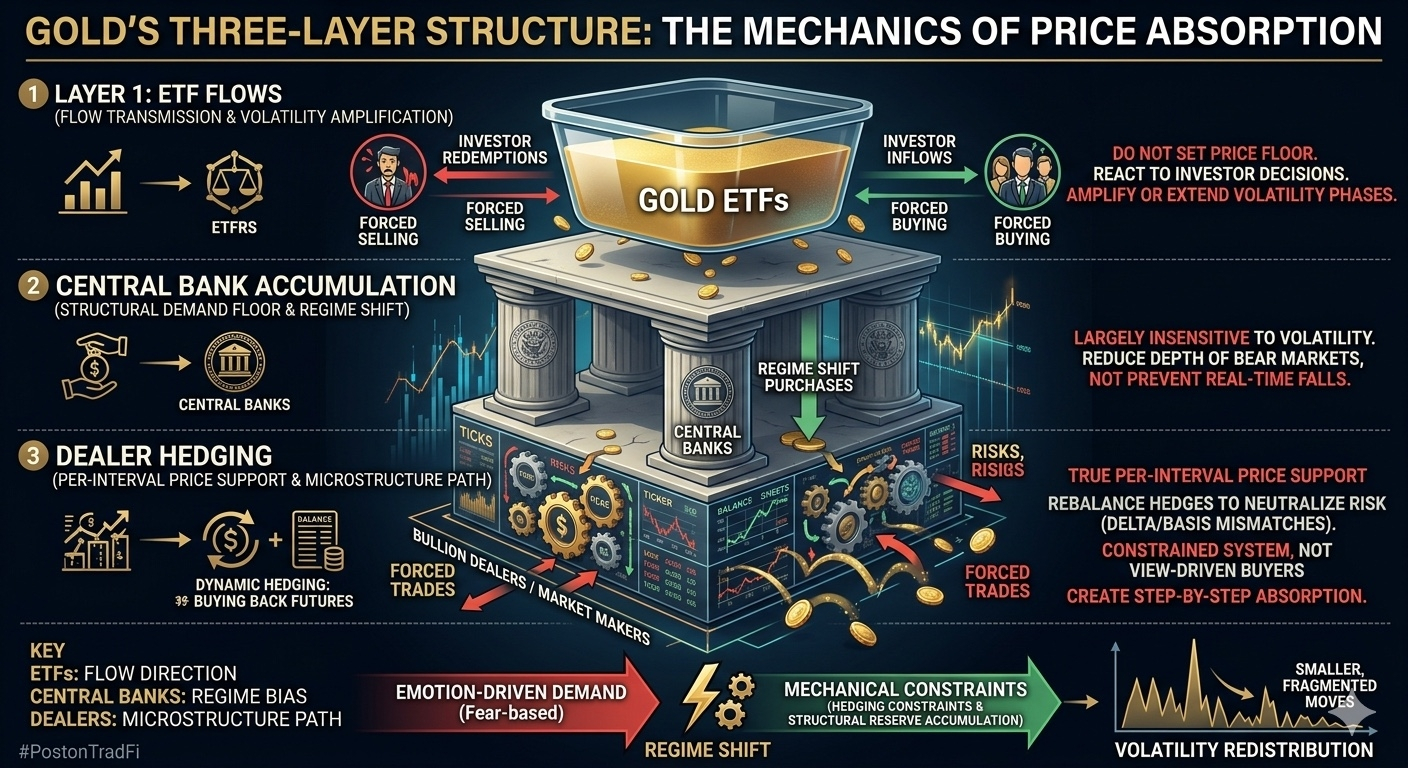

When speculative flows in gold begin to fade, the key question is no longer “who is buying,” but rather “what mechanism prevents prices from falling too sharply during each liquidity shock.” In the current regime, gold is no longer shaped by a single dominant demand force, but by a three-layer structure with clearly separated roles: ETF flows, central bank accumulation, and dealer hedging. However, if we narrow the focus to micro-level price action, only one layer actually generates immediate price support the market-making and hedging system of bullion dealers.

