Most conversations about robo focus on the robot. The hardware. The humanoid walking through a warehouse. The wheeled platform navigating a hospital corridor.

The quadruped inspecting an industrial site. What almost nobody is explaining clearly is the payment layer underneath all of that the mechanism by which one machine pays another machine for a service, without a human authorizing the transaction, without a bank processing the settlement, without a company's accounting department reconciling the ledger at month end. And honestly? That payment layer is the part of the Robo thesis that changes more than just robotics if it actually works 😂

Let me build this from the ground up because the mechanics deserve a clean explanation before the skepticism lands.

Today when a company deploys a robot for a task, payment flows through human infrastructure. A corporation owns the robot. The corporation invoices the client. The client's accounts payable team processes the invoice. A bank settles the transaction. Three to five business days. Multiple intermediaries. Each taking a fraction. The robot did the work. Humans handled the money. That separation between labor and payment is so deeply assumed that most people have never questioned whether it needs to exist.

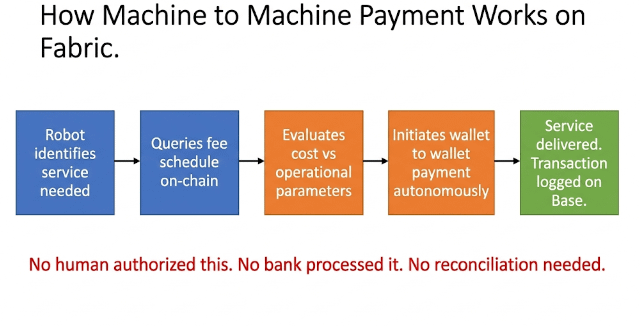

Fabric's machine to machine payment architecture removes that separation entirely. Here is how it actually works.

A robot registered on the Fabric protocol has an on-chain identity a verifiable address on Base blockchain tied to that specific machine's hardware configuration and operational history. That identity comes with a wallet. The wallet holds Robo tokens. The robot can receive tokens into that wallet autonomously. It can spend tokens from that wallet autonomously. No human co-signing required. No corporate treasury involved. The machine is the economic agent.

Imagine a day in 2029. A logistics robot completing a delivery route needs to pass through a privately operated charging station. The charging station is itself a machine — a smart infrastructure unit registered on the Fabric protocol with its own on-chain identity and wallet. The logistics robot's navigation system identifies the nearest available charging station, queries its fee schedule on-chain, evaluates whether the cost is within its operational parameters, and if so initiates a direct payment from its own wallet to the charging station's wallet. Robo tokens transfer. Charging begins. No human made that decision. No bank processed that payment. The entire transaction negotiation, payment, service delivery happened between two machines in seconds.

That is machine to machine payment. Not metaphorically. Literally.

What bugs me:

The elegance of the architecture raises an immediate practical question that the whitepaper addresses incompletely. If a robot holds tokens in its own wallet and can spend them autonomously — who is responsible when the robot makes a bad payment decision. The logistics robot in the scenario above evaluated the charging station's fee and decided it was within operational parameters. What if the fee schedule was manipulated. What if a malicious actor spoofed a charging station identity on-chain and drained the robot's wallet. The Fabric protocol includes bonding and slashing mechanisms for fraud — operators who deploy malicious infrastructure get their bonds slashed. But slashing happens after the fraud. The payment has already left the wallet. Recovery mechanisms for autonomous wallet transactions aren't detailed publicly in a way that addresses real-world attack vectors.

The tokenomics angle nobody discusses:

Total supply: 10B Robo fixed. Circulating: 2.23B — 22.3%. FDV: $391.6M. Market cap: $87.36M. FDV/MC ratio: 4.48x. Insider cliff: February 2027 — investors 24.3% plus team 20.0% combined 44.3%.

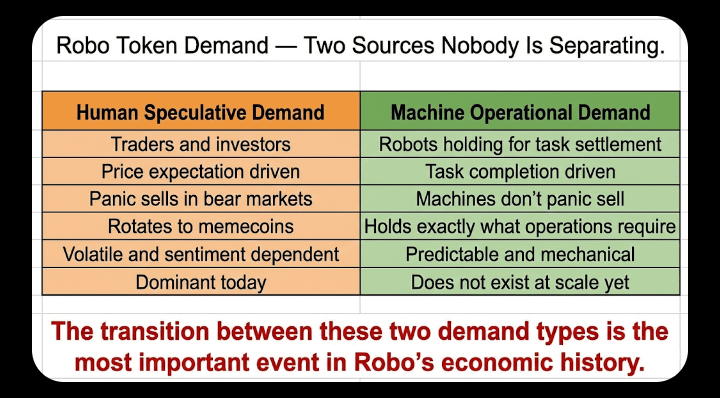

Machine to machine payments have a direct and undermodeled tokenomics implication. Every machine to machine transaction uses Robo tokens as the settlement currency. A logistics robot paying a charging station. A manufacturing robot paying a calibration service. A healthcare robot paying a data verification node. Each transaction is a fee event. Each fee event requires Robo tokens to be held by the paying machine and transferred to the receiving machine. As the number of registered machines grows and the number of machine to machine transactions compounds — the demand for Robo tokens as a settlement currency grows independently of any human holder's investment decision.

