A year ago, they moved like one trade. Today, they're telling completely different stories.

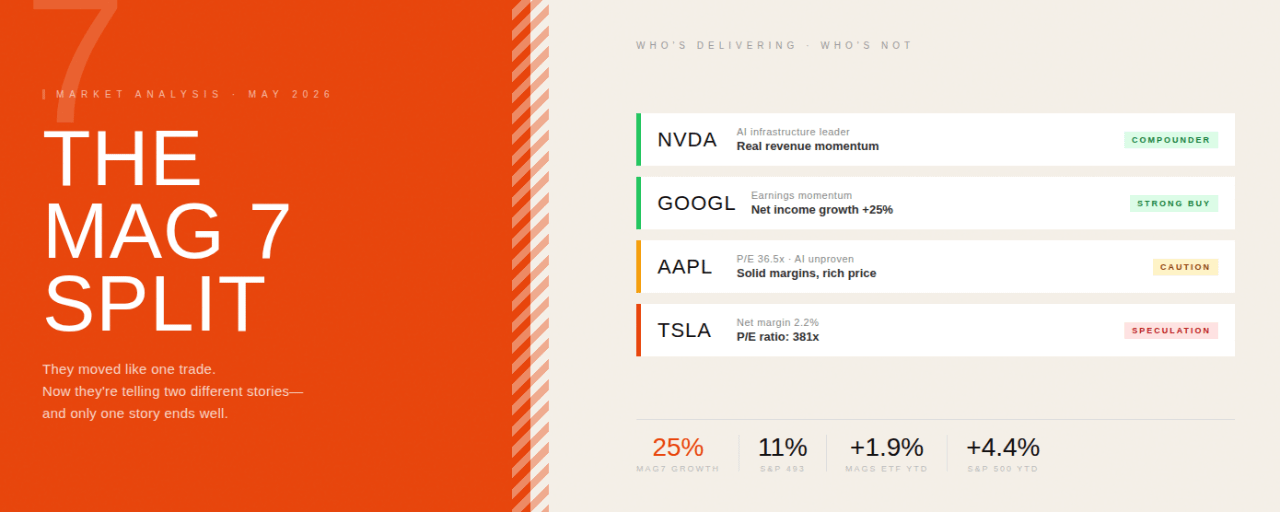

The MAGS ETF is up just 1.9% year-to-date. The S&P 500? Up 4.4%. The group that once carried the whole market is now being carried by only part of itself.

The AI Compounders Are Pulling Ahead

Earnings growth estimates for the Mag 7 just got revised up to 18% for 2026, from 14% after the tariff selloff. But the gains are concentrated:

Mag 7 net income growth: 25% in 2026 vs 11% for the other 493 S&P companies

Nvidia, Alphabet, and Microsoft are driving almost all of that gap

Strip out tech entirely and S&P 500 earnings growth drops to just 7.7%

The Laggards Are Flashing Warning Signs

Tesla:

Operating margin: 4.2%

Net margin: 2.2%

P/E ratio: 381x

52-week range: $273 to $499, currently at $417

Apple:

Operating margin: 32.3% (solid fundamentals)

P/E ratio: 36.5x

52-week range: $193 to $303, currently at $305

AI narrative still unproven at the product level

The Macro Backdrop Is Accelerating the Split

Rising oil prices and volatile tech mean market gains are shifting toward a broader set of players, not just the mega-caps. Rotation is already happening.

What This Means Practically

The "buy the basket" trade that worked from 2023 to 2025 is over. You have to pick now:

Nvidia and Alphabet: earnings momentum backed by real AI revenue

Microsoft: deep enterprise relationships, steady compounder

Tesla: a speculation on robotaxi timelines, not a car company valuation

Apple: premium brand priced like a hypergrowth AI stock

The divergence is not a red flag. It is the market repricing based on who is actually delivering.

Which of the 7 do you still own with conviction? Drop it below.