The Fed's QT program ended in early December 2025 – how has the balance sheet changed? 📊

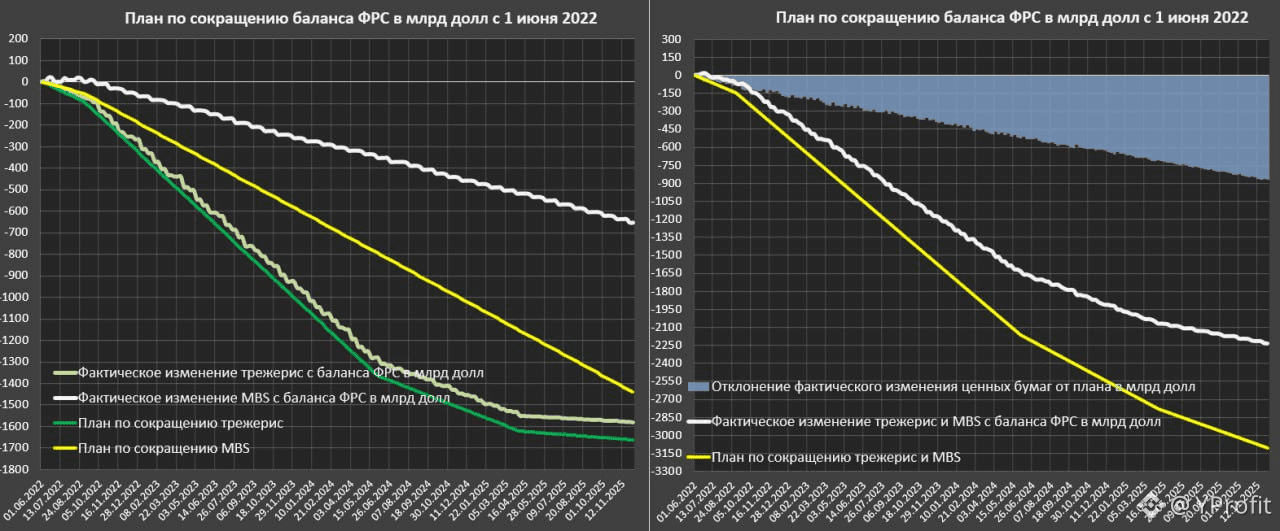

The actual volume of asset reduction on the balance sheet amounted to $2.23 trillion over 3.5 years (the program began on June 1, 2022) against a declared plan of $3.1 trillion (~72% completed).

