The market is no longer asking whether Bitcoin matters, but what kind of asset it is becoming

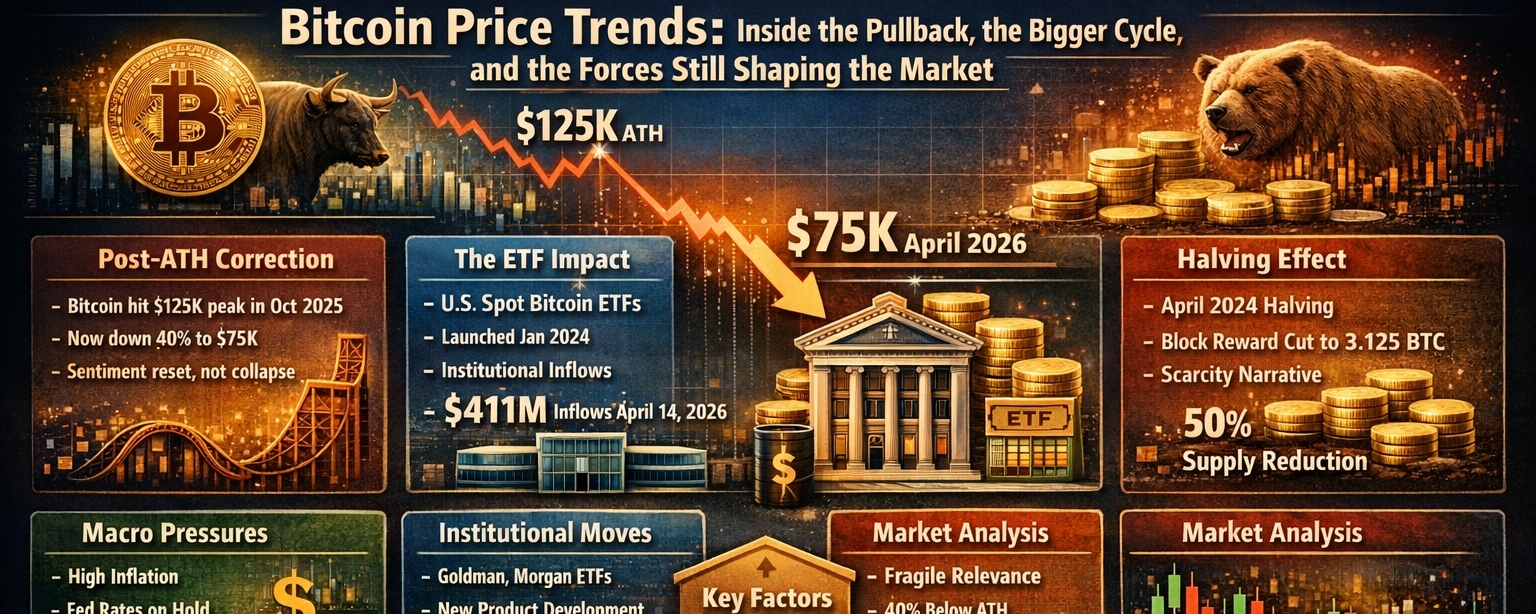

Bitcoin’s price trend in April 2026 is difficult to reduce to a simple bullish or bearish label, because the market is balancing two realities at once: on one side, Bitcoin is still trading far below the record high it set in early October 2025, and on the other side, it remains deeply embedded in institutional products, ETF flows, and macro conversations in a way that would have been hard to imagine only a few years ago. The latest market price from the finance tool places Bitcoin near $75,051, while Reuters reported that Bitcoin rose above $125,245 on October 5, 2025, which means the asset is still sitting in a drawdown of roughly 40% from that peak, a decline large enough to reset sentiment but not large enough, at least yet, to erase the broader institutional story around it.

That is why Bitcoin price trends right now are less about raw excitement and more about market character, because what the market is showing is not the easy vertical momentum of a clean breakout phase, but the harder and more revealing process that comes after excess, when a major rally has already happened, expectations have already overshot, and the asset now has to prove whether it can hold relevance after the emotional part of the move has faded. Reuters noted this week that Bitcoin was down nearly 15% year to date when it was trading around $74,591, which captures the tone of the current phase quite well: not a collapse into irrelevance, but a correction that has forced the market to trade under scrutiny instead of under excitement.

The post-October 2025 correction changed the mood more than the structure

When Bitcoin pushed to a new all-time high above $125,000 in October 2025, the market was trading on a combination of momentum, institutional demand, and a broader belief that the asset had entered a new and more durable phase of acceptance. Reuters described that record move at the time as part of a strong rally fueled by investor appetite, and in the same month Reuters also reported record inflows into global crypto ETFs, with $5.95 billion entering the category in the week ending October 4, 2025, which shows how powerful the demand backdrop looked near the top.

