$SKHYNIX just dropped a bombshell: South Korea’s memory giant wants to raise up to $29.4 billion through a Nasdaq ADR listing.

If it happens, we’re looking at one of the largest U.S. equity offerings in history. Bigger than most tech IPOs. Bigger than many SPACs.

This isn’t just “SK Hynix goes to Wall Street.” It’s a signal that AI memory chips are now front-and-center for U.S. investors. Here’s the full story, in plain words.

1. What SK Hynix Actually Announced

*The plan*: SK Hynix, the #2 memory maker globally behind Samsung, will list American Depositary Receipts on Nasdaq to raise up to $29.4B.

*ADR = American Depositary Receipt*: Think of it as a U.S. stock version of a foreign company. 1 ADR = X shares of SK Hynix Korea stock. U.S. investors can buy it in dollars, during U.S. hours, without opening a Korea brokerage account.

*Why now*: 3 goals, all tied to AI boom:

1. *Expand AI chip production*: Specifically High Bandwidth Memory - HBM. That’s the memory stacked next to Nvidia GPUs.

2. *Fund new semiconductor fabs*: Fabs cost $20B+ each now. TSMC, Intel, Micron all spending hundreds of billions. SK Hynix needs cash.

3. *Broaden investor base*: Right now SK Hynix mainly trades in Seoul. Nasdaq ADR = U.S. institutions, ETFs, retail can buy easily. More buyers = higher valuation.

2. Why $29.4B Matters: This Would Be Historic

For context:

- *Largest U.S. IPO ever*: Saudi Aramco at $25.6B, but that was in Riyadh. U.S. record is Meta at $16B in 2012.

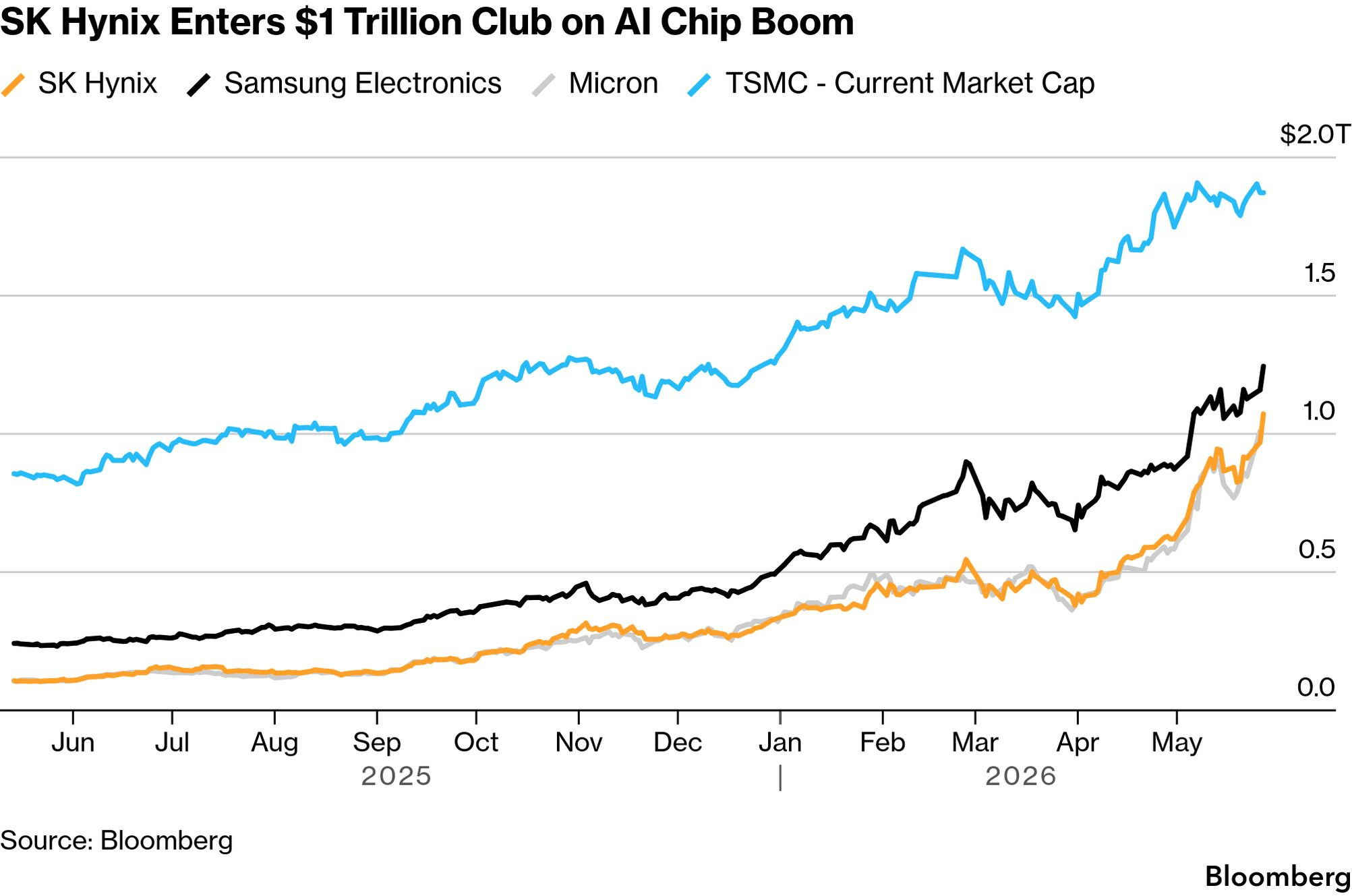

- *Micron market cap today*: ∼$1.2T. A $29.4B raise = ∼2.5% of that.