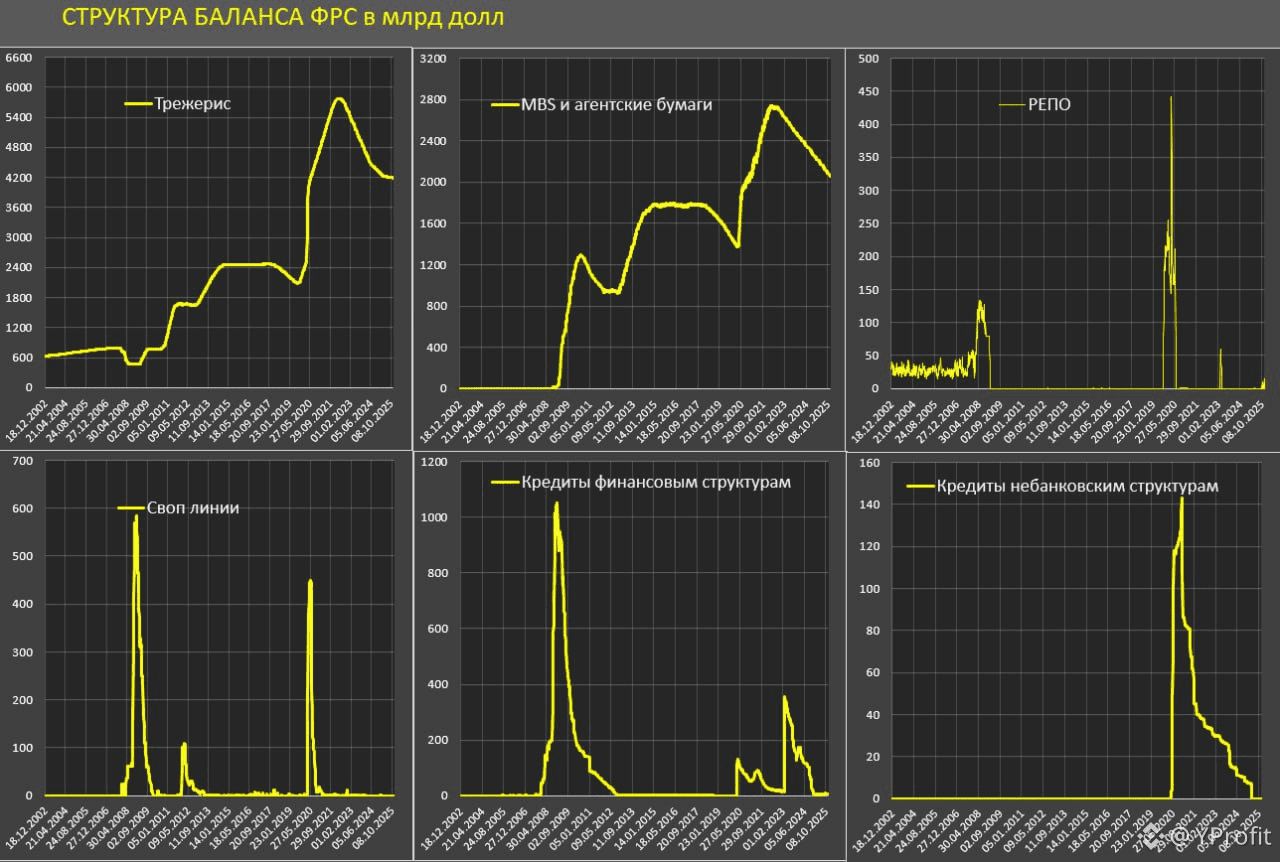

· Treasury securities were reduced by $1.58T against a plan of $1.66T (95.2% completed).

· MBS were reduced by only $0.653T against a plan of $1.44T (45.3% completed).

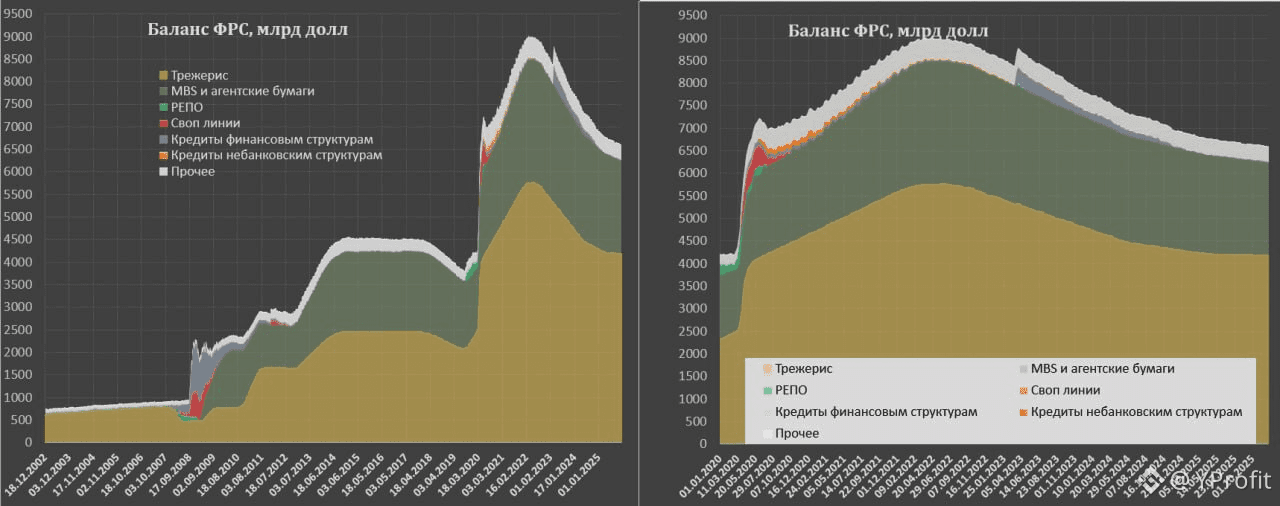

The total securities portfolio now stands at $6.24T (Treasuries – $4.19T + MBS – $2.06T), while the peak balance in history was $8.5T in April 2022.

The monetary frenzy of 2020-2021 led to an explosive balance sheet growth of $4.7T in just two years (from Mar '20 to Mar '22) from a level of $3.8T at the start of 2020. Over $2.3T was accumulated in Q2 2020 alone (the period of the most aggressive QE in history).

The 3.5-year balance sheet reduction removed less than half of the monetary madness phase. However, it has led to a "spreading out" of liquidity—the average annual increase over 6 years (2020-2025 inclusive) is about $415B per year, not $2.5T per year as during the era of monetary excess.

From Mar '20 to Mar '22, the net issuance of U.S. Treasury securities amounted to $6.4T. The Fed directly (through Treasury purchases) and indirectly (via MBS and other liquidity channels) monetized over 73% of the government debt issuance—an incredible concentration.