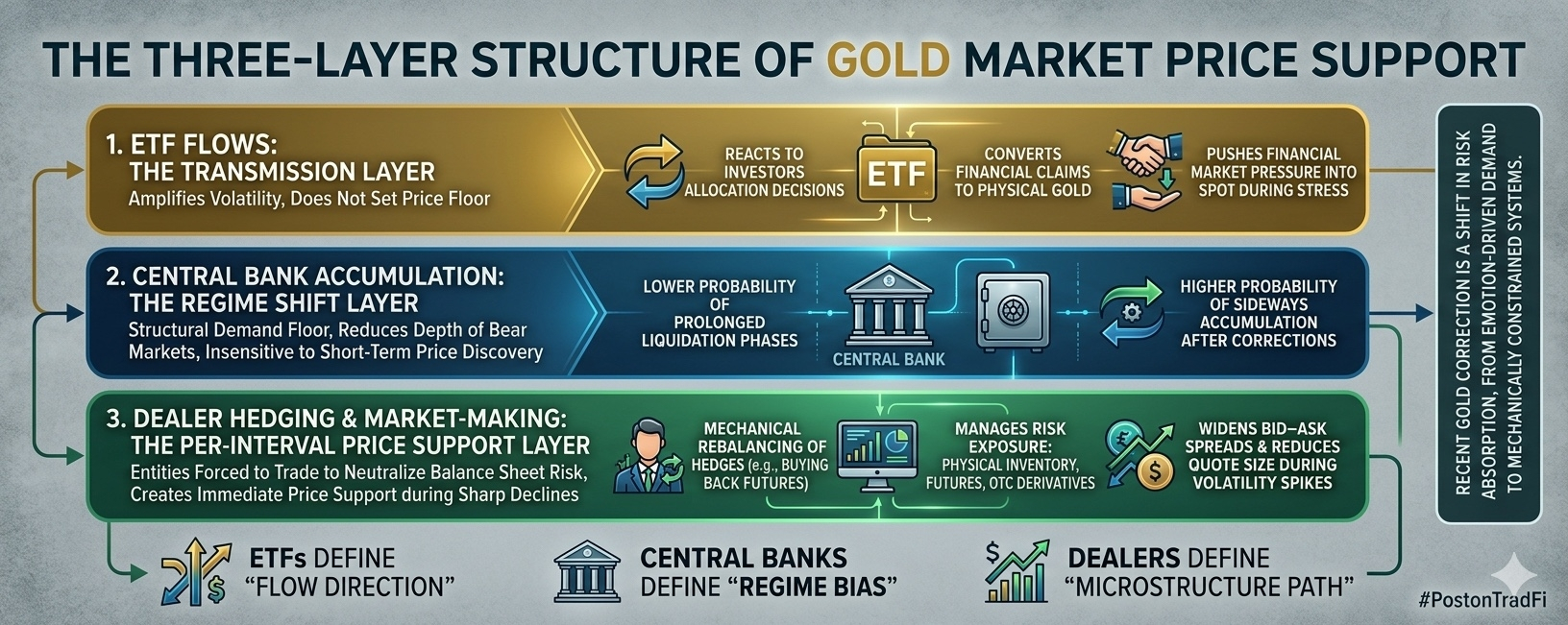

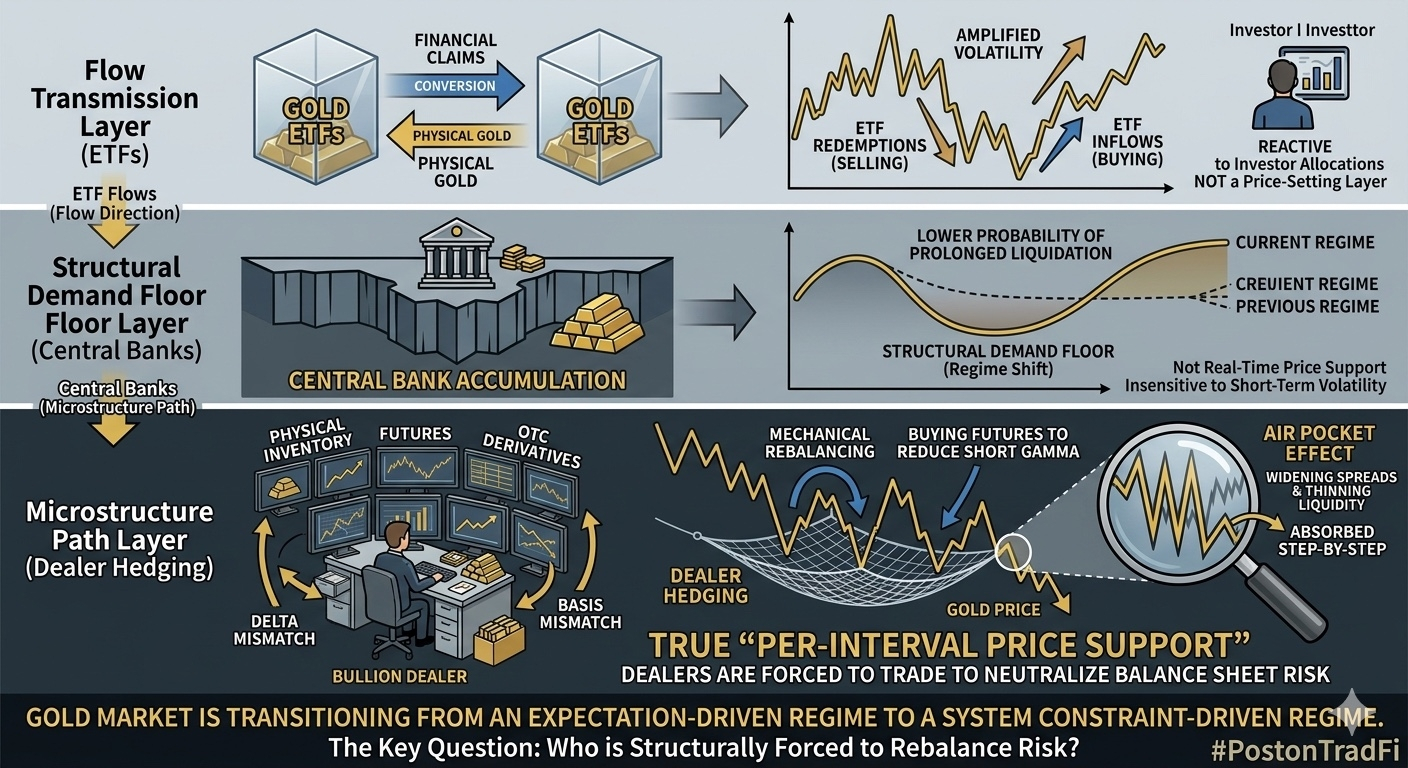

ETFs operate as a flow transmission layer, not a price-setting layer. Mechanically, gold ETFs simply convert between two states: financial claims and physical gold. When investors redeem, ETFs are forced to sell gold to maintain NAV balance; when inflows occur, they must buy. The key point, however, is that ETFs do not determine timing. They react to investors’ allocation decisions. As a result, ETFs do not create a price floor; they merely amplify or extend volatility phases depending on the speed of inflows or outflows. During stress periods, ETFs can even act as a transmission channel, pushing financial-market pressure directly into the spot market rather than absorbing it.

Central banks operate at a completely different layer. They do not participate in short-term price discovery and are largely insensitive to volatility. Their gold purchases are better described as regime shifts rather than trading activity. This creates a form of “structural demand floor,” though not in a technical market sense. It does not prevent prices from falling during sell-offs, but it alters the distribution of downturns: lower probability of prolonged liquidation phases and higher probability of sideways accumulation after corrections. In other words, central banks do not support price in real time; they reduce the depth of bear markets.

The most important layer lies in dealer hedging and market-making within the gold derivatives and OTC ecosystem. This is where true “per-interval price support” is formed. When gold prices drop sharply, dealers must simultaneously manage three risk exposures: physical inventory, futures positions, and OTC derivatives exposure. If they are structurally short through derivatives (a common feature of liquidity provision), sharp price declines create delta and basis mismatches across spot, futures, and the lease market.

