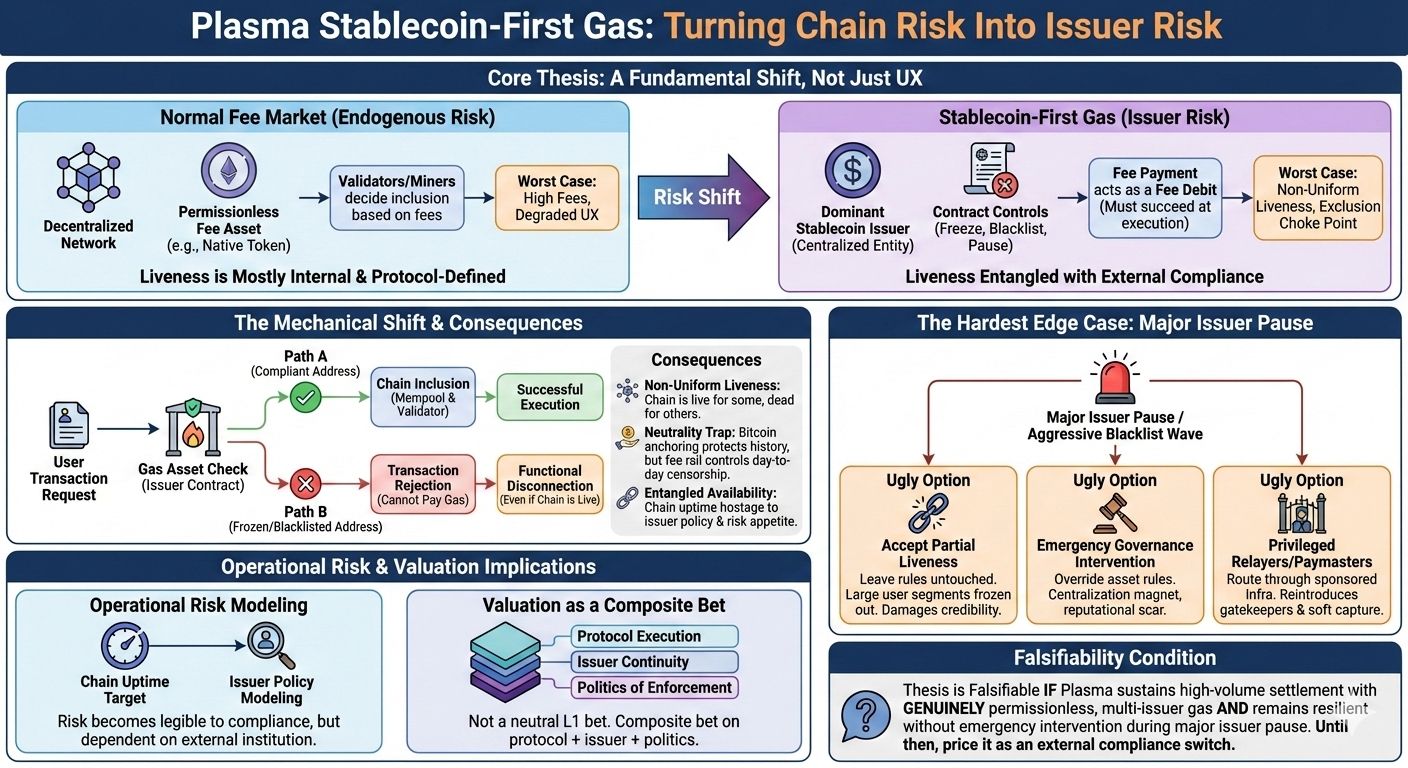

On Plasma, I keep seeing stablecoin-first gas framed like a user-experience upgrade, as if paying fees in the stablecoin you already hold is just a nicer checkout flow. The mispricing is that this design choice is not cosmetic. It rewires the chain’s failure surface. The moment a specific stablecoin like USDT becomes the dominant or default gas rail, the stablecoin issuer’s compliance controls stop being an application-layer concern and start behaving like a consensus-adjacent dependency. That’s a different category of risk than fees are volatile or MEV is annoying. It’s the difference between internal protocol parameters and an external switch that can change who can transact, when, and at what operational cost.