The combined monetary and fiscal frenzy, coupled with a critical delay in tightening monetary policy, played a fundamental role in forming the largest inflationary impulse in 45 years and accumulating imbalances at all levels (especially in asset markets through price distortion).

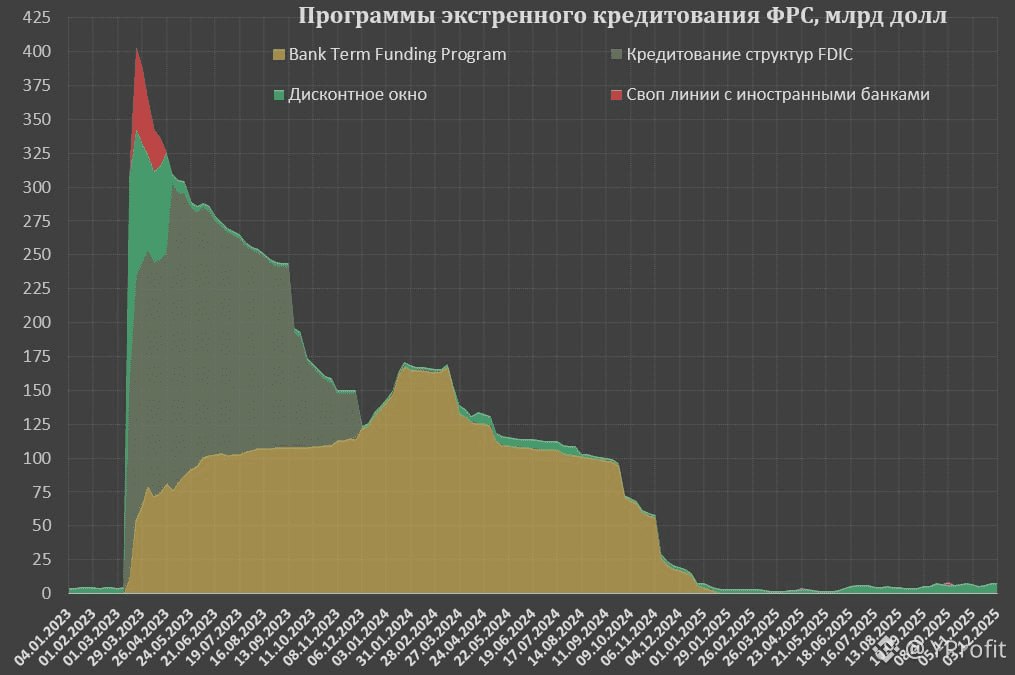

▪️ Emergency bank lending programs, launched in spring 2023 in response to the regional bank crisis, were almost completely wound down by January 2025 and have remained largely unchanged since.

▪️ Bank deposits (reserves) at the Fed are fluctuating around $2.8T—a level close to critical, where tension in the money market begins to form, putting upward pressure on the interest rate range.

Since late October, bank reserves have held at ~$2.88T, having fallen by nearly $0.5T since Aug '25. The relatively comfortable average level was $3.32T in Q3 '25, $3.36T in 2024, and $3.24T in 2023.

