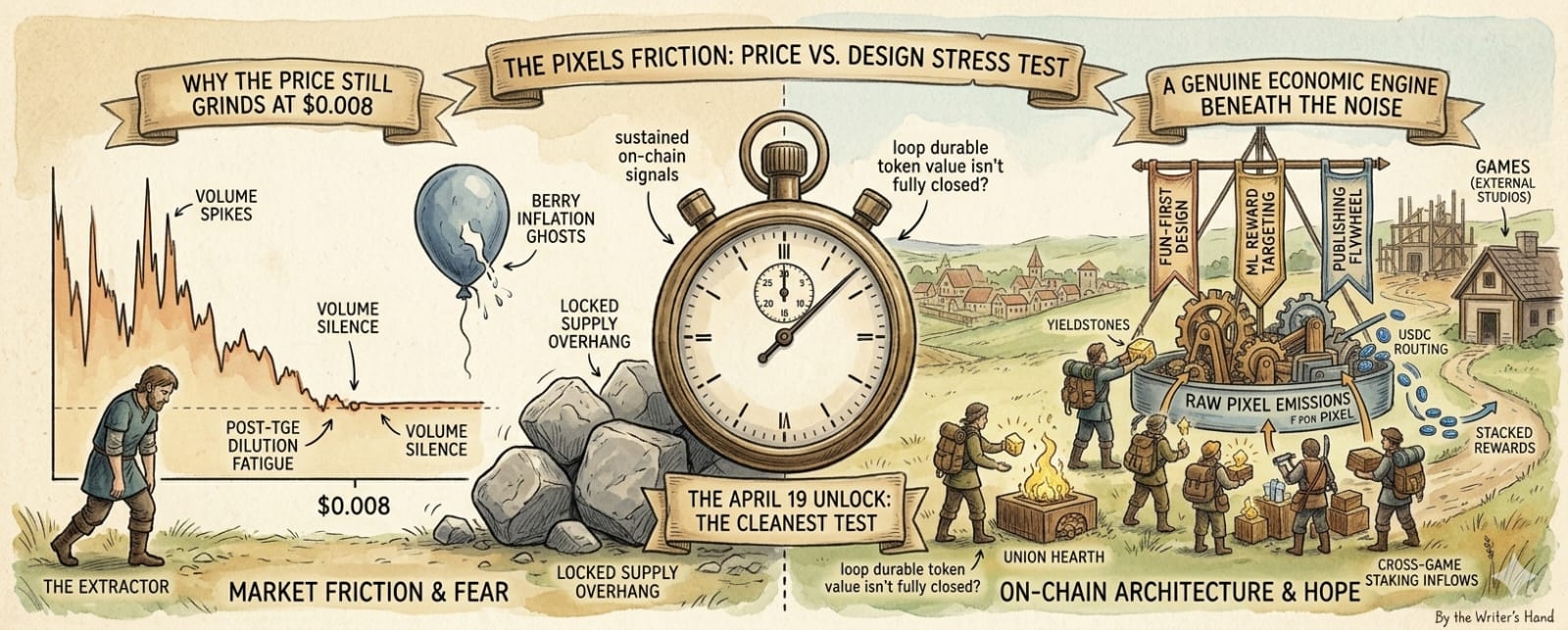

What keeps bothering me about Pixels is how the token price continues grinding around the $0.008 level even after Chapter 3 Bountyfall launched last October and the Stacked rewards app went live in March. Circulating supply now sits at roughly 3.38 billion out of 5 billion total, market cap near $27 million, and another 91 million tokens worth roughly $700,000 at current prices are due to unlock on April 19. Volume spikes to $15–20 million on some days then fades into silence. I noticed this gap because the project narrative says the old BERRY inflation problems are behind us, yet the chart still reads like classic post-TGE dilution fatigue.

The part that feels more important, and stranger, is that Pixels’ internal mechanics appear deliberately built to neutralize exactly this kind of unlock pressure. The three pillars in their documentation fun-first design, machine-learning reward targeting, and the publishing flywheel are not abstract ideas. Chapter 3 pushes players into one of three Unions where they gather tiered Yieldstones through normal play and land use, then either reinforce their own Hearth or strategically undermine rivals. Prize pools scale with real participation. Reputation gates still restrict low-trust wallets from heavy trading or withdrawals. Stacked, meanwhile, increasingly routes rewards in USDC rather than raw PIXEL to limit immediate sell pressure. The fundamental shift has moved from “emit more to keep users logging in” to “emit only what genuine on-chain activity can absorb.”

If this reading holds, the implications are clear. Today’s pattern of spiky CEX volume should start mattering less than sustained on-chain signals like Union activity, Hearth contributions, and sabotage volume. Wallet concentration and the remaining locked supply would feel less risky if the reputation system and land-based economic PVP keep filtering out pure extractors. The publishing flywheel would begin proving itself by actually lowering user acquisition costs for new titles. Should Return on Reward Spend stay sustainably above 1.0 and Stacked successfully onboard external studios without forcing PIXEL sales, the final third of supply turns from overhang into concentrated long-term governance and staking power.

I’m not fully convinced the transition is finished. The team continues shipping bi-weekly updates and Union seasons are live, but I keep returning to how little the current price seems to reflect this deeper architecture. What the market may be mispricing is the assumption that Pixels remains just another single-game play-to-earn token capped by farming rewards. In my view, PIXEL has quietly become the settlement layer for a broader publishing system staking directing resources across games, vPIXEL enabling clean utility, and the data engine rewarding only behaviors that drive real revenue. The friction is genuine, yet the design is already working around it.

The specific reading I’m carrying forward is this: the April 19 unlock and the ones that follow will be the cleanest test yet. If Union deposits, sabotage activity, and cross-game staking inflows hold or rise through the release without a clear price reaction, the market will have been slow to see that token demand has moved past the old reward-spend problem. If the price simply absorbs the new supply as more weight, then the loop between player activity and durable token value isn’t fully closed. That single data point will show which version of Pixels the market is actually pricing.