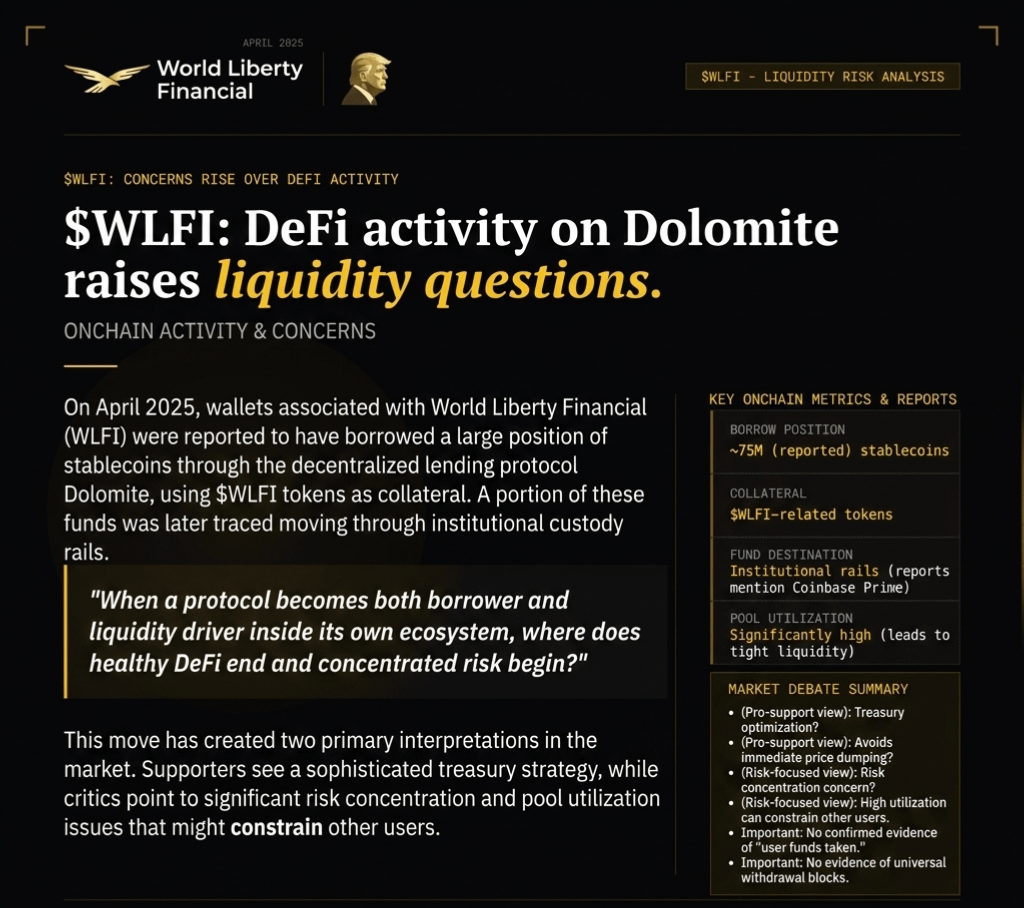

On April 2025, wallets associated with World Liberty Financial (WLFI) were reported to have borrowed stablecoins via the decentralized lending protocol Dolomite, using WLFI-related tokens as collateral.

Some onchain trackers suggest:

A large stablecoin borrow position (~$75M range reported in community analysis) was opened against WLFI collateral.

A portion of borrowed funds was later moved through institutional custody rails (reports mention Coinbase Prime usage), though final purpose (treasury, liquidity, or operations) is not independently confirmed.

The position size appears significant relative to liquidity conditions within the lending pool, according to DeFi dashboard estimates.

What this means in DeFi terms

In lending protocols like Dolomite, this structure is not unusual:

Assets are deposited into liquidity pools by users

Borrowers take loans against collateral

Interest rates adjust based on utilization

When utilization becomes very high, liquidity can become tight leading to slower withdrawals or higher borrowing costs for others.

The debate

There are two interpretations in the market:

1️⃣ Pro-support view (treasury strategy):

The borrow could be part of liquidity management or treasury operations

Using DeFi borrowing avoids direct token sales, reducing immediate market impact

High-yield environments often rely on large anchor borrowers to stabilize utilization

2️⃣ Risk-focused view (centralization concern):

Heavy borrowing against protocol-related assets raises questions about risk concentration

If collateral value drops, liquidation pressure could increase selling risk

If liquidity is thin, users may experience withdrawal delays or reduced flexibility

Connections between advisors and ecosystem participants raise governance concerns for some observers

Important clarification

There is no confirmed evidence that “user funds were taken” or that withdrawals are universally “stuck.”

In DeFi lending, liquidity constraints typically refer to pool utilization levels, not direct confiscation of deposits.

Final fund usage (treasury, market operations, or custody conversion) has not been independently verified in full detail publicly.

The question ❓ came to mind Why this matters???

This situation highlights a core DeFi tension:

"High yields and aggressive borrowing strategies can improve short-term liquidity efficiency but they also increase systemic risk if leverage, governance, or liquidity depth is concentrated"

This is less about a confirmed exploit, and more about a risk structure question:

When a protocol becomes both borrower and liquidity driver inside its own ecosystem, where does healthy DeFi end and concentrated risk begin?

#WLFI #TRUMP #JustinSunVsWLFI #LearnWithFatima #MarketSentimentToday $WLFI $USD1