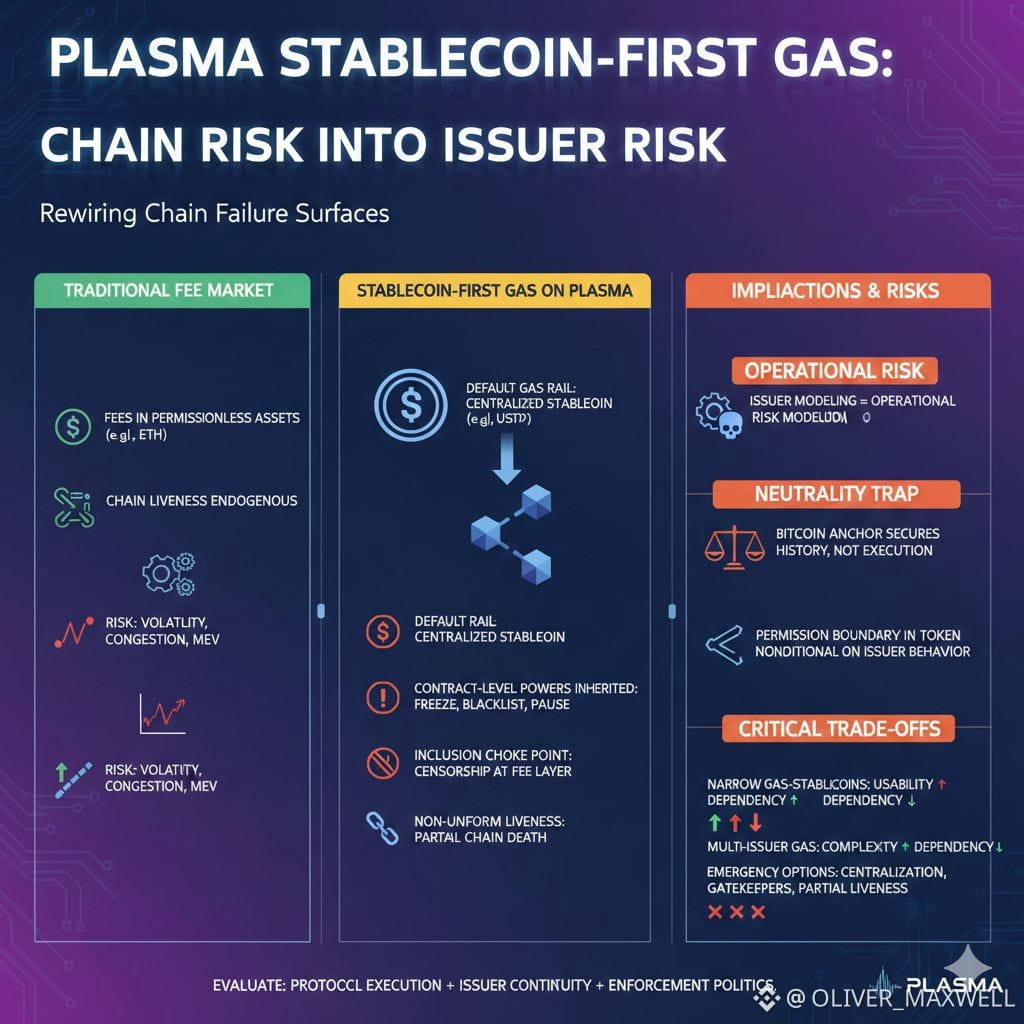

On a normal fee market, the chain’s liveness is mostly endogenous. Validators decide ordering and inclusion, users supply fees, the fee asset is permissionless, and the worst case under stress is expensive blocks, degraded UX, or a political fight about blockspace. With stablecoin-first gas, the fee rail inherits the stablecoin’s contract-level powers because fee payment becomes a fee debit that must succeed at execution time: freezing addresses, blacklisting flows, pausing transfers, upgrading logic, or enforcing sanctions policies that may evolve quickly and unevenly across jurisdictions. Even if Plasma never intends to privilege any issuer, wallets and exchanges will standardize on the deepest-liquidity stablecoin, and that default will become the practical fee rail. That’s how a design becomes de facto mandatory without being explicitly mandated.

Here’s the mechanical shift: when the gas asset is a centralized stablecoin, a portion of transaction eligibility is no longer determined solely by the chain’s mempool rules and validator policy. It is also determined by whether the sender can move the gas asset at the moment of execution. If the issuer freezes an address, it’s not merely that the user can’t transfer a stablecoin in an app. If fee payment requires that stablecoin, the user cannot pay for inclusion to perform unrelated actions either. That’s not just censorship at the asset layer, it’s an inclusion choke point. If large cohorts of addresses become unable to pay fees, the chain can remain up technically while large segments become functionally disconnected. Liveness becomes non-uniform: the chain is live for compliant addresses and partially dead for others.