But Bitcoin has a long history of punishing anyone who assumes that a strong narrative is enough to sustain a straight-line price trend, and the current pullback fits that pattern. What matters here is that the decline from the October high has not simply been a technical dip inside a smooth advance, because it has forced the market to reassess what actually drove the move in the first place, and whether that move was supported by durable allocation demand or was partly accelerated by the kind of reflexive enthusiasm that always shows up when Bitcoin begins printing new highs. That distinction is important, because Bitcoin often does not fail by losing all of its long-term appeal, but by getting priced too far ahead of conditions that cannot support that level of optimism for very long.

The ETF era permanently changed Bitcoin’s trend behavior

One of the clearest reasons Bitcoin now behaves differently from earlier cycles is the arrival of the U.S. spot Bitcoin ETF market, because the Securities and Exchange Commission officially approved the listing and trading of spot Bitcoin exchange-traded products on January 10, 2024, creating a cleaner bridge between Bitcoin and traditional portfolio construction. That approval did not remove volatility, and it certainly did not make Bitcoin conservative, but it changed the type of capital that could participate and, just as importantly, the speed and format through which participation could happen.

That shift matters because Bitcoin is no longer being priced only by crypto-native traders responding to internal narratives, exchange positioning, and sentiment inside the digital asset ecosystem. It is also being priced by advisors, funds, model portfolios, tactical allocators, and product manufacturers that think in terms of exposure, volatility budgets, inflow momentum, and correlation. Farside’s daily ETF flow data shows that the U.S. spot Bitcoin ETF complex is still seeing meaningful movement in April 2026, including net inflows of $411.4 million on April 14 and strong gross creation in several vehicles, while CoinShares reported that digital-asset investment products attracted about $1.03 billion in weekly inflows in its latest April 13 update, with Bitcoin products accounting for roughly $790 million of that amount.

The significance of this is not just that capital is still entering the ecosystem, but that Bitcoin now lives inside a market structure where flows can reinforce trends in both directions. During strong phases, steady ETF demand can turn a constructive move into a powerful surge because there is an automatic and visible mechanism for converting interest into buying pressure. During fragile phases, however, the same structure can expose Bitcoin to tactical de-risking from investors who do not have any emotional attachment to the asset and will reduce exposure the moment macro conditions or volatility profiles turn less attractive. That is one reason the ETF era made Bitcoin more legitimate while also making it more directly exposed to the same shifting allocation logic that shapes other risk assets.

Scarcity still matters, but it no longer explains everything by itself

Bitcoin’s 2024 halving remains an essential part of any serious discussion of price trends, because the block reward fell to 3.125 BTC in April 2024, reducing the rate at which new supply enters the market. That change is structurally supportive over time, and it reinforces the central idea that Bitcoin’s issuance schedule remains one of the asset’s defining characteristics. But scarcity is not the same thing as immediate price support, and one of the most common mistakes in Bitcoin analysis is to assume that a supply-side improvement automatically overrides every cyclical and macro headwind at the same time. The halving changes issuance mechanics; it does not neutralize inflation fears, geopolitical stress, portfolio deleveraging, or the consequences of a market that has already run too far too quickly.

This is why Bitcoin often confuses both believers and critics. Believers tend to overestimate how quickly structural positives should show up in price, while critics tend to underestimate how much structural discipline can matter over longer periods even when near-term trading looks weak. The current environment sits exactly in that tension, because the scarcity framework is still intact, the institutional access framework is stronger than before, and yet price is not behaving like a market that has been handed an easy road forward. That does not invalidate the long-term case; it simply means the market is still governed by present-tense capital conditions, and right now those conditions are demanding.

Macro pressure is now central to the Bitcoin trend, not secondary to it

One of the most important developments in Bitcoin’s maturation is that macro conditions now matter in a much more direct and visible way than they did in earlier years, which means rate expectations, inflation trends, oil shocks, and geopolitical instability now affect Bitcoin not just indirectly through mood, but directly through liquidity and risk appetite. Reuters reported on April 15 that St. Louis Fed President Alberto Musalem expects high oil prices tied to the war involving the U.S., Israel, and Iran to keep core inflation near 3% for the rest of 2026, well above the Federal Reserve’s 2% target, and he argued that rates may need to stay on hold for some time. Reuters separately reported that Cleveland Fed President Beth Hammack also sees rates staying unchanged for “a good while,” reinforcing the sense that monetary policy is unlikely to turn supportive in the near term.

That matters for Bitcoin because the asset still behaves, in practice, like a liquidity-sensitive instrument even when its long-term narrative is framed in harder monetary terms. When inflation stays sticky and central banks remain cautious, the market becomes less willing to pay aggressively for assets whose appeal depends partly on future growth in adoption, demand, and speculative participation. This does not mean Bitcoin stops functioning as a scarcity asset, but it does mean the path of the price becomes more vulnerable to macro tightening and less able to rely on narrative alone. Barron’s described Bitcoin this week as constrained by geopolitical risks, cautious institutional demand, and fading expectations for rapid rate cuts, while the Economic Times similarly linked the recent trading range to a tug of war between ETF support and broader uncertainty.