In such conditions, rather than expressing a market view, dealers are forced to rebalance their hedges. This leads to a mechanical behavior: buying futures back to reduce short gamma exposure or to correct inventory imbalances. More importantly, during volatility spikes, dealers tend to widen bid–ask spreads and reduce quote size, which effectively thins liquidity at the exact moment selling pressure increases. The result is an “air pocket” effect, where prices do not collapse in a straight line but are absorbed step-by-step through hedging adjustments.

The key point is this: dealers are not “buyers of gold.” They are entities forced to trade in order to neutralize balance sheet risk. It is this constraint that produces what the market perceives as “price support,” though in reality it is simply a dynamic equilibrium within a derivatives-driven system.

When these three layers are combined, the structure becomes clear: ETFs transmit flows and can amplify volatility; central banks define the long-term boundary of the demand regime; but dealer hedging determines the actual shape of each downside move. In other words, ETFs define “flow direction,” central banks define “regime bias,” and dealers define “microstructure path.”

From this perspective, the recent correction in gold does not signal trend exhaustion. Instead, it reflects a shift in the way risk is absorbed: from emotion-driven demand (fear-based buyers) to mechanically constrained systems (hedging constraints and structural reserve accumulation). This reduces the probability of liquidation-driven crashes, but does not eliminate volatility it simply redistributes it into smaller, more fragmented moves absorbed across different liquidity layers.

Therefore, when viewed correctly, the gold market is not lacking buyers. It is transitioning from a regime where bids are driven by expectations to one where bids are driven by system constraints. And in such a market, the key question is no longer who believes in gold, but who is structurally forced to rebalance risk whenever prices deviate from equilibrium.