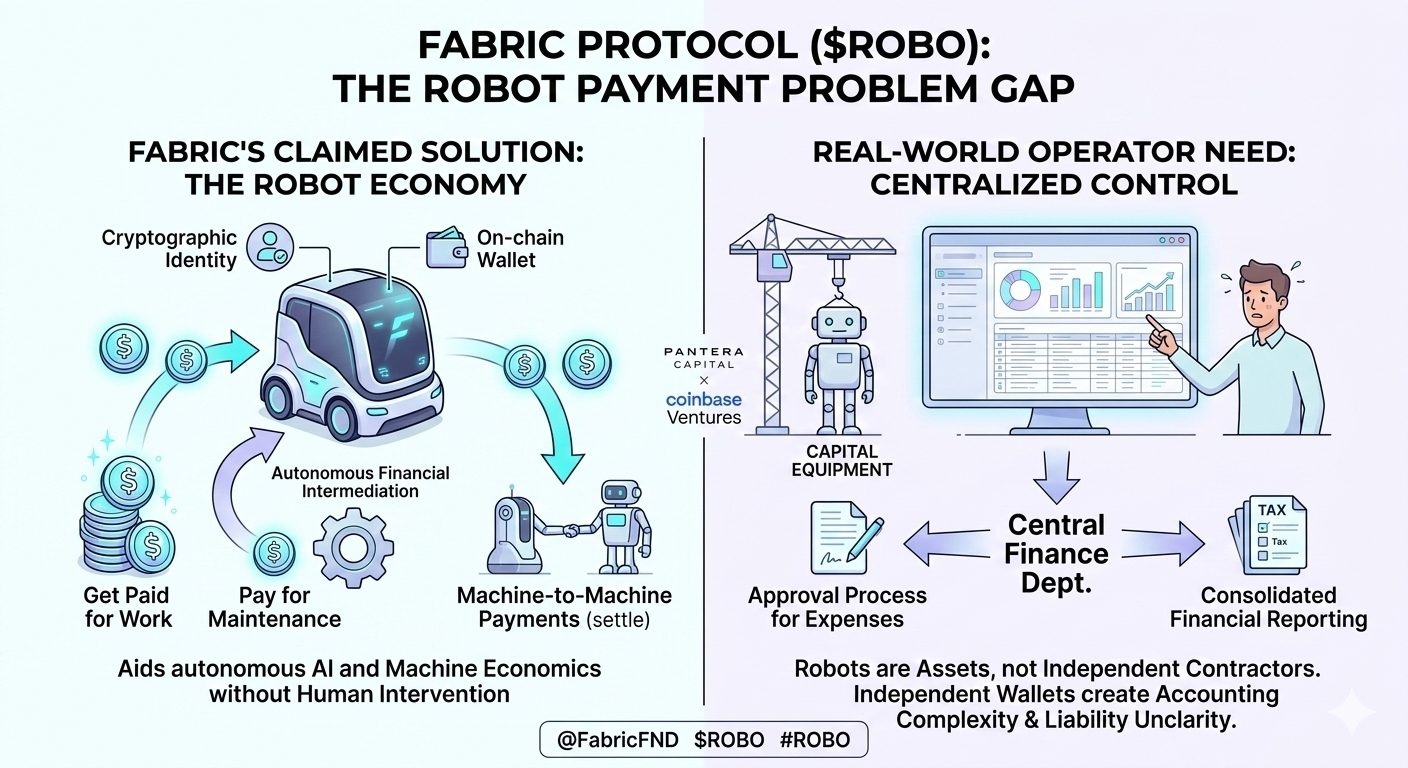

Fabric Protocol launched $ROBO claiming to solve a critical bottleneck in robotics: robots can’t open bank accounts, hold legal identities, or participate as independent economic actors. The protocol provides on-chain wallets and identities letting robots get paid for work, pay for their own maintenance, and operate autonomously without human financial intermediation. The concept makes logical sense until you talk to actual robot manufacturers and operators who reveal they don’t want robots functioning as independent economic entities for reasons Fabric’s infrastructure doesn’t address.

The core thesis states that robots need autonomous payment capabilities to enable the “robot economy” where machines work, earn money, settle their own expenses, and coordinate tasks without humans handling every financial transaction. Fabric built blockchain infrastructure giving robots cryptographic identities, wallets holding $ROBO tokens, and smart contracts enabling machine-to-machine payments. Operators stake $ROBO as collateral when registering robots, task requesters pay robots in $ROBO, and protocol revenue gets used to buy $ROBO creating demand pressure.

This sounds innovative until you understand how robot economics actually work in commercial deployments today. I talked to operations leadership at a logistics company using autonomous mobile robots in their warehouse. When I asked whether they’d want robots handling their own payments and expenses, the response revealed why Fabric’s value proposition might not match real operator needs.

“We own the robots. We pay for maintenance. We assign tasks. The robots are capital equipment, not independent contractors. Having them hold wallets and pay their own bills creates accounting complexity we don’t want. We need centralized financial tracking for budgeting, tax reporting, and operational planning. Decentralizing robot payments makes our finance department’s job harder without providing benefits we’re asking for.”

This pattern repeated across conversations with robot operators. They view robots as owned assets, not autonomous economic agents. Financial independence for robots creates problems rather than solving them. Companies need consolidated financial reporting showing total automation costs. They want predictable budgets, not robots making autonomous spending decisions. They require approval processes for maintenance and upgrades, not robots self-authorizing expenses. The autonomous payment model that Fabric enables conflicts with how organizations actually want to manage robot operations.

Manufacturing companies showed similar perspectives. A robotics deployment manager at an automotive supplier explained their approach. “Our robots are tracked as depreciating assets on the balance sheet. Maintenance is scheduled through central planning. Task allocation happens through our warehouse management system. We don’t need robots operating as independent economic entities because that would complicate asset tracking, financial planning, and operational control. The robots are tools we own and manage, not workers we hire and pay.”