Institutional product expansion is continuing even during the drawdown

An especially important signal in the current cycle is that large financial institutions are still building Bitcoin products even after the market has already suffered a major drawdown from its peak. Reuters reported on April 14 that Goldman Sachs filed for its first Bitcoin ETF product, designed to combine Bitcoin price exposure with options-based income, following closely after Morgan Stanley launched its own spot Bitcoin ETF. That development says quite a lot about how Wall Street now sees the category, because institutions do not usually spend time designing, filing, and packaging new products around something they believe has already passed its window of relevance.

This does not guarantee a bullish price trend in the near term, and it certainly does not remove the downside risk that comes with a volatile and still maturing market. But it does reinforce the idea that Bitcoin’s long-term role in the financial system is becoming harder to dismiss. Even when the chart looks soft, the infrastructure around Bitcoin keeps deepening, and that widening infrastructure matters because it tends to stabilize attention even when it does not stabilize price. In previous cycles, a sharp correction could easily trigger questions about whether the entire asset class would lose institutional interest; in the current cycle, the more notable fact is that institutions are still creating new ways to distribute Bitcoin exposure during the correction itself.

What the current price trend is really saying

The cleanest way to read Bitcoin right now is that it is in a post-peak correction inside a broader institutionalized cycle, which is a more nuanced condition than either a full bull continuation or a structural breakdown. The current price near $75,000 shows that the market has not recovered the emotional force of late 2025, and the drawdown from above $125,000 confirms that the market is still digesting a period of excess. At the same time, ongoing ETF inflows, continued product launches, and the persistence of Bitcoin in mainstream market coverage all suggest that the broader cycle has not simply ended in the old sense of speculative collapse followed by disappearance.

The phrase that probably fits best is fragile relevance. Bitcoin is clearly still relevant, because flows, products, and macro commentary all continue to revolve around it. But it is fragile because the market no longer has the luxury of rising on enthusiasm alone, and each new advance now has to contend with inflation uncertainty, rate sensitivity, geopolitical stress, and a more crowded institutional audience that is willing to rotate quickly if conditions worsen. That is a more mature market, but it is not an easier one.

The technical and psychological dimension of the trend

From a trend perspective, the most important psychological fact is that Bitcoin is trading far enough below its record high that every rally is now being judged not as a fresh discovery of value, but as an attempt to recover lost ground. That changes behavior. A market making new highs usually attracts momentum traders, trend followers, and fresh believers who feel like they are witnessing confirmation. A market that has already broken sharply from those highs attracts a more cautious crowd, because every bounce has to prove that it is not just a relief move inside a larger corrective structure. That is part of why the current phase feels slower and more conflicted, even though the absolute price level is still historically elevated.

This is also where Bitcoin’s history matters. Deep retracements are common enough that they cannot be treated as unusual by themselves, yet each retracement still feels uniquely dangerous while it is happening because Bitcoin tends to magnify both greed and doubt more aggressively than most major assets. The October 2025 high created a strong memory point for the market, and memory points are powerful because they anchor expectations. Until Bitcoin either meaningfully rebuilds above current levels or breaks down far enough to force a new repricing of the entire cycle, the market is likely to remain trapped between those two reference frames: the memory of $125,000 and the reality of a macro-sensitive market trading around $75,000.

What could shape the next major move

The next decisive phase in Bitcoin’s price trend will likely depend less on a single crypto-specific catalyst and more on the interaction between macro relief and institutional participation. If inflation pressure eases, oil prices normalize, and the market begins to believe that central banks have room to become less restrictive, Bitcoin could recover quickly because ETF infrastructure and institutional access are already in place. But if inflation remains elevated and rates stay higher for longer, Bitcoin may continue to behave like a high-beta expression of broader risk appetite, which would keep rallies more vulnerable and consolidations more prolonged. Reuters’ recent reporting on inflation, oil shocks, and Fed caution supports exactly that interpretation, because the market backdrop is not one where easy liquidity is returning on demand.

That means Bitcoin’s next move is not only about whether people believe in the asset, but about whether the broader environment allows capital to act on that belief in size and with enough persistence to sustain trend strength. This is an important distinction, because strong narratives often survive bearish phases, but price only turns decisively when narratives and capital conditions finally align. Right now the narratives remain alive, but the capital backdrop is still unsettled.

Final view

Bitcoin price trends in 2026 are no longer a story about a fringe asset occasionally catching mainstream attention; they are now a story about how a volatile, scarce, highly reflexive instrument behaves after becoming woven into institutional products and macro-sensitive portfolios. The current price action is weaker than enthusiasts would prefer, because a 40% drawdown from a record high is too large to dismiss as noise, but it is also stronger than critics often suggest, because Bitcoin remains central to ETF flows, product launches, and broader market analysis even after the correction.

So the most honest conclusion is that Bitcoin is not in a clean breakout trend, and it is not in a dead market either. It is in a difficult middle phase, where structural adoption remains intact, but enthusiasm has already been forced through reality. That usually produces a market that is slower, more selective, and much harder to read, but also more revealing. And right now, what Bitcoin is revealing is that its price trend depends less on mythology than before, and more on the harder intersection of flows, policy, volatility, and conviction.