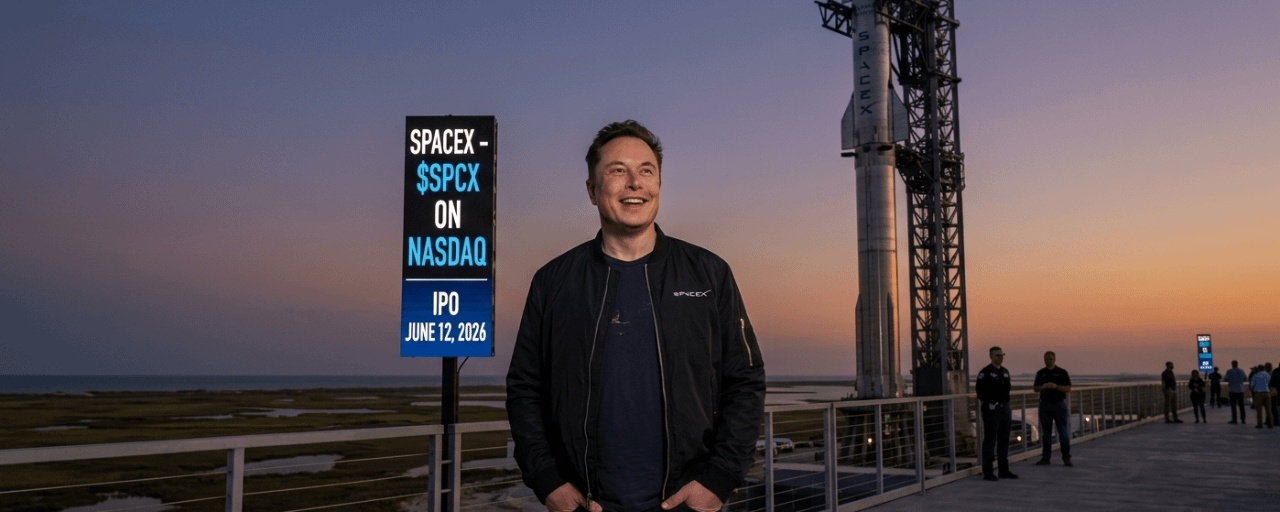

On June 12, 2026, the global financial landscape is set to experience a seismic shift. Wall Street is bracing for the arrival of SpaceX on the Nasdaq under the ticker $SPCX. Armed with an unprecedented target valuation approaching $1.75 trillion and looking to raise a staggering $75 billion in a single offering, this transaction moves past standard market milestones straight into the history books.

To put it in perspective, when Saudi Aramco set the previous world record in 2019 by raising $29.4 billion, it was considered an untouchable high-water mark. SpaceX plans to more than double that in a single, audacious move. Should the listing clear this multi-trillion-dollar bar, Elon Musk will secure an unprecedented legacy as the first CEO to simultaneously command two separate, publicly traded trillion-dollar titans: Tesla and SpaceX.

But behind the historic headlines, a critical realization is settling over institutional trading desks: investors buying into $SPCX are not simply buying a rocket company. They are buying a highly integrated, multi-industry conglomerate divided into three starkly contrasting business segments.

Deconstructing the Triad: What Lies Inside $SPCX?

┌─────────────────────────────────────────────────────────┐ │ $SPCX │ │ Target: $1.75T Valuation │ └────────────────────────────┬────────────────────────────┘ │ ┌─────────────────────────┼─────────────────────────┐ ▼ ▼ ▼ ┌──────────────────┐ ┌──────────────────┐ ┌──────────────────┐ │ Space Launch │ │ Starlink │ │ xAI & X │ │ (Core Engine) │ │ (Cash Generator)│ │ (The AI Bet) │ └──────────────────┘ └──────────────────┘ └──────────────────┘

1. The Space Launch Business: The Vision & The Heavy Lifting

This is the foundational rock upon which the entire empire was constructed—encompassing the Falcon 9, Falcon Heavy, Dragon capsules, and lucrative aerospace contracts with NASA and the Department of Defense.

The Financials: This division generated a robust $4.09 billion in revenue for 2025.

The Catch: It registered an operating loss of $657 million.

The deficit is entirely structural. The next-generation Starship system has already aggressively swallowed more than $15 billion in raw development costs. While Starship represents the future of deep-space logistics and Mars colonization, it has yet to generate predictable, commercial revenue, meaning the core launch business is currently running hot on capital expenditure.

2. Starlink: The Economic Engine

If the launch business is the heart of the company’s vision, Starlink is the cash-flow engine that funds it. The low-Earth orbit satellite network has successfully transformed from a highly speculative telecom project into an absolute juggernaut.

The Financials: In 2025, Starlink brought in $11.39 billion in revenue—surging nearly 50% year-over-year. More impressively, its operating profit skyrocketed 120% to $4.42 billion.

Current Momentum: The velocity has only accelerated. In Q1 2026 alone, Starlink generated $3.26 billion, accounting for an overwhelming 69% of SpaceX's entire consolidated revenue.

Supported by 9,600 active satellites in orbit and a global subscriber base of 10.3 million users, Starlink represents a high-margin utility that, on a standalone basis, could comfortably anchor a massive premium valuation.