That's a genuinely different demand characteristic than most utility tokens have. Most utility tokens require humans to buy and hold them to access a service. Machine to machine payment demand requires machines to hold them to operate. Machines don't panic sell. Machines don't rotate into memecoins during a bull run. Machines hold exactly as much as their operational parameters require and spend exactly as much as their task completion demands. That mechanical demand — if the robot fleet scales — is structurally more predictable and less volatile than human speculative demand.

The original frame worth sitting with: Robo's token demand has two sources that almost nobody is separating in their analysis. Human speculative demand — traders, investors, governance participants buying and holding based on price expectations. And machine operational demand — robots holding tokens because their tasks require settlement in Robo. Today the demand is almost entirely human speculative. The bull case is that machine operational demand eventually dominates and becomes the stable demand floor that human speculative demand trades above. That transition — if it happens — changes the token's volatility profile fundamentally. A token with a mechanical demand floor from millions of operating robots behaves differently in a bear market than a token whose demand is entirely human sentiment driven.

My concern though:

The machine operational demand thesis depends entirely on robot fleet scale that doesn't exist yet. Today there are no robots generating machine to machine payment volume on the Fabric protocol at any meaningful scale. The protocol is in early rollout. The demand floor from mechanical robot payments is theoretical. The February 2027 cliff arrives on a fixed calendar regardless of whether machine operational demand has materialized. If the cliff opens before robot fleet deployment reaches meaningful scale — the token's demand at that moment is still primarily human speculative. Human speculative demand is far more fragile than mechanical operational demand under supply pressure. That sequencing risk — cliff before mechanical demand floor — is the variable most Robo holders haven't modeled against the machine to machine payment thesis.

What they get right:

The Base chain selection makes machine to machine micropayments economically viable in a way that Ethereum mainnet never could. A logistics robot paying a charging station a fraction of a cent in Robo tokens needs the gas cost of that transaction to be smaller than the payment itself. On Ethereum mainnet that math fails for any micropayment below several dollars. On Base — Coinbase's L2 — gas costs are low enough that true micropayments between machines become economically rational. That infrastructure decision is not cosmetic. It determines whether machine to machine payments work at the granularity the use case requires.

The ERC-7777 standard for machine identity that Fabric is contributing creates a foundation for machine to machine payment trust that extends beyond the Fabric ecosystem. If that standard gets adopted broadly — by other robot operating systems, by smart infrastructure providers, by autonomous vehicle networks — then any machine running ERC-7777 identity can transact with any other ERC-7777 machine regardless of manufacturer. The payment rails become as open as the internet. That's the infrastructure bet underneath the token.

The bonding mechanism for infrastructure operators — requiring machines and the humans who deploy them to post Robo tokens as operational bonds — creates aligned incentives against the fraud vectors the architecture opens. An operator running a spoofed charging station risks losing their bond if caught. The economic penalty is designed to exceed the economic gain from fraud. Whether that deterrent is sufficient against sophisticated attackers is uncertain. But the design logic is correct.

What worries me:

The regulatory question sitting underneath autonomous machine wallets is the most underexamined risk in the entire Robo thesis. A robot that holds its own wallet, makes its own payment decisions, and accumulates its own wealth is not a tool under existing legal frameworks — it is something law has no clean category for. Different jurisdictions will reach different conclusions about whether autonomous machine wallets constitute money transmission, whether the tokens held in them are property of the operator or the machine, and whether machine to machine payments require the same KYC and AML compliance that human to human payments require. The Fabric protocol is being built as if regulatory clarity exists. It doesn't. When it arrives — and it will arrive — the shape of that clarity will either validate the architecture or require fundamental redesign.

Only 2,730 total holders are currently pricing a token whose machine to machine payment thesis requires millions of deployed robots generating billions of micro-transactions daily to validate. The distance between that vision and today's reality is measured in years of hardware deployment, regulatory navigation, enterprise adoption, and protocol maturation. The token is trading against the vision. The vision is trading against a timeline the protocol doesn't control.

Honestly don't know if machine to machine payments become the quiet infrastructure revolution that makes Robo's mechanical demand floor the most defensible token thesis in crypto, or if regulatory frameworks arrive before robot fleet scale does and reshape the payment architecture in ways the current token design hasn't anticipated. Both outcomes are sitting inside the same elegantly designed protocol.

What's your take - machine to machine payments genuine new economic primitive or infrastructure thesis that arrives too early for its own regulatory environment?? 🤔