read through $OPEN's exchange listIng history again. same question keeps coming back.

multiple exchange listings signal broad accessibility. m0re venues. more liquidity. lower barriers for retail participation. the standard narrative around exchange listings is that more is better.

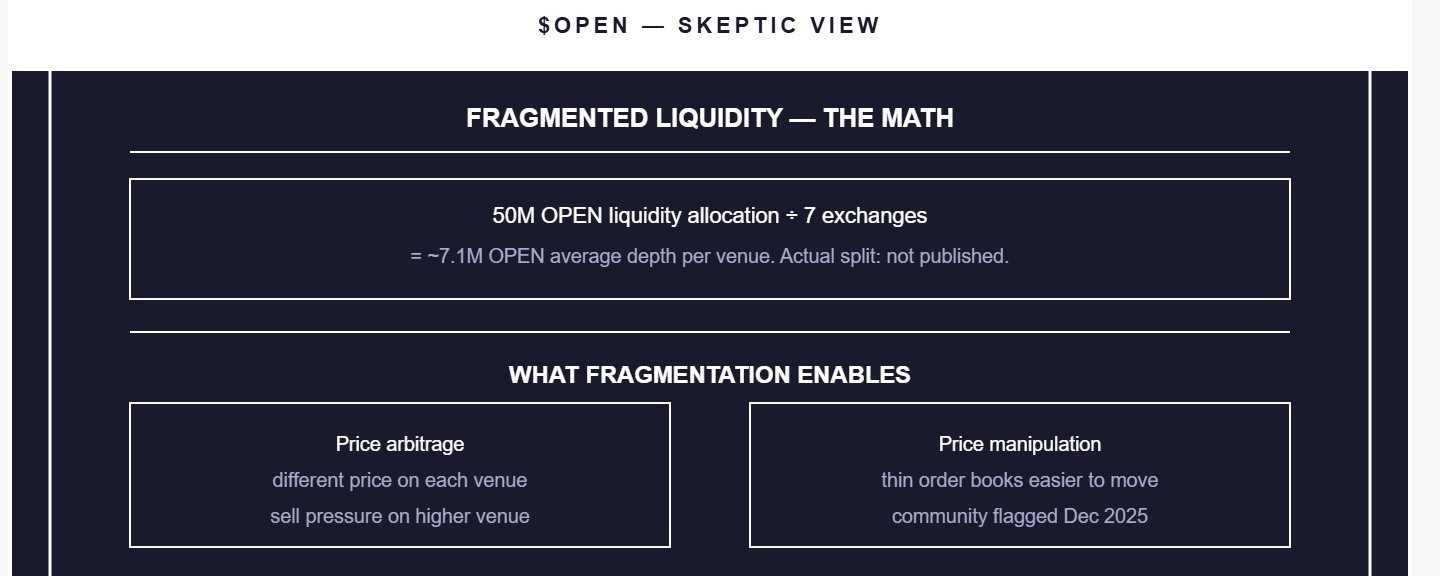

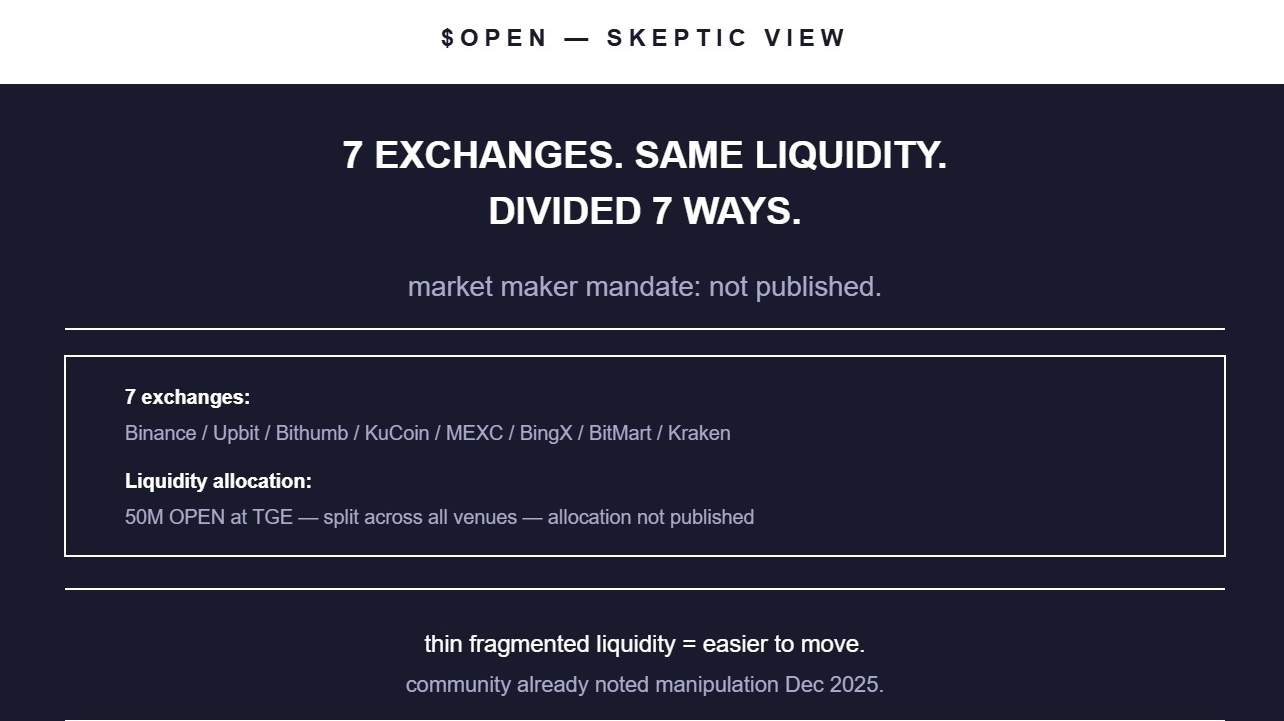

seven exchanges with separate order books means liquidity is fragmented across all of them. atoken with fragmented liquidity has a different effective price on each venue at any given moment. the spread between venues creates arbitrage opportunities traders buying 0n the cheaper venue and selling on the more expensive one.

arbitrage is not neutral for the token. it creates sell pressure on whatever venue is temporarily higher. it creates buy pressure on whatever venue is temporarily lower. for a token with 290 million circuLating supply and $60M market caP a relatively thin market fragmented liquidity means price discovery is noisier and more manipulable than a token with the same market cap on one or two deep venues.

the 5% liquidity allocation 50 million OPEN was unlocked at TGE to support market making across exchanges. that is 50 million tokens spread across sevEn exchanges and multiple trading pairs. the math on market depth per venue is not published. nobody has disclosed how the 50 million is allocated across venues 0r whether any dedicated market maker has a mandate to maintain tight spreads across all seven.

the December 2025 community comments about price manipulation become more legible in this context. thin fragmEnted liquidity is easier to move than deep concentrated liquidity. seven Order books is not seven times the liquidity. its the same liquidity divided seven ways.

watching published market maker mandate and spread commitments across exchanges whether liquidity concentrates to fewer venues over time onChain vs exchange volume ratio as an indicator of real vs wash trading.