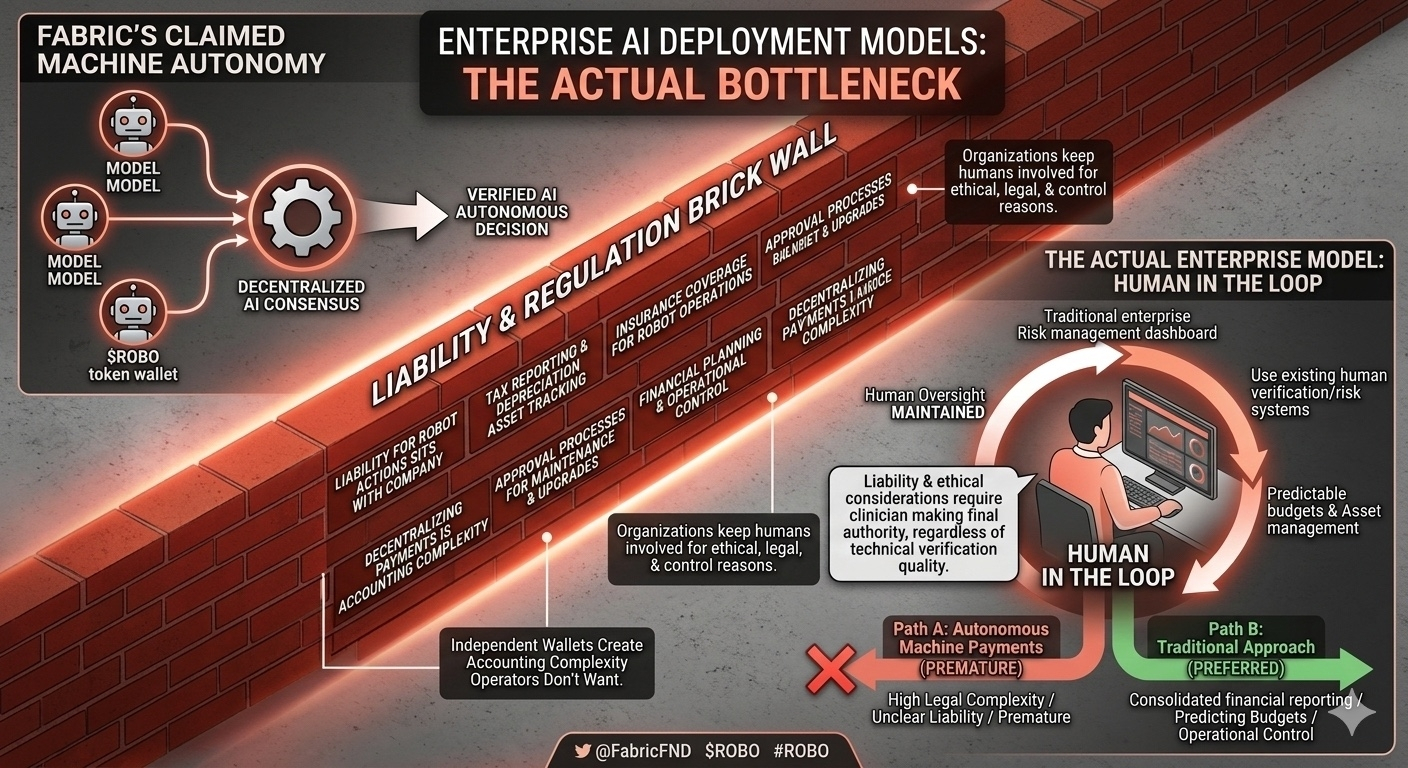

The legal and liability structure creates additional barriers. Organizations maintain insurance covering robot operations. Liability for robot actions sits with the company owning the robots, not with the robots themselves. If robots operated as independent economic entities, the liability framework would become unclear. Who’s responsible when autonomous robots cause damage or make mistakes? The legal complexity of robot economic independence might exceed any operational benefits, making organizations prefer keeping robots as owned assets rather than autonomous agents.

Fabric’s coordination mechanisms assume robots from different operators need to coordinate tasks and settle payments between themselves. But commercial robot deployments typically involve single-vendor solutions within facilities specifically to avoid coordination complexity. Companies buy integrated systems from vendors who handle coordination through proprietary software. The multi-vendor robot coordination that would need Fabric’s infrastructure rarely exists in practice because operators deliberately avoid creating that complexity.

The token economics depend on transaction volume from robot payments, task settlements, and maintenance expenses flowing through $ROBO. If operators keep robots as owned assets with centralized financial management rather than independent economic entities, the transaction volume doesn’t materialize. The infrastructure works technically while serving a use case that commercial operators aren’t adopting because it creates problems rather than solving them.

Fabric raised roughly $20 million from investors including Pantera Capital and Coinbase Ventures based on the robot economy vision. The protocol recently listed on major exchanges including Binance, Coinbase, and KuCoin. Token supply is 10 billion $ROBO with 29.7% allocated to ecosystem and community. The technology exists to enable robot economic independence. The question is whether organizations operating robots actually want that independence or whether they prefer robots remaining as controlled assets within centralized financial management.

For anyone evaluating $ROBO, the critical question is whether the robot economy model matches how organizations actually deploy and manage robots. Conversations with operators suggest they view robots as capital equipment requiring centralized oversight rather than autonomous agents needing independent payment capabilities. That doesn’t mean Fabric’s vision is wrong, but it suggests adoption might require fundamentally changing how organizations think about robot ownership and management rather than just providing infrastructure for a model operators are already pursuing.