I remember watching a token listing a while back where the narrative was perfect and the behavior was wrong. Strong AI story, exchange access, clean branding, decent early liquidity. Yet the chart behaved like traders were renting attention rather than buying into a system. That stuck with me. Over time I started noticing the same pattern across infrastructure tokens. Markets get excited about what a network says it can accumulate, but recurring value usually comes from what the system forces participants to repeatedly do.

That is partly why my view on OpenLedger shifted.

At first I looked at it the obvious way. AI attribution infrastructure. Contributors provide data, models consume it, usage gets tracked, rewards get distributed, $OPEN coordinates incentives. Reasonable thesis. The market understands that kind of story because crypto likes tokenized marketplaces.

But what caught my attention was a different question. What happens when valuable AI memory becomes a liability instead of an asset?

That sounds philosophical until you think operationally.

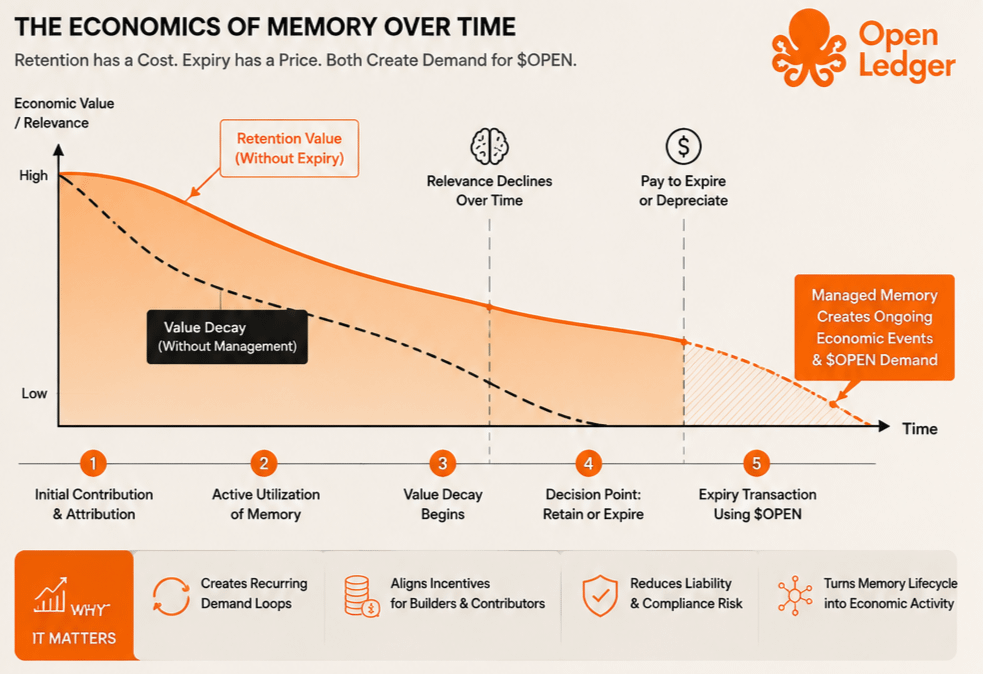

Most AI narratives assume memory is always positive. More data, more context, better outputs. In practice, memory creates obligations. Retaining training influence, preserving contributor claims, keeping historical attribution trails, dealing with disputes over provenance, handling changing permissions, maybe even responding to regulatory pressure around data retention. Intelligence does not just inherit knowledge. It inherits baggage.

This is where the OpenLedger framing starts to look less like attribution infrastructure and more like something stranger.