- *Nvidia raised $0 in equity last 3 years*: Because they didn’t need to. SK Hynix does, because building fabs is capital-heavy.

If SK Hynix pulls off $29B, it instantly becomes one of the most watched listings ever. Wall Street will call it the “AI memory IPO of the decade.”

3. The Real Story: HBM Demand Is Insane

SK Hynix isn’t raising money because it’s broke. It’s raising because demand is outpacing supply.

*What’s HBM and why it’s hot:*

Regular DRAM = memory in your laptop. HBM = memory stacked in 8-12 layers, sits right next to AI chips. Bandwidth is 10x higher. Without HBM, Nvidia’s H100/B200 GPUs can’t feed data fast enough.

*SK Hynix position*: They’re actually #1 in HBM market share today, ahead of Samsung and Micron. Nvidia’s CEO Jensen Huang said publicly that SK Hynix was first to ship HBM3 for AI. That endorsement = gold.

*Result*: HBM prices up 5x vs normal DRAM. Profit margins exploding. That’s why SK Hynix profits went vertical in 2024-2026, same as Micron’s 346% revenue jump.

But making HBM needs new factories, new equipment, new engineers. That costs tens of billions. Hence: Nasdaq ADR.

4. Why U.S. Investors Should Care

*1. Easier access = more demand*

Right now U.S. funds want SK Hynix exposure but buying Seoul stock is painful: currency conversion, time zones, custody issues. Nasdaq ADR removes friction. Same reason TSMC trades as TSM on NYSE and trades $20B/day.

More access = more index inclusion = more passive money flows in. S&P, Nasdaq ETFs will add it.

*2. Valuation re-rating*

Korean stocks often trade at discount vs U.S. peers due to “Korea discount” - governance, geopolitics fears. Listing on Nasdaq signals SK Hynix wants U.S. governance standards. U.S. investors pay higher multiples. Micron trades ∼50x earnings. SK Hynix Korea trades lower. ADR could close gap.

*3. Sector validation*

When a $29B deal hits market, every analyst covers it. Every fund manager has to answer “do you own SK Hynix?” That spotlight lifts whole sector: Micron, Samsung, ASML, Lam Research, Applied Materials. Rising tide.

5. Risks: $29B Isn’t Free Money

*Dilution*: New shares = existing SK Hynix shareholders own smaller % of company. If raise is too big, stock drops on “dilution fear.”

*Timing*: 2026 is hot for AI, but if AI bubble pops in 2027, SK Hynix just built $100B of new fabs for demand that vanished. Memory is cyclical. Boom today, bust tomorrow.

*Geopolitics*: SK Hynix has China fabs. U.S.-China chip war adds risk. U.S. listing = more U.S. scrutiny on what tech goes where.

*Execution*: Building fabs on schedule is hard. TSMC delays are normal. If SK Hynix spends $29B but HBM2E arrives late, money burns.

6. What This Means For Micron, Samsung, Nvidia, AI Stocks

*For Micron MU*: Mixed. Competition gets more capital to fight for HBM share. But also validates “memory shortage thesis.” Micron +10% after-hours last week because of same demand story. SK Hynix ADR confirms demand is real.

*For Samsung*: SK Hynix is Samsung’s little brother in memory. Samsung may feel pressure to do U.S. listing too, or risk losing U.S. investors.

*For Nvidia AMD*: Good news. More HBM supply = fewer bottlenecks. If SK Hynix builds more fabs, Nvidia can sell more GPUs. AI capex cycle extends.

*For U.S. investors*: New way to play AI without betting only on Nvidia at 70x earnings. Memory is “picks and shovels” of AI gold rush.

7. Investor Playbook: How To Think About SK Hynix ADR

*If ADR launches in 2026:*

1. *Don’t buy day 1 IPO pop*: $29B deals often open high then fade as lockups expire. Wait 3-6 months for base to form.

2. *Compare to Micron*: ADR price vs MU P/E, margins, growth. If SK Hynix cheaper, arbitrage exists.

3. *Watch use of proceeds*: If 80% goes to new HBM fabs, bullish. If goes to debt/pay dividends, less bullish.

*If you already own Korean SK Hynix*: ADR listing = liquidity event. Your shares become more valuable because U.S. money can flow in. But also more volatility.

*Long-term thesis*: AI needs memory. Memory needs fabs. Fabs need $29B. This cycle has years left. SK Hynix wants to be the TSMC of memory.

Bottom Line In Your Words

SK Hynix planning a $29.4B Nasdaq ADR isn’t just news. It’s a statement:

“The AI boom needs so much memory that even the #2 player needs $29B to keep up.”

For U.S. investors, it means easier access to the company that’s quietly winning AI more than almost anyone. For the sector, it means memory chips are no longer “boring commodities.” They’re the bottleneck.

Will the ADR actually raise $29.4B? Will it be priced right? We’ll see when filings drop. But one thing’s clear: Wall Street is about to get a lot more exposure to HBM, and HBM is about to get a lot more capital.