3. xAI and X: The Frontier Tech Amalgamation

The most complex and heavily debated component of the IPO stems from a massive structural shift. In February 2026, SpaceX executed a $250 billion merger with Elon Musk’s artificial intelligence venture, xAI—which had itself previously absorbed X (formerly Twitter), the social media platform acquired for $44 billion in 2022.

By pulling xAI and X into the corporate perimeter, SpaceX transformed from an aerospace corporation into a sprawling tech conglomerate. The operational scale of this unit is immense: the company poured $12.7 billion into artificial intelligence projects over the course of 2025. In Q1 2026, capital expenditures hit $10.1 billion, with a jaw-dropping $7.72 billion funneled straight into high-performance AI computational infrastructure. This level of infrastructure spending eclipses the annualized budgets of almost every pure-play AI startup in existence.

The Clash of Paradigms: The Bull vs. The Bear

The investment community is sharply divided on how to properly discount a business that operates simultaneously across deep space, global telecommunications, and frontier artificial intelligence.

The Bull Case: Absolute Vertical Integration

Optimistic investors argue that SpaceX is uniquely positioned to capture cross-sections of a combined addressable market valued at $28.5 trillion. The bedrock of the bull thesis is an unfair competitive advantage via total vertical integration: SpaceX builds the rockets, launches its own payloads, operates the world's largest satellite constellation, and builds its own data centers to process the information.

Furthermore, the company has teased a massive, long-term wildcard: orbital data centers. By aiming to deploy solar-powered, liquid-cooled supercomputing clusters directly into space by 2028, SpaceX hopes to bypass terrestrial energy grid limitations and radically lower the cooling costs associated with heavy AI workloads. While it sounds like science fiction, SpaceX is uniquely positioned to attempt it, given their routine, low-cost access to orbit.

The Bear Case: Staggering Cash Burn & Corporate Governance

Conversely, skeptics highlight that the consolidated entity recorded an overall net loss of $4.9 billion in 2025. At a $1.75 trillion valuation, public investors are being asked to pay an extreme multiple for operational execution that remains years away.

Signs of market maturity are also appearing. Starlink’s average revenue per user (ARPU) dropped from $99 per month in 2023 to $66 in Q1 2026. While the user base is growing globally, monetization per user is compressing as the service expands into lower-income emerging markets, all while localized competitive pressures begin to surface.

Finally, the corporate governance framework outlined in the S-1 prospectus is highly non-traditional. Elon Musk's executive compensation structure contains unorthodox milestones, including specific multi-trillion-dollar market cap targets and legal provisions tied directly to the establishment of a self-sustaining human colony on Mars. This introduces a variable that standard valuation models are simply not built to handle.

The Hidden Catalyst: Nasdaq’s Fast-Track Rule

A critical element of the IPO that remains under-analyzed by retail markets is Nasdaq’s Accelerated Inclusion Rule.

Under this framework, because of SpaceX’s sheer scale, $SPCX could automatically qualify for inclusion in the elite Nasdaq-100 index just 15 trading days after its public debut. The moment this milestone is crossed, passive investment vehicles and exchange-traded funds (ETFs) tracking the index will experience a structural mandate.

The Passive Inflow Inevitability: The premier Invesco QQQ ETF alone commands over $300 billion in assets under management. Within weeks of the IPO, index-tracking funds will be legally forced to buy billions of dollars worth of $SPCX to accurately match the index weighting—completely independent of whether their portfolio managers agree with the $1.75 trillion valuation.

This mechanical institutional buying pressure could trigger highly abnormal, upward price distortions during the initial weeks of public float, offering a unique liquidity window for early market participants.

Repricing the Cosmos: The Ripple Effect

The instant trading commences on June 12, the entire pure-play space and aerospace ecosystem will undergo an aggressive fundamental repricing. Public market valuations for independent players are already moving dynamically in anticipation of the $SPCX benchmark:

Space Sector Equities Recent Performance Benchmarks EchoStar Up 499% over the past 12 months Satellogic Up 407% Year-to-Date Planet Labs ($PL) Up 110% Year-to-Date Rocket Lab ($RKLB) Trading at elevated sector multiples

Public funds are rapidly scrambling to readjust their portfolios before the industry's ultimate gravity well enters the public domain. For current space asset holders, the incoming tide could represent either a rising tide that lifts all boats or an institutional landmine if capital drains out of smaller caps to feed the main event.

The Ultimate Question for Investors

SpaceX is an extraordinary, generation-defining enterprise; that reality is firmly established. However, disciplined market participants must separate the greatness of the company from the physics of the investment vehicle.

The core question hanging over June 12 is straightforward: Is this IPO priced to offer an attractive entry point for public capital, or is the market being asked to provide exit liquidity for early-stage venture investors who have already captured the steep part of the growth curve?

If Starlink scales efficiently to 100 million global nodes, Starship drives launch economics to an unprecedented sub-$100 per kilogram threshold, and the space-based AI infrastructure yields real margin expansion, a $1.75 trillion valuation may ultimately look cheap. But if the heavy capital expenditure of the AI infrastructure falters, or if orbital data centers prove economically unviable, public shareholders will bear the full brunt of the markdown. Combined with the reality that Musk will maintain airtight voting control via super-voting shares, investors must accept being along for the ride.

On June 12, 2026, the public markets will begin testing the exact boundary between brilliant engineering and capital market reality.