And it could become a problem for every stock market in the world.

The Bank of Japan spent the last two years trying to unwind one of the biggest money printing programs in history through Quantitative Tightening.

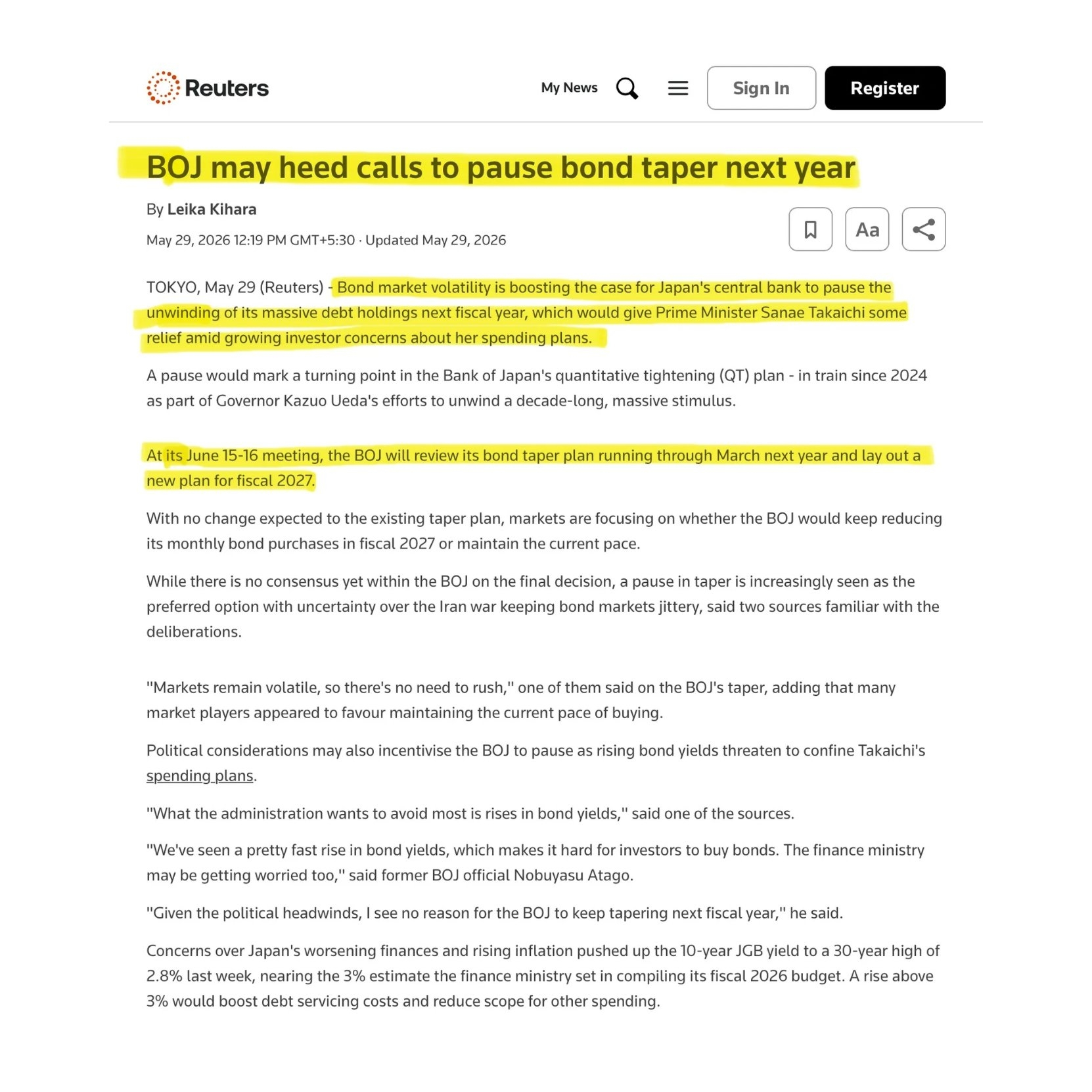

The goal was simple: reduce its massive bond holdings, normalize policy, and slowly return the bond market to private investors after years of central bank intervention.

Now that plan may be falling apart.

According to Reuters, BOJ officials are increasingly considering a pause to QT in 2027 as bond market volatility continues to rise.

This would be a major reversal for a central bank that has spent years trying to exit emergency-era policies.

The reason is the bond market itself.

Japan's 10-year government bond yield recently hit 2.8%, the highest level in nearly 30 years.

Long-dated bond yields have reached record highs, and investors are becoming increasingly concerned about Japan's debt burden and rising inflation.

This is becoming a serious problem because Japan has more than $8 trillion of government debt. The finance ministry built its entire 122.3 trillion yen budget assuming yields would not exceed 3%. Japan's debt servicing costs have already risen 10.8% this year to 31.3 trillion yen. Every move above 3% automatically wipes out spending room the government does not have.

At the same time, inflation is rising again.

For years Japan wanted inflation because the country was stuck in a low growth, low wage environment.

Now inflation is being driven by higher energy costs and imported inflation from the Iran conflict, which is a very different type of inflation and much harder to control. Japan has recorded above-target inflation for 45 consecutive months.

This leaves the BOJ trapped.

If it continues QT, bond yields could move even higher and put more pressure on government finances.

If it pauses QT, it risks showing that the bond market still depends on central bank support after more than a decade of intervention.

And this is where global markets come in.

Japan is the third largest economy in the world and the single largest foreign holder of US Treasuries. The BOJ currently owns 49% of all outstanding Japanese government bonds, 503 trillion yen out of a total 1,025.8 trillion yen market.

When Japanese bond yields rise, Japanese institutional investors stop buying US Treasuries and bring money home instead.

That reduces demand for US debt, pushes US yields higher, and tightens financial conditions for every market on earth that prices risk against the US 10-year rate.

But the bigger risk is the carry trade.

For years global investors borrowed money in Japan at near zero interest rates and invested those funds into higher yielding assets around the world US stocks, emerging market bonds, tech stocks, crypto. This trade worked as long as Japanese rates stayed low.

As the BOJ raises rates and Japanese yields rise, the cost of borrowing in yen increases. That forces carry trade investors to close their positions, selling the assets they bought and converting back to yen to repay their loans.

In August 2024 the BOJ raised rates by just 0.15%.

What followed was the single largest single day crash in the history of the Japanese stock market and a violent selloff across global equities, crypto, and emerging markets within 48 hours.

The BOJ is now expected to raise rates to 1% at its June 15-16 meeting. That is a significantly larger move than August 2024.

The carry trade built on decades of near zero Japanese rates is estimated at over $4 trillion globally.

That's why this should scare every investor in the world.

#Bitcoin #BTC #CryptoNews #MarketCrash #GlobalMarkets $BTC $ETH $LAB