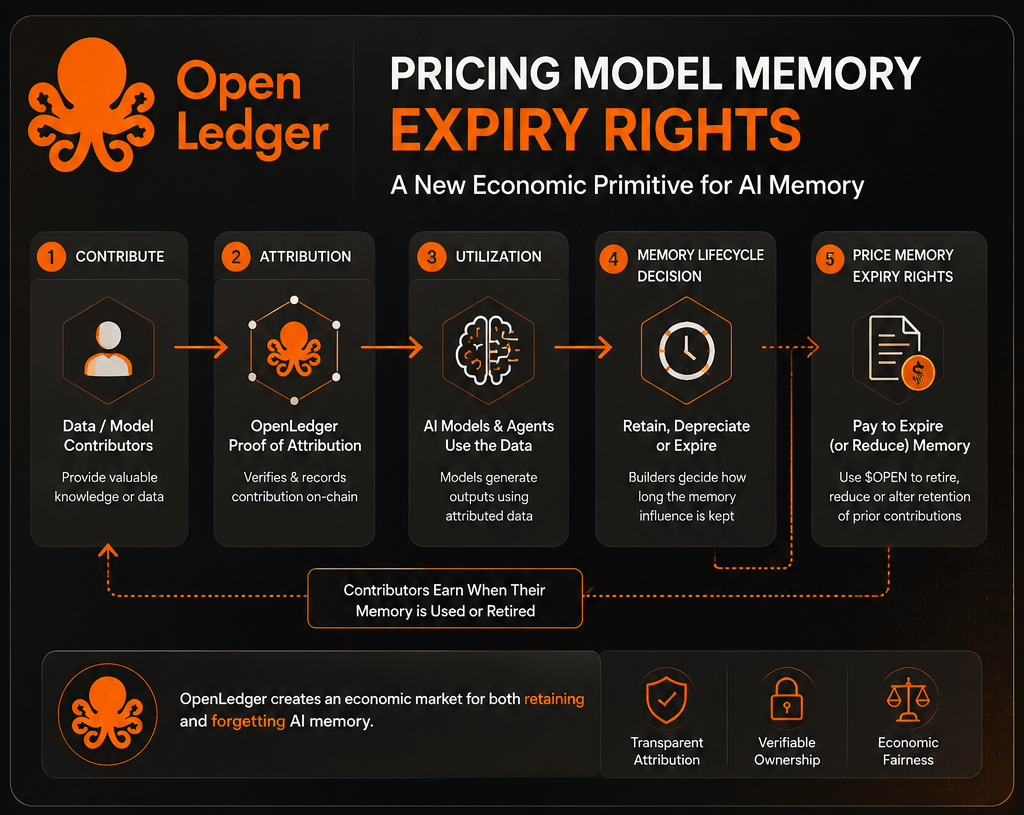

Potentially, a market around controlled forgetting.

Not forgetting in the technical “model weights instantly deleted” sense. That is messier. I mean economically managed memory expiry. Systems where retaining influence carries cost, while removing or depreciating old contribution also becomes part of network economics.

Crypto traders should care because this changes the demand model.

A pure attribution network can suffer from a familiar retention problem. A contributor uploads something useful, gets compensated, and leaves. Builders consume what they need. Activity spikes during onboarding, then fades unless fresh usage keeps entering. That looks fine in a deck. It trades badly if recurring demand never forms.

Infrastructure tokens die there all the time.

The more interesting version is where memory itself becomes an active economic object.

Imagine an AI builder sourcing proprietary domain data through a datanet. Attribution is tracked. Contributors expect compensation if their influence persists. Fine. But six months later, that retained influence may be commercially inconvenient, legally risky, outdated, or expensive. Suddenly keeping old memory is not free.

Now $OPEN starts looking less like access fuel and more like economic arbitration around retention.

That loop matters.

Because recurring token demand rarely comes from initial participation. It comes from operational maintenance. Gas works because transactions repeat. Staking works when security assumptions persist. Infrastructure tokens survive when users return because the system creates ongoing obligations, not one-time excitement.

If OpenLedger ever evolves toward pricing retention rights, depreciation rights, or controlled attribution expiry, that is structurally more interesting than simple contribution rewards.

Still, traders need to separate concept from evidence.

Token economics matter here. If a project carries heavy fully diluted valuation pressure relative to circulating supply, narrative strength can temporarily hide dilution, but only temporarily. Infrastructure names often list with enough liquidity to attract speculation while future unlocks quietly overhang price discovery. I have seen that movie enough times.

So the practical question is not whether the idea sounds intelligent.

It is whether actual token sinks exist.

Who buys $Open repeatedly?

Builders paying for access is one answer, but that can be cyclical. Contributors staking for participation is another, though that often becomes reflexive incentive farming if verification is weak. Validators or operators bonding capital can help if network security genuinely depends on it. Better if fees are denominated in economic activity rather than narrative speculation.

The dangerous version is spoofed participation.

Low-quality data contributors farming incentives. Artificial attribution loops. AI outputs claiming dependence on weak inputs. Token rewards leaking to actors creating volume without value. That destroys infrastructure credibility quickly because verification becomes expensive and trust degrades faster than adoption grows.

And attribution itself is not simple.

What percentage of a model response came from one contributor versus background statistical inference? How do disputes resolve? What happens when contributors disagree? If proving influence becomes ambiguous, the economic layer gets noisy. Traders should be skeptical whenever the reward logic depends on measurement that looks cleaner in diagrams than in production.

There is also coordination friction.

If builders can source equivalent data off-network more cheaply, the token layer becomes optional. Optional utility rarely produces durable demand. If compliance-heavy enterprise users need cleaner guarantees than decentralized attribution can realistically provide, adoption narrows.

This is where the “memory expiry rights” thesis becomes useful as an analytical framework, even if OpenLedger never explicitly markets itself that way.

Because it asks a harder question than attribution alone.

Who pays not just to remember, but to stop remembering?

That is a stronger recurring economic loop if real.

As a trader, I would watch behavior, not storytelling. Sustained fee generation matters more than social engagement. Bonded participation matters more than headline partnerships. If contributors are staying active without emissions doing all the work, that matters. If service buyers repeatedly return for economically necessary operations rather than one-time experimentation, that matters more.

I would also watch supply absorption closely. Unlock schedules can ruin elegant infrastructure theses if demand arrives slower than token issuance. A good architecture trapped inside bad market structure still trades badly.

And liquidity tells its own truth. If exchange volume remains speculative while on-network usage stays thin, the market is likely trading abstraction, not infrastructure.

That does not mean the thesis is wrong.

Just early. Or incomplete.

I think traders make a recurring mistake with AI infrastructure tokens. They price the intelligence narrative first and the maintenance economy second. Usually it should be reversed.

Anyone can build a story around attribution. The harder question is whether the network creates recurring economic obligations that participants cannot easily avoid.

That is where real token demand tends to live.

So if you are watching $OPEN, I would spend less time asking whether AI needs attribution.

And more time asking whether AI memory, once priced, eventually becomes something the market must also learn how to forget.