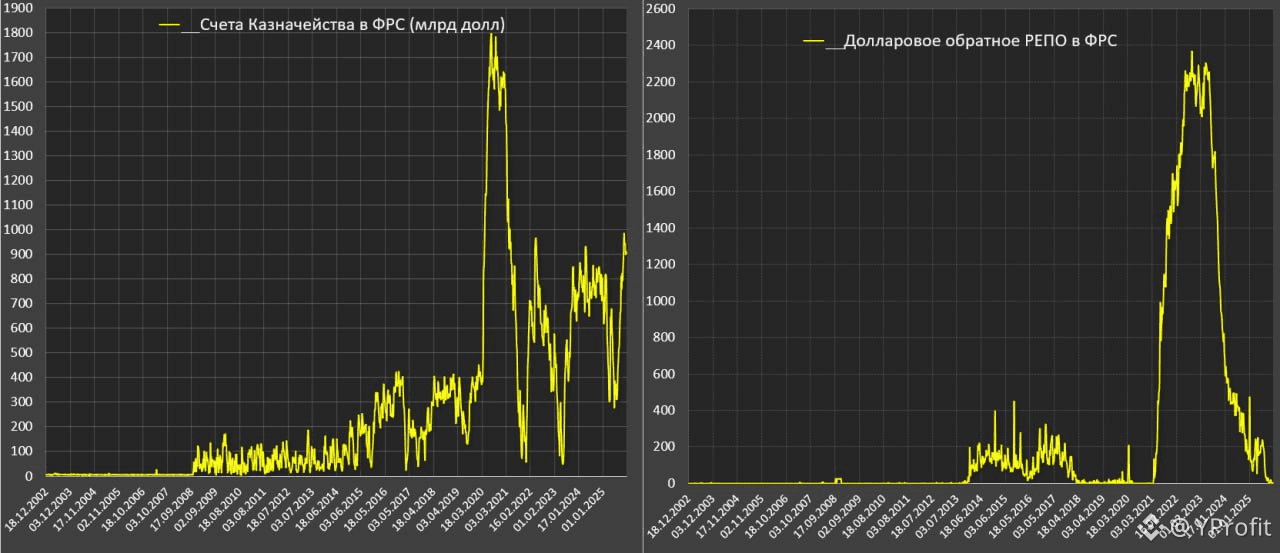

▪️ The U.S. Treasury's cash balance is at ~$0.9T, down from a peak of $1T in early November. Before the debt ceiling was suspended, it had fallen to $0.3T (a critical level that at best allows smoothing monthly volatility in income/expenditure distribution, but not smoothing borrowing cycles).

The minimum sustainable level for balancing the debt position is $0.7T (about one-third of the annual budget deficit or 4 months of government functioning).

Given that the Treasury's cash position has reached its target level, future borrowing plans will be formed according to the current need to cover the budget deficit.

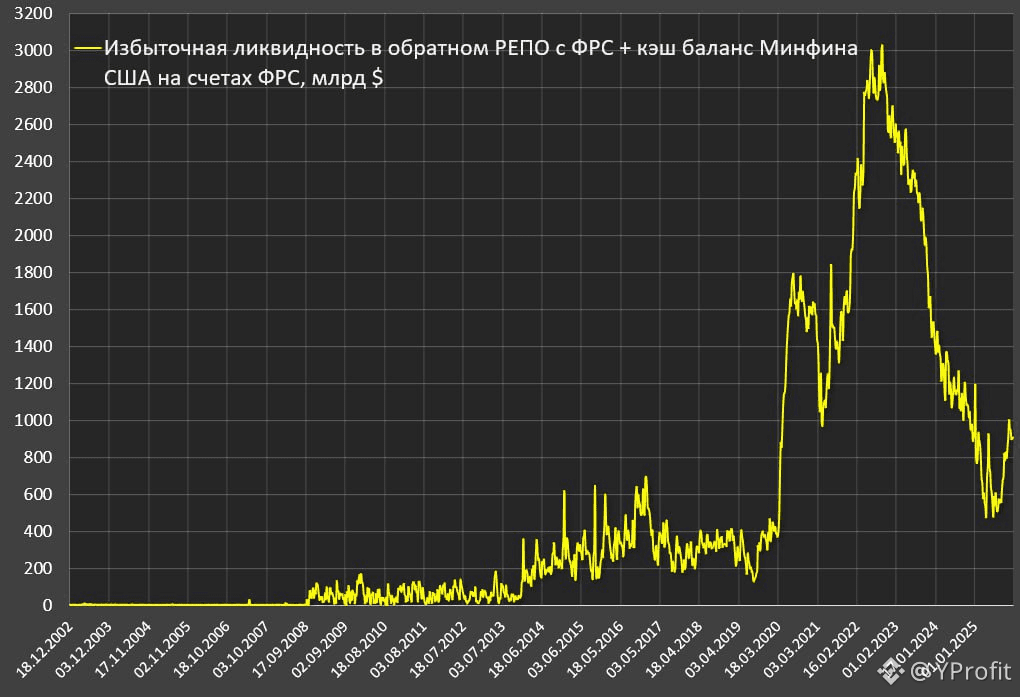

▪️ Reverse Repo (RRP) at the Fed dropped to zero by mid-August '25 (the 4-week average fell below $50B). Previously, in H1 '25, it averaged around $160B.

There is currently no significant pressure on the money market. The Fed's credit facilities are effectively deactivated, aside from local and irregular volatility within $10-14B from repo and discount window operations.

Considering the depleted buffer of excess liquidity from RRP and the reduction of bank reserves to $2.8T, the estimated liquidity deficit is assessed at $0.5-0.7T, but no clear signs of pressure have emerged yet.

Stopping QT is fair and reasonable (it could have been slowed down in the summer, as noted earlier this year). However, launching QE amid a record divergence of inflation from target and extreme financial market bubbles at this stage would be an act of vandalism and lawlessness.

A rate cut is unjustified. The fair interest rate, considering labor market issues, is at least 4.5%. ⚖️📉