The uncomfortable part is that this is not a remote tail risk. Stablecoin compliance controls are exercised in real life, sometimes at high speed, sometimes with broad scopes, and sometimes in response to events outside crypto. And those controls are not coordinated with Plasma’s validator set or governance cadence. A chain can design itself for sub-second finality and then discover that the real finality bottleneck is a blacklisting policy update that changes fee spendability across wallets overnight. In practice, the chain’s availability becomes entangled with an external institution’s risk appetite, legal exposure, and operational posture. The chain can be perfectly healthy, but if the dominant gas stablecoin is paused or its transfer rules tighten, the chain’s economic engine sputters.

There’s also a neutrality narrative trap here. Bitcoin-anchored security is supposed to strengthen neutrality and censorship resistance at the base layer, or at least give credible commitments around history. But stablecoin-first gas changes the day-to-day censorship economics. Bitcoin anchoring can harden historical ordering and settlement assurances, but it cannot override whether a specific fee asset can be moved by a specific address at execution time. A chain can have robust finality and still end up with a permission boundary that lives inside a token contract. That doesn’t automatically make the chain bad, but it does make the neutrality claim conditional on issuer behavior. If I’m pricing the system as if neutrality is mostly a protocol property, I’m missing the fact that the most powerful gate might sit in the fee token.

The system then faces a trade-off that doesn’t get talked about honestly enough. If Plasma wants stablecoin-first gas to feel seamless, it will push toward a narrow set of gas-stablecoins that wallets and exchanges can standardize on. That boosts usability and fee predictability. But the narrower the set, the more the chain’s operational continuity depends on those issuers’ contract states and policies. If Plasma wants to reduce that dependency, it needs permissionless multi-issuer gas and a second permissionless fee rail that does not hinge on any single issuer. But that pushes complexity back onto users and integrators, fragments defaults, and enlarges the surface area for abuse because more fee rails mean more ways to subsidize spam or route around policy.

The hardest edge case is a major issuer pause or aggressive blacklist wave when the chain is under load. In that moment, Plasma has three ugly options. It can leave fee rules untouched and accept partial liveness where a large user segment is frozen out. It can introduce emergency admission rules or temporarily override which assets can pay fees, which drags governance into what is supposed to be a neutral execution layer. Or it can route activity through privileged infrastructure like sponsored gas relayers and paymasters, which reintroduces gatekeepers under a different label. None of these are free. Doing nothing damages the chain’s credibility as a settlement layer. Emergency governance is a centralization magnet and a reputational scar. Privileged relayers concentrate power and create soft capture by compliance intermediaries who decide which flows are worth sponsoring.

There is a second-order effect that payment and treasury operators will notice immediately: operational risk modeling becomes issuer modeling. If your settlement rail’s fee spendability can change based on policy updates, then your uptime targets are partly hostage to an institution you don’t control. Your compliance team may actually like that, because it makes risk legible and aligned with regulated counterparties. But the chain’s valuation should reflect that it is no longer purely a protocol bet. It is a composite bet on protocol execution plus issuer continuity plus the politics of enforcement. That composite bet might be desirable for institutions. It just shouldn’t be priced like a neutral L1 with a nicer fee UX.

This makes Plasma specific. If the goal is  stablecoin settlement at scale, importing issuer constraints might be a feature because it matches how real finance works: permissioning and reversibility exist, and compliance isn’t optional. But if that’s the reality, then the market should stop pricing the system as if decentralization properties at the consensus layer automatically carry through to the user experience. The fee rail is part of the execution layer’s control plane now, whether we say it out loud or not.

stablecoin settlement at scale, importing issuer constraints might be a feature because it matches how real finance works: permissioning and reversibility exist, and compliance isn’t optional. But if that’s the reality, then the market should stop pricing the system as if decentralization properties at the consensus layer automatically carry through to the user experience. The fee rail is part of the execution layer’s control plane now, whether we say it out loud or not.

This thesis is falsifiable in a very practical way. If Plasma can sustain sustained, high-volume settlement while keeping gas payment genuinely permissionless and multi-issuer, and if the chain can continue operating normally without emergency governance intervention when a single major gas-stablecoin contract is paused or aggressively blacklists addresses, then the issuer risk becomes chain risk claim is overstated. In that world, stablecoin-first gas is just a convenient abstraction, not a dependency. But until Plasma demonstrates that kind of resilience under real stress, I’m going to treat stablecoin-first gas as an external compliance switch wired into the chain’s liveness and neutrality assumptions, and I’m going to price it accordingly.